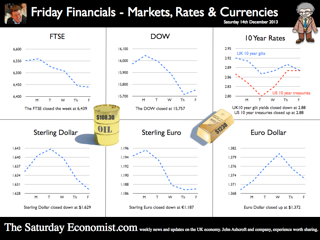

Economics news – the spirit of Christmas present is a cheerful spirit ... The spirit of Christmas Past - should not be forgotten. The spirit of Christmas Present - is a cheerful spirit. The spirit of Christmas Yet to Come suggests that it is unlikely that equilibrium interest rates will return to historically normal levels any time soon”. Excellent. Don’t you just love a central banker with a Christmas message. Governor Carney was speaking in New York this week at the Economic Club of New York. The Governor is anxious to secure the message, interest rates will not rise any time soon. The recovery will not be put at risk. The UK will achieve escape velocity from a liquidity trap, avoiding secular stagnation in the process. Forward guidance is the new policy mantra, secular stagnation the new spectre on the blog. The UK is set for recovery, despite the prophets of gloom on either side of the Atlantic. Forward guidance is integral to the central bankers response to the recession and setback. FG reduces uncertainty, providing reassurance that monetary policy will not be tightened before the recovery is sufficiently established. Businesses will have the confidence to invest. Households will have the confidence to spend. A liquidity trap is avoided. A liquidity trap occurs when the short-term nominal interest rate hits the zero lower bound. Typically in a liquidity trap, inflation is low, the equilibrium real interest rate is negative, creating a persistent inability to match aggregate demand and supply. Businesses won’t invest and consumers are reluctant to spend, aggregate demand continues to fall and a deflationary spiral develops. Fiscal constraints ensure Government spending cannot bridge the output gap. In the UK, the financial crisis pushed the equilibrium real interest rate to the lower bound. With nominal interest rates stuck at zero, and inflation low, monetary policy was unable to push actual real rates to a level low enough to generate growth allegedly. “Pushing on a string, is no way to wag the dog”. I think Keynes said that. Hence the emergence of QE on Planet ZIRP. Allegedly, a way to stimulate liquidity AND activity. In reality, a great way to undermine the gilt curve and returns to savers and investors in the process. So what of secular stagnation? Larry Summers had recently raised the spectre of secular stagnation at the IMF meeting in November in honour of Stanley Fischer, guru of monetary theory at MIT. Secular stagnation, a concept first developed by Alvin Hansen in the 1920s suggested the “new normal” in the USA (post depression) was of lower growth, primarily a result of lower population growth and technological exhaustion. No new things to boost productivity, that sort of thing. Larry Summers, resurrected the term, suggesting the short term real interest rate consistent with full employment may have fallen to -2% -3% in the middle of the last decade. “The natural and equilibrium interest rates may have fallen significantly below zero”. “We may have to think about how we manage an economy in which the zero nominal interest rate is a chronic and systemic inhibitor of economic activity holding our economies back below their long run potential.” he said. In theory, the Fed funds rate can be kept at ZIRP forever but it is much harder to do “extraordinary additional stuff” forever” either in the form of QE, or government deficit funding perhaps. This said Summers, is “my” lesson from this crisis which the world has “under internalised”. Actually Summers went on to say “Now this may all be madness and I may not have this right at all”. Mmm. Stuck on Planet ZIRP, QE was introduced, the effect of which, was to ensure we were marooned on the planet for longer. ZIRP creates of itself a problem which is compounded by QE. In the UK, QE has lost intellectual credibility and momentum but in the USA the persistent purchase of Treasuries and Mortgages (CMBS) continues, achieving no more for Uncle Sam, than a monthly dispensation into a NASDAQ tracker fund. It really is time to begin tapering in the US, end QE and return the equilibrium rate of interest to a natural rate. A natural rate for gilts and treasuries, which reflects an inflation hedge and a real rate of return to risk. In his speech, Summers said, “we have learned one thing, finance cannot be left to the financiers”. Perhaps but then I have always felt much the same about monetary economics. We should begin to think how we can manage an economy in which the academics are confined to campus and not allowed near policy levers. The concept of a negative equilibrium interest rate, which may have fallen to -3% pre recession is as incomprehensible, as life on Planet ZIRP without oxygen. The escape from ZIRP and the beginning of recovery can only be accelerated by an end to QE. Let the free markets free and end QE - the cry. It is time to suggest “Schools out for Summers” and the MIT class of 14462. The US is set to grow by over 2.5% next year or has no one noticed. Back in the UK Back in the UK, as expected the march of the makers picked up the pace in October. Manufacturing growth year on year increased to 2.7% in the month. Construction output grew at over 5% in the latest data for October. The trade figures on the other hand continued to disappoint. The UK's deficit on trade in goods and services was estimated to have been £2.6 billion in October 2013, unchanged from September. The deficit of £9.7 billion on goods, partly offset by an estimated surplus of £7.1 billion on services. Yes, the march of the makers is picking up pace, momentum is “building”, investment plans will be brought back to the board room, just the trade figures alone will continue to disappoint, as the UK recovery gains pace. What happened to sterling? The pound closed at £1.6294 from £1.6346. Against the Euro, Sterling closed at €1.1856 from €1.1922. The dollar moved down up the yen closing at ¥103.2 from ¥102.8 and closing at 1.3740 from 1.3700 against the Euro. Sterling is on a rally which has led to a break out above £1.60, but €1.20 still presents significant overhead resistance. Oil Price Brent Crude closed at $108.83 from $111.61. The average price in December last year was almost $110, so no threat to inflation. Markets, US moved lower - The Dow closed at 15,755 from 16,020. The FTSE closed at 6,434 from 6,552. 7,000 FTSE now a tough call before Christmas. The markets still nervous until tapering finally begins. UK Ten year gilt yields closed at 2.90 from 2.91 US Treasury yields closed at 2.87 from 2.86. Yields will test the 3% level over the coming months but this will await the New Year. Gold closed at $1,239 from $1,231. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow and watch out for news of our Monthly Markets updates coming in the New Year. John Join the mailing list for The Saturday Economist or why not forward to a colleague or friend? © 2013 The Saturday Economist. John Ashcroft and Company, Dimensions of Strategy. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice. It's just for fun, what's not to like! Dr John Ashcroft is The Saturday Economist.

