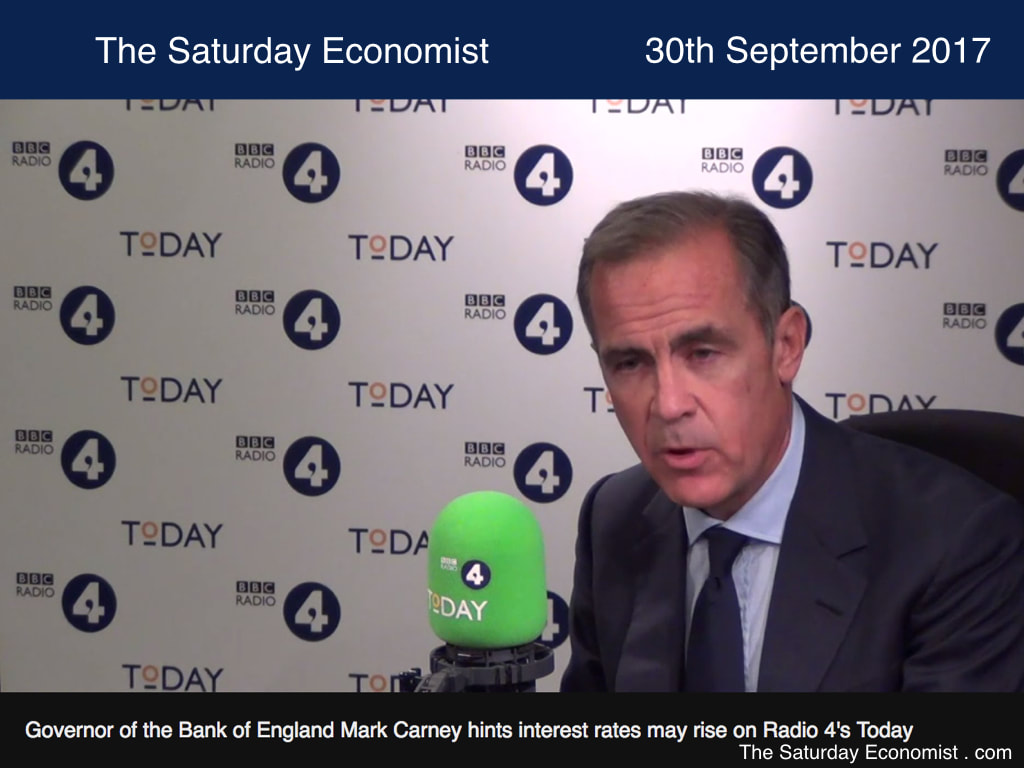

The Governor was on Radio 4 this week. Interest rates could rise in the "Relatively Near Term" Mark Carney explained. It was time for the Bank to "ease it's foot off the accelerator". Taking away the punch bowl to avoid a drink driving offence, presumably... could the rate rise be as early as November?

"If the economy continues on the track that it has been on, and all indications are that it is, in the relatively near term we can expect that interest rates will increase," he said. Ironic, on the same day, the ONS revealed the latest estimates of growth in the economy. The U.K. economy grew by 1.6% last year, compared to the 1.8% last estimated. The downward revisions continued into 2017. Growth in the second quarter was revised down to 1.5% from 1.7% earlier. The economy appears to be slowing, the Bank is threatening to hike rates. Does that make sense? Perhaps. The Governor is seeking to return rates to the "Status Quo Ante Referendum". A 25 basis points rise would reverse the mistake of August last year. For the moment, further rises will be small and gradual, despite the concerns about bank lending and household borrowing. Here too, there was some good news for monetary policy. The household savings ratio bounced back in the second quarter. The ONS had previously estimated this had fallen to a record low of 1.7%. That always looked like an errant outlier. The fall supported the proposition households were financing consumption by saving less and borrowing more. The savings figure has now been revised up. The Q2 estimate is now over 5%. Should the Bank relax? "What we are worried about, is a pocket of risk. A risk in consumer debt, credit card debt, debt for cars and debt for personal loans" Carney told BBC Radio 4's Today Programme. That is not the Bank of England's fault. "Banks had not been as disciplined as the should be in their underwriting standards and pricing of the debt." Oh dear. So much for regulatory control. As for pricing, banks will take their lead from base rate plus. Life on Planet ZIRP can lead to a heady cocktail of mispricing of loans and asset prices after all. It really is time to plan for take off, despite the apparent sluggish growth in truly global Britain.