0 Comments

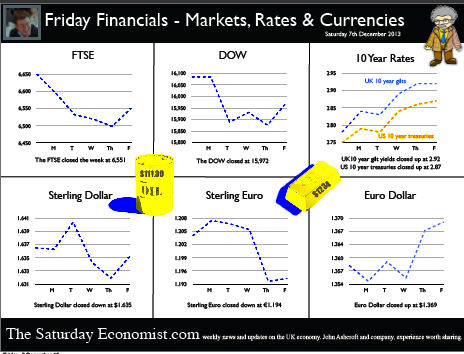

Economics news – fixing the roof whilst the sun is shining ... “Britain’s economic plan is working but the job is not done”, said Chancellor Osborne in the Autumn statement this week, “we need to secure the economy for the longer term”. Yes the Chancellor is intent on fixing the roof despite the sunny OBR outlook. The office for Budget Responsibility has revised up forecasts for the economy with growth of 1.4% expected this year and 2.4% next. Better still, borrowing is expected to fall significantly. The government is expected to borrow £111 billion this year, falling to to £96 billion next year, then down to £79 billion in 2015-16. By 2018-19, the OBR forecast the government will not have to borrow anything at all. Back from the brink of bankruptcy indeed. Growth is up, the deficit is down, unemployment is down, inflation is falling, spending will be kept under control, the government has an economic plan that is working. Who said the pasty tax was such a bad move? We even expect a much stronger performance from investment over the next two years. Just the trade figures alone will continue to disappoint. “Britain is currently growing faster than any other major advanced economy”, [which of itself will create a significant balance of payments problem for the UK economy]. "Exports are growing but they are not growing as fast as we would like", said the Chancellor. The Prime Minister’s visit to China this week is the latest step in this government’s determined plan to increase British exports to the faster growing emerging markets. We are even offering pig semen, to boost pork output in the Chinese economy apparently. So this Autumn Statement is fiscally neutral across the period. No giveaways. Government will ensure that debt continues to fall as a percentage of GDP. This means capping welfare to keep it under control and extending the working life to limit pension payments over the longer term. Business rates are to be capped, with some reduction in department spending to offset the revenue loss. The Bank levy will be increased slightly and the troops will be brought back from Afghanistan, saving lives and money in the process. All in all, this is a play it safe spending review, with a strong recovery in process. Fixing the roof, whilst the sun is shining. Yes, the sun has got his hat on and the Chancellor has a smile on his face” PMI Markit Surveys The good news continued from the PMI Markit Survey data this week, with manufacturing, construction and services all continuing to show strong growth. The recovery is extending across all sectors. Even the slow march of the makers will begin to pick up some speed this quarter. Over in the USA In the USA, growth figures for the third quarter reveal the economy grew by 1.8% year on year in real terms. The US economy will grow by around 1.8% this year, that’s actually faster than the UK but who would want to trouble an Autumn statement with facts. In the USA, more good news, unemployment data in the US fell faster than expected last month. 203,000 jobs were created in November pushing the unemployment rate down to 7%. Tapering is back on the agenda, with some speculation the cut back could begin this month. Courtesy would suggest the decision should await the move to Planet Janet in the New Year. Either way, tapering will begin soon and US base rate rises may be in prospect in 2015. What happened to sterling? The pound closed at £1.6346 from £1.6360. Against the Euro, Sterling closed at €1.1922 from €1.2045. The dollar moved down up the yen closing at ¥102.8 from ¥102.4 and closing at 1.3700 from 1.3582 against the Euro. Sterling is on a rally which has led to a break out above £1.60, but €1.20 still presents significant resistance. Oil Price Brent Crude closed at $111.61 from $109.65. The average price in December last year was almost $110. Markets, were tapered - The Dow closed at 16,020 from 16,086. The FTSE closed at 6,552 from 6,650. 7,000 FTSE now a tough call before Christmas. The markets are nervous until tapering begins. UK Ten year gilt yields closed at 2.91 from 2.78 US Treasury yields closed at 2.86 from 2.75. Yields will test the 3% level over the coming months but this may await the New Year. Gold closed at $1,231 from $1,252. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow and watch out for news of our Monthly Markets updates coming in the New Year. John Join the mailing list for The Saturday Economist or why not forward to a colleague or friend? © 2013 The Saturday Economist. John Ashcroft and Company, Dimensions of Strategy. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice. It's just for fun, what's not to like! Dr John Ashcroft is The Saturday Economist.

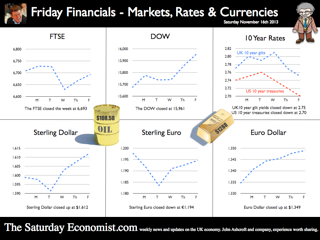

Economics news – you don’t have to be an optimist to see the glass is half full .. Yes it's the Inflation Report “You don’t have to be an optimist to see the glass is half full”, the opening remarks from Governor Carney’s Inflation Report presentation this week. The Governor went on to say, “the glass is half full and it will be filled”. A clear reference the recovery will be allowed to gain momentum before the Bank of England and the MPC will intervene “to take away the punch bowl” and begin the rise in base rates. The MPC are sticking with forward guidance. Rate rises will not even be considered until the level of unemployment hits 7% or even lower. [Subject to caveats on inflation expectations and market stability]. When will this be? In August the Bank assumed this would be in 2016 at the earliest. On Wednesday, the Governor admitted there was a 40% chance this could be by the end of 2014 with a 60% chance it would be by the end of 2015. Such has been the strength of the economics data over the last three months. Our own models assume the knock out unemployment rate will be hit by the third quarter of 2015. Thereafter rates may rise by around 50 basis points in short time. For the moment, the MPC are on a learning journey. The path of productivity, earnings, job creation and unemployment so unclear, we are all embarking on a “learning journey” suggested the governor. The £5m recently spent on the Bank of England model, of little value in the new world it would appear. Charlie Bean appeared most discomfited by the trip. Economics from Cambridge, a PhD from MIT and teaching at Stanford and LSE in the knowledge pack. One could be forgiven the reluctance to take the Mark Carney refresher course. But then why not? Having seriously failed to understand the impact of low rates on investment and depreciation on the trade balance, it is time to denounce the omniscient stance of the Oxbridge collective. Yes send them back to school. Martin Weale was indeed sent back to school this week. The MPC member was delivering a speech on the role of monetary policy and forward guidance to A-level students in London. “To cut a long story short, our job is to ensure that people buy coats when they need them”. Excellent. I am sure that cleared things up. Martin once worked in a shop apparently. Yes the black cloud gang disbanded, it’s back to school for all. Fill up your glasses, the punch bowl is on the table, the Carney Credit card is behind the bar. Inflation Good news for the Governor, inflation fell in October CPI to 2.2% from 2.7% in the prior month. Education hikes last year fell out of the index as we expected but the fall in transport costs pushed the index even lower. 2.4% CPI inflation was our call and still seems to be a reasonable target by the end of the year. Manufacturing prices suggest there is little cost pressure in the economy but retail energy prices are moving significantly higher. Retail Sales Retail sales figures in October were slightly disappointing, an increase of 1.8% in volume and 2.5% in value, slightly down on the averages in Q3. The demise of Barratts Shoes and Blockbuster a reminder, conditions remain tough on the high street as household real incomes remain under pressure. Internationally Janet Yellen, the new head at the Fed is still worried about the strength of the US recovery. Tapering may be postponed still later into the New Year. Growth in France and Japan in the third quarter a further warning the world recovery still requires accommodation. QE tapering US style is not the answer. Buying treasuries and Mortgage Backed Securities to support asset prices makes no sense. Blend a NASDAQ tracker fund into the purchase mix would follow the logic and demonstrate the folly. What happened to sterling? Sterling closed at £1.6113 from £1.6018. Against the Euro, Sterling closed at €1.1940 from €1.1982. The dollar moved up against the yen closing at ¥100.1 from ¥99.1 and closing at 1.3494 from 1.3368 against the Euro. Oil Price Brent Crude closed at $108.50 from $105.12. The average price in November last year was almost $110. We expect Brent Crude to average $110 in the month, with no material inflationary impact. Markets, pushed higher - The Dow closed at 15,962 up from 15,762. The FTSE closed at 6,693 from 6,708. UK Ten year gilt yields closed at 2.75 from 2.77 US Treasury yields closed at 2.70 from 2.75. Yields will test the 3% level over the coming months. Gold closed at $1,288 from $1,284. The bulls may have it may just have to wait for now. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow and watch out for news of our Friday Financials Feature with Monthly Markets updates coming soon. John Join the mailing list for The Saturday Economist or please forward to a colleague or friend. UK Economics news and analysis : no politics, no dogma, no polemics, just facts. © 2013 The Saturday Economist. John Ashcroft and Company, Dimensions of Strategy. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice. It's just for fun, what's not to like! Dr John Ashcroft is The Saturday Economist.

Economics news – news from Washington and Beijing ...