0 Comments

Theresa May was in Florence this week. Plastering the cracks in the city of Renaissance, that's a tough job. Johnson and Hammond were on hand to ensure the Prime Minister held the centre line. No tilt too far, to hard or soft Brexit. This was Florence and not Pisa after all. No leaning tower, just an upright delivery of the olive branch to Brussels. The PM had one eye on Brussels and the other on Manchester. The Tory party conference looms. Difficult to plaster the cracks on the front and back benches. Brexit means Brexit, albeit now in 2021, five years after the referendum result. "The eyes of the world are upon us, at a critical time in this defining moment of a vibrant debate, as we begin a new chapter for truly global Britain". "Shared history, shared challenges, shared future". Yes waffles in the land of pizza and pasta. "The next few years are going to be an exciting time" said the Prime Minister. Just over 5,000 words with little content, were hardly reassuring. "The UK has never totally felt at home in the European Union." You speak for yourself Theresa. We know those jingoistic crackpots in the Tory Party never were. I just enjoyed a pleasant holiday in Sicily, resenting the fact that £106 quid was extracted from my current account in Manchester, to deliver €100 euros from an ATM in Naxos. So much for parity! Anyway, back to Florence. Good news there will be a two year transition period once negotiations have been finalized. The U.K will stay in the single market and in the customs union. We will pay to stay. We accept, bills must be paid before talks about trade. We will guarantee the rights of EU citizens, subject to the rule of law and the European Court of Justice. "We love you" the PM said. Your status will be sorted out "quickly" as a top priority. The speech was a bit short on detail. We already know that Ireland has "unique issues" which will need to be addressed said the PM. Interesting but hardly original. I think Oliver Cromwell said it first. Cromwell also said "Depart I say and be done with you". It sounds even better in French. €40 billion euros is the offer. The Irish jig has just begun. Brussels will accept the opening bid, then ask for more. The Conservative Conference may not even accept the opening stance. Boris Johnson was not in Italy to endorse the Prime Minister, he was merely taking notes, witnessing the Betrayal of the Brexiteers … So what of borrowing ...? Good news for the Chancellor this week. Borrowing in August was just £5.7 billion, over £2 billion lower than prior year. The year to date total was £28.3 billion slightly lower than prior year. The Chancellor has some room for manoeuvre in the Autumn budget but not much. Public sector debt (excluding public sector banks) was £1.8 trillion at the end of August, equivalent to 88.0% of GDP. This was an increase of £150.9 billion on the same period last year. Moody's, the credit agency were not impressed. The UK was downgraded to Aa2. "Leaving the European Union was creating economic uncertainty at a time when the UK's debt reduction plans were already off course". Her Majesty's Treasury was displeased. Downing Street said the EU view was outdated. A reference to the credit agency of course and not the Tory backbenches. The Retail Sales Boom Continues ... Retail sales in August were up by 5.6% in value terms and 2.4% in volume. Online sales increased by over 15% again. No real signs of a household income squeeze and a hit to spending. The pound in your pocket may be shrinking as inflation increases but the tills are still ringing. Base rates at 0.25% are incompatible with such strong growth in spending. Will the Bank move before the end of the year? The odds have just increased. In the U.S. the Fed remains on track to increase rates again in December. The Federal Reserve has called time in the $4.5 trillion bond buying spree. The final tranche will be purchased this month. Janet Yellen has called an end to the QE experiment . We were never sure what it achieved anyway, apart from creating the biggest bond bubble in history, set to pop and soon. “It’s pretty clear that QE works in terms of having the expected impact on bond-market yields, and on asset prices more generally,” former Fed Governor Jeremy Stein said . While it’s a “bit of a leap to conclude that it also stimulates” the economy". "Does The Fed Even Know If QE worked", the headline in the Wall Street Journal this week, the academic debate may run and run but we knew from the outset and said so! John That's all for this week. Have a great week-end ... © 2017 John Ashcroft, Economics, Strategy and Social Media, experience worth sharing. ______________________________________________________________________________________________________________ The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of advice relating to finance or investment. ______________________________________________________________________________________________________________ If you do not wish to receive any further Saturday Economist updates, please unsubscribe using the buttons below or drop me an email at [email protected]. If you enjoy the content, why not forward to a friend, they can sign up here ... _______________________________________________________________________________________ For details of our Privacy Policy and our Terms and Conditions check out our main web site. John Ashcroft and Company.com  The MPC voted to keep rates on hold this week. Just two members voted to hike rates. Seven members voted to keep rates on hold. No change from prior month.

So when will interest rates rise? It's like waiting at the bus stop, for a bus that's two days late. You know it's going to come eventually. You just can't be sure when. We have been waiting at the bus stop in Threadneedle Street for some years now. Churlish to talk of forward guidance and the 7% unemployment trigger rate. That bus passed by with the "out of service" sign some years ago. So why the excitement this week? Sterling rallied against the euro/dollar as market expectations of an increase in base rates heightened. Despite the decision to hold rates on Thursday, Sterling is trading at over $1.35 against the dollar and testing €1.20 against the Euro. It all began with the closing statement from the Governor on Thursday. "Monetary policy could need to be tightened by a somewhat greater extent over the forecast period than current market expectations". Traders arose from slumbers, to go long Sterling. It doesn't take much to wake up the queue. The bus is coming, it could be here within the hour. The came the speech on Friday from Gertjan Vlieghe at the SBE Conference in London. "The appropriate time for a rise in Bank Rate might be as early as in the coming months". Crikey. A dove squawked in SE1. The bus is around the corner. Check your tickets and grab a ride. The push to parity is off the trading floor. Sterling is the currency of choice at least for now. Well certainly for the week-end. The rally looks a little over extended to say the least. The bus may be a bit later after all. In the U.S. sluggish retail sales in August could push any Fed move into 2018. The rally in Sterling may just be enough to take the edge off prices in the short term. The Bank expects inflation to rise to over 3% CPI basis before Christmas. The unreliable boyfriend may just be flirting with the markets again. The push to parity against the Euro, was too much even for the normally indifferent Old Lady of Threadneedle Street.. Gertjan Vlieghe may talk of a rate rise in the coming months ... let's not forget there are many months to come! Don't bank on a ride before Christmas ... So what of inflation ...? Inflation CPI basis hit 2.9% in August up from 2.6% prior month. RPI inflation was 3.9%. Do we really think such high levels of inflation are compatible with base rates on hold at 0.25%? Goods inflation CPI was up to 3.1%. Service sector inflation was 2.7%. Producer prices rose slightly to 3.4%. Input costs edged up to 7.6%. The shock from the oil price rally, compounded by Sterling depreciation should be working out of the system by now. The August data suggests there is more inflation in the pipeline. Our models suggest the worst of the short rise is over. The Bank expects prices to peak at over 3% in the coming months. Does this mean the bus is coming after all? No time to leave the queue. Maybe time to push back in the queue, if you are over a few pounds over weight this weekend. Strong jobs data, weak earnings ... The latest data on employment was released this week. Almost 400,000 jobs have been created over the last twelve months. The unemployment rate fell to 4.3%. The ratio of unemploymemt to vacancies hit 1.9. Recruitment difficulties are increasing. Earnings continue to defy economics. The latest data suggest pay growth of just over 2% overall with real incomes under pressure as prices rise. The release of the public pay cap will lead to an increase in overall pay levels. The augmentation of pay will exacerbate underlying price pressure. A pay rise for every one is another "omnibus" around the corner ... Don't Miss the Economics Conference on the 13th October. Our theme is the Economics of Greater Manchester. We will be talking about the Inclusive Growth Challenge, Balancing the Books and the Sectors Driving Growth in the City Region! Another Great Conference in the pro-manchester series . We have a great line up of speakers announced this week. Book Now Don't Miss Out ... John That's all for this week. Have a great week-end ... John Thanks for your feedback on the Saturday Economist. Here's what you are saying about the weekly update! Don't forget to join the club, with access to the library, FAQs, Detailed Bulletins and Special Deals ... © 2017 John Ashcroft, Economics, Strategy and Social Media, experience worth sharing. ______________________________________________________________________________________________________________ The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of advice relating to finance or investment. ______________________________________________________________________________________________________________ If you do not wish to receive any further Saturday Economist updates, please unsubscribe using the buttons below or drop me an email at [email protected]. If you enjoy the content, why not forward to a friend, they can sign up here ... _______________________________________________________________________________________ For details of our Privacy Policy and our Terms and Conditions check out our main web site. John Ashcroft and Company.com _______________________________________________________________________________________________________________ Copyright © 2017 The Saturday Economist, All rights reserved. You are receiving this email as a member of the Saturday Economist Mailing List or the Dimensions of Strategy List. You may have joined the list from Linkedin, Facebook Google+ or one of the related web sites. Our mailing address is: The Saturday Economist, Tower 12, Spinningfields, Manchester, M3 3BZ, United Kingdom.  Manufacturing Rally ... Are Car Makers Driving Growth?