Washington Good news from across the Pond, a Washington truce has been achieved. The US government has returned to work, Yosemite National Park is open, international creditors will be paid. The debt crisis is over. A twenty week truce has been secured. Markets rallied, the dollar slipped, Google shares breached the $1,000 level and the S&P 500 hit a new high. What more could we ask? Beijing In China, growth continued at 7.8% into the third quarter up from 7.5% in the second. For those fearing a hard landing, crash landing, soft landing, end of the world scenario, it is time to stop shorting the markets and buy in, the world is not coming to an end any time soon. London - Mortgages In the UK, mortgage lending increased by 32% in the third quarter compared to Q3 last year. FLS and Help to Buy are boosting the market. We expect house prices to rise by 5% this year and almost 8% next year before a normalized escalation returns. Prices are beginning to rise across the UK. Yes Prices will move across the UK, like a tidal wave across the flood plain. Check out The Saturday Economist Housing Market Review for more information. Inflation Tuesday, the ONS released the latest inflation figures for September. CPI inflation was unchanged at 2.7% as RPI moved down slightly to 3.2% from 3.3%. We expect a further fall in CPI inflation around 30 basis points next month, as education fees drop out of the data series. Thereafter prices will be pretty sticky around 2.5%. Energy costs are set to rise and service sector inflation at 3.4% up from 3.0% last month will create problems for policy makers. As we have long pointed out, service sector inflation has averaged 3.7% for the last twenty years. Manufacturing prices Manufacturing Prices, on the other hand, have averaged around 1% over the same period, boosted by falls in clothing and footwear specifically. The immediate outlook for manufacturing prices is pretty benign, Output prices increased by just 1.2% in September and input costs increased by 1.1%, down from 5% in July. Retail sales Retail sales were also released this week. Retail sales volumes were up by 2.2% in September and by 2.4% in the third quarter. Sales values increased by almost 4% in the three months boosted by on line sales and department store sales. Is the housing market stimulating footfall? Quite probably. We expect the volume of housing transactions to increase significantly this year, boosting sales of carpets, furniture durables and DIY goods in the process. Employment The employment figures were also released this week. The claimant count fell by over 40,000 in September to a rate of 4% compared to 4.2% last month. The wider FLS count fell in the three months to August, to 2.87 million, a rate of 7.7% from 7.8% last month. Lagging as it does, the broader unemployment rate could fall to around 7.5% by the end of the year. The Bank of England “knock out rate” under forward guidance at 7% could be in sight by the end of 2014. So what of base rates? Interesting Spencer Dale the Bank of England’s chief economist was on Twitter this week in a hashtag #AskBoE “open hour” adventure. The telling tweet - a rate rise in 2014 was unlikely. Just as unlikely as a rate rise in 2016 no doubt. The markets expect a move in 2015 but will it wait until after polling day? We will have to ask next time the bank is online, perhaps using Facetime or Skype? What would Governor King have made of it all! So what does this all mean? The economy is recovering and growing at a much faster rate into the final quarter. The first estimate of GDP in Q3 will be released next week. We expect growth year on year to be over 1.5% rising to trend rate in the final quarter of the year. Inflation is falling, employment is rising, even the debt figures due next week will look much better. Energy costs may provide a problem for households but “wear a jumper”, the ministerial advice could keep bills down and boost retail sales in the process. What happened to sterling? Sterling moved up against the dollar and against the Euro as the dollar slipped. The pound closed at £1.6174 from $1.5954. Against the Euro, Sterling closed at €1.1816 from €1.1772. The dollar moved down against the yen closing at ¥97.7 from ¥98.5 and closing at 1.3682 against the Euro. Oil Price Brent Crude closed at $109.94 from $111.28. The average price in October last year was almost $112. We expect oil to average less than $112 in the month, with no inflationary impact. Markets, pushed higher - The Dow closed at 15,399 up from 15,237. The FTSE closed at 6,623 from 6,487. The US debt deal is done. The rally is on. UK Ten year gilt yields closed at 2.72 from 2.74, US Treasury yields closed at 2.58 from 2.69. Gold closed at $1,313 from $1,270. The bulls have it, at least for the week. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow. Join the mailing list for The Saturday Economist or please forward to a colleague or friend. UK Economics news and analysis : no politics, no dogma, no polemics, just facts. John © 2013 The Saturday Economist. John Ashcroft and Company, Dimensions of Strategy. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice. It's just for fun, what's not to like! Dr John Ashcroft is The Saturday Economist If you do not wish to receive any further Saturday Economist updates, please unsubscribe using the buttons below. If you enjoy the content, why not forward to colleague or friend.  Economics news – inflation falls, no boom in the housing market, good news on borrowing, Chancellor Osborne is ticking the right boxes this week ...