Manufacturing output increased in July according to the latest data from the ONS. The year on year increase was 1.9%, a strong rally from the dismal performance in the second quarter. Transport output increased by almost 8% in the month. The SMMT reported an 8% increase in car manufacturing in July, by way of explanation. In August, it just got bettter! According to the Markit/CIPS manufacturing survey, growth in the sector gathered pace as new order inflows increased. Domestic demand was the prime source of new contract wins. Growth in Europe and the rest of the world, is also stimulating demand. Should we get too excited? Not really. We expected a strong performance in the third quarter, softening towards the end of the year. Car output is down by almost 2% year to date. We expect U.K. registrations to fall by 2.5% this year. The domestic market was a contributing source of the surge in July, up by 18% year on year. For the year as a whole we expect manufacturing output to increase by 1.5%, up from less than 1% last year. Better than last year but no real "march of the makers" re balancing the economy. So what of Construction? Construction output was flat in July. Strong growth in housing, including public sector housing, was offset by weakness in infrastructure and other public sector projects. Private sector investment in commercial property continues to offset significant weakness in industrial projects. It has been a similar story throughout the year. For the year as a whole we expect construction growth of around 1.4%, down from 2.4% last year. Unless and until the government commits to real infrastucture expansion, construction will remain subdued into 2018. House Prices ... rise and fall on Planet ZIRP ... The rate of house price increases fell in August, according to Nationwide. The rate of increase fell in the month to 2.1% from 2.9% prior month. Should we worry about a house price collapse? Not really! According to the Halifax House price index, house prices increased by 2.6% in August, up from 2.1% in July. New mortgage applications suggest underlying demand strength in the market. "House prices should continue to be supported by low mortgage rates and a continuing shortage of properties for sale", according to Russell Gailey, Managing Director of the Halifax Community Bank. We expect the overall rate of house price inflation to average 2.4% in the final quarter, down from 6.4% last year. The issue driving the slow down is affordability. The price to earnings ratio is critical over the medium term. Earnings growth of 2.4% is incompatible with a 6.4% growth in house prices on a continuing basis. The Nationwide house price to earnings ratio is over six. The long term average [1987 -2017] is around 4.3. On Planet ZIRP, post 2008, the average has been around 5.5. Yes QE and low rates boost asset prices! For those hoping for the kids to leave home, leaving Planet ZIRP, will aid the exodus. Higher base rates may lead to higher mortgage costs. The irony is affordability will improve as higher asset prices, including housing are brought back within the confines of market reality! Don't Miss the Economics Conference on the 13th October. Our theme is the Economics of Greater Manchester. We will be talking about the Inclusive Growth Challenge, Balancing the Books and the Sectors Driving Growth in the City Region! Another Great Conference in the pro-manchester series . We have a great line up of speakers announced this week. Book Now Don't Miss Out ... John That's all for this week. Have a great week-end ... John Thanks for your feedback on the Saturday Economist. Here's what you are saying about the weekly update! Don't forget to join the club, with access to the library, FAQs, Detailed Bulletins and Special Deals ... © 2017 John Ashcroft, Economics, Strategy and Social Media, experience worth sharing. ______________________________________________________________________________________________________________ The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of advice relating to finance or investment. ______________________________________________________________________________________________________________ For details of our Privacy Policy and our Terms and Conditions check out our main web site. John Ashcroft and Company.com _______________________________________________________________________________________________________________ Copyright © 2017 The Saturday Economist, All rights reserved. You are receiving this email as a member of the Saturday Economist Mailing List or the Dimensions of Strategy List. You may have joined the list from Linkedin, Facebook Google+ or one of the related web sites. Our mailing address is: The Saturday Economist, Tower 12, Spinningfields, Manchester, M3 3BZ, United Kingdom.  Michael Saunders ... A Hawk in the Park ...