Inflation - Retail Prices The rate of inflation slowed to 2.7% in August compared to 2.8% in July. We expect a further significant fall next month and by the end of the year the inflation rate should be around 2.4%. Thereafter prices could be a little sticky. Service sector inflation was 3% in August and goods inflation was 2.4% in the latest monthly data. Inflation - Manufacturing Prices The good news on inflation was also manifest in the manufacturing sector. Output prices increased by just 1.6% compared to 2.1% in July. Input costs for manufacturers also fell back from 5% in July to 2.8%. Part of the reason for the slow down was oil and energy costs. The average price of oil in August was $111 dollars per barrel, slightly down on the same period last year. The rate of wages and earnings growth remains subdued, presenting a benign outlook for inflation over the short term. At close this week Brent Crude was trading at $109 dollars per barrel. The outlook for manufacturing inflation is pretty benign. House Prices - ONS data For those wary of a housing boom, the ONS also released the House Price Index in July. In the 12 months to July 2013 UK house prices increased by 3.3%, up from a 3.1% increase in the 12 months to June 2013. Signs of a national boom? Not really but certainly signs of a good recovery! Annual house price increases in England were driven by London (9.7%) and the South East (2.6%). Excluding London and the South East, UK house prices increased by just 0.8%. In the North West, prices actually fell by almost 1%. The RICS has made the call for a peg on prices around 5%. This to reflect a normalised earnings growth rate of 3% plus a supply side restraint adjustment to stimulate additional investment presumably. Would this work nationally? Obviously not. But some consideration to mortgage rationing on a regional basis especially in the South East may gain political if not market traction. Retail Sales August - A further indication, the recovery is on track with no signs of a runaway boom in prospect... Retail Sales in August were up by 2.1% in volume and 3.6% by value compared to August last year. Internet sales were up by 22% in the month accounting for 10% of all retail sales. Trading is better but not that much. With online trends and large store consolidation, life for most retailers is tough. Government Borrowing Further good news for the Chancellor, the level of borrowing fell in August. We expect further significant falls before the end of the financial year. In August 2013, public sector net borrowing excluding temporary effects of financial interventions (PSNB ex) was £13.2 billion. This was £1.3 billion lower than in August 2012 when it was £14.4 billion. The Chancellor is on track for a significant fall in borrowing this year. We expect the level of borrowing excluding interventions and transfers to fall to around £105 billion compared to a revised £115 billion last year. Car Manufacturing Car output increased by 16% in August bring the year to date output growth to 3%. More good news but the August headline should be kept in perspective. The year to date total is the better trend guide and let’s not forget commercial vehicle output is down in the year by 17%. Tapering USA Despite clear indications “Tapering” may begin in the Fall, the Fed decided to continue the process of QE, purchasing mortgage backed securities at a pace of $40 billion per month and longer term Treasury securities at the rate of $45 billion per month, this week. What does this mean for US and UK interest rates? Not much in the short term. Check out the Saturday Economist Special Post "No tapering, more tampering, leads to more questions than answers at the Fed". Assessing market reaction over the week, Bernanke fires a blank would have a more appropriate headline. What happened to sterling? Sterling responded to the news on tapering, moving up against the dollar but down against the Euro. The pound closed at $1.5994 from $1.5871 having tested the 1.60 level intra week. Against the Euro, Sterling closed down at €1.1824 from €1.1940. The dollar moved little against the yen closing at ¥99.3 from ¥99.4 Oil Price Brent Crude closed at $109 from $111. The average price in September last year was almost $113. We expect oil to average $110 in the current quarter, with no real inflationary impact. Markets, rallied - The Dow closed up at 15,451 from 15,376 . The FTSE closed up at 6,596 from 6,584. The Fed statement this month was a mis fire non event. We still think the FTSE will clear 7000 within ten weeks and the DOW will press 16,000. UK Ten year gilt yields closed at 2.92 from 2.94, US Treasury yields closed at 2.79 from 2.89. The fed statement this week pulled long rates down by just 12 basis points. Long rates are decoupling from shorts, returning to fair value. They are just a bit reluctant to leave, with pleas from the FOMC to “stick around”! Gold closed at $1,331 from $1,312. The bulls have it or do they? The news on tapering bought some upside gain but not much, we think gold will trade sideways for some time. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow. Join the mailing list for The Saturday Economist or forward to a friend UK Economics news and analysis : no politics, no dogma, no polemics, just facts. John © 2013 The Saturday Economist. John Ashcroft and Company, Dimensions of Strategy . The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice.  Good news for the economy continued this week.