Michael Saunders was in Cardiff this week. The external member of the Bank of England MPC explained why he is voting for a rate rise. He had done so in June and August this year, voting for an increase of 25 basis points. "Beyond my limits of tolerance" the term used. A reference to the policy trade off between above target inflation and the output gap. Inflation is above target. The output gap is evaporating as the economy reaches full employment. The time is right, to raise rates now to preempt the need for higher rate rises in the months and years to come. It is a familiar refrain, shared on the MPC by Ian McCafferty. The problem is to explain the ephemeral. How do we measure the output gap and capacity? Central bankers pine for the period when the Taylor rule was dominant. A simple monetary policy reaction function, tracking base rates in relation to inflation and the output gap. The output gap simply measured as GDP actual, in relation to the long term trend rate of growth. The model was blown away in the great recession. The perceived output gap was blown off scale by the large and significant slow down in the economy. To follow the Taylor rule implicitly, negative real rates would have had to be determined at scale to allow the model to run. Dangerous and impractical, the option emerged, to acclaim the substitution effect of QE. The spurious proposition that £1 billion of QE money spent would equate to a one basis point blip in base rates was proffered by Adam Posen and others. £425 billion of gilts bought somehow would offset the restrictions of the real rate floor to balance policy. It was nonsense of course. So here we are trapped on Planet ZIRP. Rates on the floor, mispricing capital. The magnetic compass spinning without end, as bankers search for the elusive measure of the output gap and measures of capacity. I have always been fascinated by the concept of capacity restrictions in £2 trillion economy. Running a business, we understood all to well the concept of capacity with a two shift system. Limits to capital could be swayed by overtime working, week-end working or in severe cases the introduction of a three shift system. When the balance of supply and demand was under threat, fixed capital was flexed until additional investment could be made. Fixed capital is not so "fixed" after all. In the wider economy, economists struggle to define and determine the concept and measurement of capacity. Why bother? The labour market offered the best option. The meandering NAIRU and the flawed Phillips Curve betray the aspirations of accuracy. Remember when 7% unemployment rate would be the trigger for forward guidance and the first rate rise? In the UK and the USA we struggle to understand why a "u" rate of 4.5% and below is failing to deliver a rise in earnings and the support of real earnings. Michael Saunders, the hawk in the park, (He was speaking at the Park Plaza Hotel in Cardiff) had difficulty in explaining the concept of capacity as a policy counterpoint to the idea of inflation above target. It is difficult. The Taylor rule is dead. The quest for a measure of capacity is difficult to define and measure. It is time to consign "capacity", the meandering NAIRU, the failing Phillips curve to the dustbin of economic thought, along with the J curve and the devaluation solution. Maybe it is time to accept that life on Planet ZIRP is the issue. One day we will realise, low rates are the problem. ZIRP is the missing link in the Phillips curve trade off. The hawk in the Park is right! It is time to raise rates and escape from Planet ZIRP ... Too many notes ... The Prime Minister was in Japan this week. Theresa May confessed she had never done "Karaoke". Running through the fields of wheat, is all we can pin on the Lady of Number Ten for the moment. David Davis was left in charge of negotiations with the EU! Liam Fox tried to help out, accusing Barnier of Blackmail over the demands for money to start the ball rolling on trade. "Bills must be paid, before talks about trade" the mantra, the trade trio fail to grasp the basics of the deal. Davis appears remarkably relaxed about the whole process. "Too many notes" Emperor Leopold II would declaim Mozart's Marriage of Figaro. "You have shown us something quite new today but is simply has too many notes". No such criticism could be leveled at the Secretary of State for Exiting the EU. Barnier appears to be quite confused about the "Ask" as part of the process. David Davis has shown "nothing new" and has no notes on the table to share. What exactly is the UK proposition? Plans for his "new form of trade" were dashed this week. Proposals for an "innovative" and "unprecedented" approach to border controls removing the need for customs checks between the UK and the UK were abandoned. The plan had been met by bafflement and scepticism from business either side of the Channel. It simply cannot work. Neither can the UK approach to Europe. Access to the single market, inside the customs union free to negotiate trade deals with the rest of the world fails to satisfy the basic "rules of origin" required for free trade function. Davis may argue the EU deal is essential to the world economy, globalization and trade. Michel Barnier is not convinced. The world looks on in bewilderment about the lack of progress ... Don't Miss the Economics Conference on the 13th October. Our theme is the Economics of Greater Manchester. We will be talking about the Inclusive Growth Challenge, Balancing the Books and the Sectors Driving Growth in the City Region! Another Great Conference in the pro-manchester series . We have a great line up of speakers to be announced this week. Book Now Don't Miss Out … That's all for this week. A bit geeky perhaps, sorry about that! Have a great week-end ... John Thanks for your feedback on the Saturday Economist Net Promoter Scores survey. Here's what you are saying about the weekly update! Thanks. |

The Saturday EconomistAuthorJohn Ashcroft publishes the Saturday Economist. Join the mailing list for updates on the UK and World Economy. Archives

July 2024

Categories

All

|

| The Saturday Economist |

RSS Feed

RSS Feed

The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The presentation should not be construed as the giving of investment advice.

|

The Saturday Economist, weekly updates on the UK economy.

Sign Up Now! Stay Up To Date! | Privacy Policy | Terms and Conditions | |