A fall in the rate of unemployment AND an increase in output and orders for the construction industry. Who would believe it was just a few months ago headlines were devoted to the risk of a triple dip recession? The year is becoming a tale of two halves with a significant pick up in activity and sentiment into the third quarter. Get ready, we are leaving Planet ZIRP. Speed bumps in the housing market It is a strange recovery with strange roles in evidence. The Bank of England is hoping to keep base rates on hold for three years. The RICS warned this week of the need to maintain a stable and sustainable path for house prices. “We suggest setting an annual growth rate threshold in a national index, which if exceeded, triggers tighter macro prudential policy” said Josh Miller Senior Economist in the RICS report. The RICS is advocating “speed bumps” to limit the rate of price increases. The Bank of England (in the form of the FPC) should intervene to regulate mortgage allocations of LTV ratios across the UK if prices moved over 5%. That sort of thing. “Taking away the punch bowl as the party gets started” is the traditional role of the central banker. Now some of the heavy drinkers are suggesting, we dilute the hooch. How strange. Most commentators have reacted badly to the suggestion. Why 5%? Is there a regional variation? Is it the same for maisonettes and mansions? Should the government confiscate revenues where prices exceed the guidelines? Are the RICS advocating a prices and incomes board, monitored by the RICS perhaps? Graeme Leach at the IOD has suggested it is a “statist solution to a state created problem”. Calm down Graeme, it was just for fun and not to be taken too seriously. The FPC is to meet this week. Top of the agenda will be the need to limit loan to value ratios. The government “homes for heroes” scheme, (the scheme in which the tax payer underwrites high loan values for house buyers) will be on the agenda no doubt. Unemployment The unemployment rate ticked down in July to 7.7% in July. The claimant count fell to 4.2% in August. The number of claimants - down by 32,000 to 1.4 million. Further indicators the recovery is on track, towards trend rate of growth, into the final quarter. What does this mean for forward guidance? The models still suggest it will be the end of 2015 at least before the 7% threshold will be reached. That is the rate at which the MPC will begin to think about base rate rises, (speed bumps and knock out drops aside). The caveat about earnings continues. The recovery cannot be sustained without a change in household fortunes, either lower inflation or higher earnings growth is required. Plus, the UK cannot grow at a faster rate then Europe for too long, without the trade deficit coming under severe pressure. The trade deficit, of itself, “a speed bump or pothole”, where growth is concerned. Construction Good news on construction. Output increased in July by 2% compared to July last year. Orders for new work, especially in the housing market, were up by 33% compared to the same time last year. This is an important change indicator for the sector. Overall the growth in services continues. The recovery in manufacturing and construction will look much stronger into the final quarter of the year. The UK recovery is on track. It is just over eighteen months to the election. Buckle up, we are leaving Planet ZIRP. Gilts are already in low orbit. What happened to sterling? Sterling responded to the economics news, moving up against the dollar and also against the Euro. The pound closed at $1.5871 from $1.5627 and at €1.1940 from €1.1860 against the euro. The dollar moved up against the yen closing at ¥99.4 from ¥99.0 Oil Price Brent Crude closed at $111 from $114. The average price in September last year was almost $113. We expect oil to average $112 in the current quarter, with no real inflationary impact. Markets, rallied - The Dow closed up at 15,376 from 14,923. The FTSE closed up at 6,584 from 6,547. The Fed statement this month will mark the larger DOW move. Still a good time to move in? The FTSE will clear 7000 within ten weeks and the DOW will press 16,000. UK Ten year gilt yields closed at 2.94 from 2.95, US Treasury yields closed at 2.89 from 2.93. Long rates are decoupling from shorts, returning to fair value. They are just a bit reluctant to leave! Gold closed at $1,312 from $1,388. The bulls have it or do they? Some still worry about tapering. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow. Join the mailing list for The Saturday Economist or forward to a friend UK Economics news and analysis : no politics, no dogma, no polemics, just facts. John © 2013 The Saturday Economist. John Ashcroft and Company, Dimensions of Strategy . The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice.  Economics news – for a further week, the good news keeps on coming ... falling inflation, a fall in unemployment plus a boost to retail sales in July ...

Inflation figures were reported on Tuesday. The CPI inflation index fell to 2.8% in July from 2.9% in the prior month. By the end of the year we expect inflation to fall below the 2.5% threshold but the 2% target will be elusive for many months if not years ahead. In October the hefty tuition fees will fall out of the index providing a drop of 20 - 30 basis points. The 2% target will be a challenge - goods inflation averaged 2.4% and service sector inflation averaged 3.1%. Bad news for rail travelers, the rail fares will be indexed to RPI plus 1%. A 4.1% increase in fares is in prospect for 2014, placing additional pressure on retail prices and disposable incomes. The unemployment picture continues to improve, for those who can find work at least. The claimant count fell by 29,000, to a rate of 4.3% in July. The wider LFS data suggests a more modest fall in the three months to June. The rate of unemployment at 7.8% was unchanged, still way above the 7% threshold that may signal a change in monetary policy. Retail sales volumes increased by 3% in July as sunshine and consumer confidence provoked a spending rush, stimulated by sunny weather, a Murray win at Wimbledon and the Royal baby allegedly. Sunny weather boosted sales across a range of products including food, alcohol, clothing and outdoor items. By value retail sales increased by almost 5%. After a slow start to the year, the retail outlook has improved in the summer months. Will this continue? Why not! Employment is increasing and earnings are improving. A further 400,000 are in work compared to this time last year and earnings increased by 2% in the three months to June. We expect the retail rally to continue, though perhaps not at the 3% rate for the rest of the year. Housing - The big story continues to be the housing market. Prices are rising, mortgage activity is increasing, the help to buy scheme is providing a boost to first time buyers. New home build is set to increase by almost 30% this year. The housing market is on the move, time to lock up your fixed rates, as prices rise, the real cost of borrowing is zero, capital appreciation - the bonus. So what does this mean for the year? Our forecast is for growth of around 1.2% plus, rising to 2% in 2014. The economy has turned, the real risk - monetary policy is behind the curve. It is difficult to believe rates will be kept on hold until 2016, watch the US and add six months the best guide as always. Markets were equally sceptical, gilts and treasury yields are rising - gold is beginning to glitter again. What happened to sterling? Sterling responded to the economics news, moving higher. The pound closed at $1.5633, from $1.5505 against the dollar and at €1.1713 from €1.1617 against the euro. The dollar up against the yen closing at ¥97.5 from ¥96.24 Oil Price Brent Crude closed up at $110.40 from $108.22. The average price in August last year was almost $115. We expect oil to average $112 in the current quarter. Markets, were troubled - The Dow fell to 15,081 from 15,425. The FTSE closed down at 6.499.99 from 6,583. It’s a chance for market makers to clean out the bear pit. A good time to make a move. We still think the FTSE will clear 7000 within ten weeks. UK Ten year gilt yields closed at 2.72 from 2.45, US Treasury yields closed up at 2.83 from 2.58. Yields are moving higher, despite the wishes of central bankers. The name is Carney not Canute after all. Gold closed up at $1,377 from $1,315. Still waiting for the next big move but which way? Last week we said, the arguments are building for the bulls. It looks like they have made a decision. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow. Check out The Saturday Economist web site, and the new Chart of the Day Page. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow. The Saturday Economist.com is mobile friendly, no need for a special app any more! Join the mailing list for The Saturday Economist or forward to a friend to let them share the fun! John John Ashcroft is the Saturday Economist, Chief Economist at the Greater Manchester Chamber of Commerce, Economics Adviser to Duff & Phelps and Chief Executive of pro.manchester. The views expressed are personal and in no way reflect the policy statements of organisations with which we work. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice. It's just for fun, what's not to like! Dr John Ashcroft is The Saturday Economist.  In the service sector, manufacturing , construction and housing, the news is good news...

The August Inflation Report was presented this month by Mark Carney, the new Governor of the Bank of England. The Bank is forecasting growth of almost 1.5% this year and 2.5% next. Inflation will remain above target but base rates may be kept on hold for a further three years. So much for forward guidance. The time may come when the central banker "will take away the punchbowl" but for the moment Carney is "putting his credit card behind the bar". Enjoy. Business activity in the service sector increased in July at fastest rate since late 2006 according to the latest survey data*. The headline Business Activity Index climbed to its highest reading since December 2006, posting 60.2 up from 56.9 in June. Above 50.0 readings have now been recorded for seven months in a row, with growth accelerating continuously throughout this period. *Markit/CIPS UK Services PMI® data. In the manufacturing sector, output was up by 2% in June compared to prior year after a disappointing first half. Capital goods, continue to drive recovery with strong growth of almost 4%. Consumer goods also rallied in June with output of consumer durables increasing by 2%. In construction, output in the second quarter was estimated to be 1.4% higher when compared with Q1 2013. Comparing Q2 2013 with the same period a year ago, construction output actually fell by 0.5%. We expect a further recovery in output into the second half with growth of 1% year on year, boosted by some housing activity. On trade, the deficit on trade in goods reduced to £24.9 billion in Q2 2013 from £26.5 billion in the first quarter. Exports of goods in the second quarter of 2013 reached £78.4 billion, the highest on record. Imports of goods also increased in Q2 2013 to £103.3 billion. Seasonally adjusted, the UK’s deficit on trade in goods and services was estimated to have been £1.5 billion in June, compared with a deficit of £2.6 billion in May. The deficit of £8.1 billion on goods, was offset by an estimated surplus of £6.5 billion on services. So what does this mean for the year ahead? We still expect the deficit trade in goods to increase to £105 billion in the year. Exports of goods will improve as world trade recovers but imports will increase to meet the improving demand in the domestic economy. The service sector will continue to drive recovery with a trend rate accelerating from 1.5% to 2% over the next six months. Manufacturing and construction output will improve in the second half but contribution to growth for the year will be muted following such a poor start. Our forecast for growth this year is around 1.2% with further growth in 2014 of around 2%. Slightly more bearish than the “Bank”. For the moment, the good news keeps on coming, a sustained recovery will require a growth in real household incomes. In the housing market, the Halifax reported prices increasing by almost 5% in July. There is little sign of a great change in the volume of activity for the moment, although the Council of Mortgage Lenders reported a strong recovery in buy to let activity. Lenders advanced 40,000 mortgages, worth £5.1 billion, to buy-to-let investors in the second quarter of 2013. Both the number of buy-to-let loans, and the value of lending, were the highest since the third quarter of 2008. The promise of low rates will push prices higher as the real cost of borrowing falls. Strong rental yields, low costs of borrowing and the prospects of capital appreciation present a heady cocktail for buy to let. More pressure on first time buyers, the real price of life on planet ZIRP. What happened to sterling? Sterling responded to forward guidance, moving higher. The pound closed at $1.5505 from $1.5284 against the dollar and €1.1617 from €1.1504 against the euro. The dollar slipped against the yen closing at ¥96.24 Oil Price Brent Crude closed largely unchanged at $108.22 from $108.95. The average price in August last year was almost $115. Not much pressure on price as we move into the Autumn. Markets, were up - The Dow fell to 15,425 from 15,658. The FTSE closed down slightly to 6,583 from 6,648. Markets trade softly into August. Still a good time to average in. The FTSE will clear 7000 within ten weeks. UK Ten year gilt yields closed at 2.45 from 2.42, US Treasury yields closed down at 2.58 from 2.60. Yields are set to move higher but the path will be slow, we remain parked on the runway of Planet ZIRP, the pilot has gone off the to pub. Gold closed down at $1,315 from $1,308. Still waiting for the next big move but which way? The arguments are building for the bulls. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow. Check out The Saturday Economist web site, and the new Chart of the Day Page. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow. The Saturday Economist.com is mobile friendly, no need for a special app any more! Join the mailing list for The Saturday Economist or forward to a friend to let them share the fun! John John Ashcroft is the Saturday Economist, Chief Economist at the Greater Manchester Chamber of Commerce, Economics Adviser to Duff & Phelps and Chief Executive of pro.manchester. The views expressed are personal and in no way reflect the policy statements of organisations with which we work. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice. It's just for fun, what's not to like! Dr John Ashcroft is The Saturday Economist.  7% unemployment and 2.5% the inflation the thresholds - rates may be on hold until 2016.

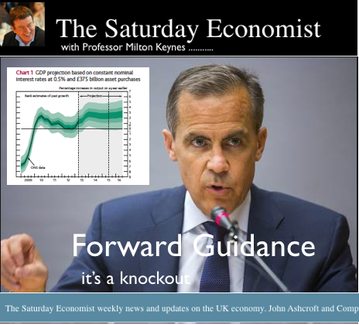

The Bank of England released its quarterly inflation report, the first since Governor Mark Carney assumed the role of Governor. The report presents a more optimistic view of the UK’s growth prospects following a batch of recent good news on the economy. The MPC increased the GDP growth forecast for this year to around 1.5% increasing the 2014 forecast to around 2.5%. Consumer price inflation is likely to fall back to 2.0% but not for some time yet. It could be 2015 before inflation falls back to target and then some, 2.5% is the new threshold target for CPI inflation. Governor Carney introduced the first every version of "Forward Guidance" linking a change in monetary policy to the rate of unemployment. In particular, the MPC intends not to raise Bank Rate from the current level of 0.5% at least until the Labour Force Survey headline measure of the unemployment rate has fallen to a level of 7%. On current projections, this is unlikely to occur until 2016, inline with forward market forecasts on base rates. Is this an unconditional commitment? No. The Old Lady of Threadneedle Street will exercise the prerogative to change her mind subject to certain conditions. The guidance linking Bank Rate to the unemployment threshold would cease to hold if any of the following three ‘knockouts’ were breached: In the MPC’s view, CPI inflation 18 to 24 months ahead will be 0.5 percentage points or more above the 2% target. Medium-term inflation expectations no longer remain sufficiently well anchored and the Financial Policy Committee (FPC) judges that the stance of monetary policy poses a significant threat to financial stability. What does that mean? We can’t be sure. The intention is to suggest rates will be held until the recovery is well developed and “escape velocity” from recession has been achieved. The MPC would have us believe this is 2016. The risk is that inflation will remain above target as the recovery gains momentum and the MPC will be forced to raise rates before the suggested 2016 timeline. It is a knock out start by Mark Carney. The economy is recovering, rates will be held for the next twelve to eighteen months at least. Forward guidance has made a promising start. Let’s hope it does not provide too much mis direction. For now enjoy the recovery. Bank of England inflation report, August 2013 7th August 2013  “Regarding the Bank Rate and the stock of asset purchases, the Committee voted unanimously in favour of the proposition that base rates and Quantitative Easing (QE) should be kept on hold. The Governor had "invited the Committee to vote on the propositions that Bank Rate should be maintained at 0.5% and the Bank of England should maintain the stock of asset purchases at £375 billion". The MPC were united as Carney called time on QE.

“And so the period of Quantitative Easing draws to a close, as an experiment in monetary policy. David Miles [MPC member] and Paul Tucker [Deputy Governor Responsible for Financial Stability] fell into line with the “new reality”. The pair had been the two QE stalwarts who had “stuck it out” with Mervyn King right to the end of the line. With the economy recovering and inflation rising, it was time to say goodbye to QE. A farewell stimulated by the arrival of the new Governor. “Earlier this week, Paul Fisher, Head of Markets at the Bank of England, gave evidence to the Treasury Select Committee. Fisher suggested any unwinding of monetary stimulus was likely to be years in the future. No need to worry about the unwinding of QE, the gilts will be held to redemption and like old soldiers will fade away, into the ghostly shadows of public sector accounting. “Paul Fisher also confirmed that market expectations of rate rises was much sooner than the Bank might expect. The MPC would like markets to believe base rates will not rise until 2016. We shall await the notes on forward guidance in August for more information on this. For the moment, rejoice, QE is dead, it ran out of funding and intellectual currency a long time ago.” - See more at: http://www.gmchamber.co.uk/stories/committee-united-on-quantitative-easing#sthash.Z3vxUJnC.dpuf |

The Saturday EconomistAuthorJohn Ashcroft publishes the Saturday Economist. Join the mailing list for updates on the UK and World Economy. Archives

May 2024

Categories

All

|

| The Saturday Economist |

RSS Feed

RSS Feed

The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The presentation should not be construed as the giving of investment advice.

|

The Saturday Economist, weekly updates on the UK economy.

Sign Up Now! Stay Up To Date! | Privacy Policy | Terms and Conditions | |