“Capitalists will sell us the rope by which they will hang” said Stalin. No need for communists to undertake the task, businesses are in danger of commercial suicide if gloom persists about the impact of the referendum result. “Waiting for Godot” or capitalising on the hanging tree with a stronger belt the options in Beckett’s drama. So too, the options loom for UK business. In the UK, survey data continues to cast a gloom over the economy. Little reason why this should be the case. Post referendum nothing has really happened yet. Nor is it likely to for the next five years. Stalin said, “It is not the people who cast the vote who determine the election, it is the people who count the votes that really matter”. Better still and not too late for the referendum, the counters also get to interpret the result. So why so gloomy? UK GDP growth of 2.2% in the second quarter of the year … Growth in the UK increased by 2.2% in the second quarter up from 1.8% in the first quarter of the year. A strong performance in services was boosted by 5% growth in the leisure sector and 2.7% growth in business services. Construction output fell by 1.2%. Weakness of government spending is largely to blame, offsetting the strength in private sector housing and commercial real estate. A surprise leap in manufacturing output produced growth of 1.4% in the quarter. We as yet cannot determine if this is just a blip, or a return to trend growth. Our forecast manufacturing growth of just 0.1% this year would increase to 1.1% if this were the case, with little or no material impact on overall GDP. We have reduced our forecast for GDP growth for the current year to 1.9% slowing to 1.3% in 2017. The forecast could be upgraded if the Autumn review were to release new funds for infrastructure and housing. Bank of England Set to Act … According to Sam Coates writing in The Times today, the Bank of England is set to forecast zero growth next year from 2% previously. Speculation persists a further round of QE or even a rate cut is possible in August, as the Old Lady Frets about the referendum result. Let’s hope not. The damage to savers and the banking sector is already intense. There is little in the handbooks to suggest a further cut would have any positive impact on activity or sentiment. Survey data continues to cast a gloom over the economy. Little reason why this should be the case. Post referendum nothing has really happened yet. Nor is it likely to for the next five years. Article 50 will not be triggered until 2017. No trade talks will take place until the exit timetable and framework has been agreed. It would appear that every board room has a Brexit bin at present. Profit warning … dump it in the Brexit bin. Need to restrutcure … dump it in the Brexit bin. Job losses … dump it in the Brexit bin. Problems with sterling weakness? Then businesses should have been hedging synthetically or naturally. In any case, there is no reason to assume Sterling weakness is a structural adjustment without fundamentals to sustain the move. Technically oversold, a bounce back is possible if the Bank of England holds rates and begins to hint at an increase. Inflation is set to rise in the final quarter of the year as oil prices increase by over 30% in sterling terms. In the first quarter of 2017, prices will rise by over 60% assuming oil and sterling hold at closing prices as of this week. No time to cut rates. The implications could be devastating! I would be forced to admit that Danny Blanchflower was right all along! So what happened in the USA … US GDP increased by just 1.2% in the second quarter of the year. This was below estimates and the 1.6% growth recorded in the first quarter. Strong growth in consumer spending was offset by the weakness in investment particularly in the oil sector. Expectations of a Fed rate rise in September have receded slightly. A strong jobs market, rising house prices and healthy household spending may yet force a rate rise in early Autumn. So what happened to markets ? Sterling rallied against the Dollar to $1.323 from $1.309 but moved down against the Euro at €1.185 from €1.194. The Euro moved up against the Dollar to 1.116 from 1.096. Oil Price Brent Crude closed at $42.36 from $45.27. The average price in July last year was $56.56. In August it was $46.52. Markets, were down - The Dow closed up at 18,441 from 18,583. The FTSE closed at 6,724 from 6,730. Gilts - yields moved down. UK Ten year gilt yields closed at 0.69 from 0.82. US Treasury yields moved to 1.48 from 1.58. Gold closed at $1,350 from $1,320. John That's all for this week ... don't miss our what the papers review every morning @jkaonline. Don't miss our Masters of Strategy Series on Digital Disruption and the New Yahoo Case Study out now! If you enjoy the Saturday Economist, you will love our research on strategy. Join the mailing list here! Don't miss out! Finally Don't miss the Economics Conference in October, our theme is Manchester China ! Book Now! The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of advice relating to finance or investment..

0 Comments

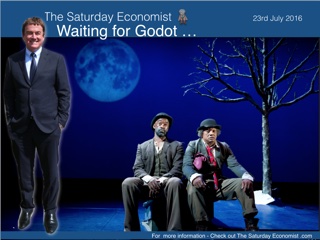

An early start to the week on Monday, BBC Breakfast at 6:50am talking down the excitement from the EY ITEM club latest forecast. The far too gloomy outlook for the economy has growth plummeting next year and employment on the rise. Why so gloomy? At the end the week we take a hard look at the PMI Markit Flash forecast for the UK economy. “Britain’s economy shrinking at fastest rate since 2009”, the headline in the Guardian today. “Flash survey points to post Brexit recession” the headline in the Times. The PMI Markit “Flash” survey has an index plummeting below the magic 50 level, a clear signal of setback, or is it? According to Chris Williamson, Chief Economist at Markit, the downturn whether as a result of order cancellations, a lack of new orders, or the postponement or halting of projects was attributed in one way or another to Brexit. Interesting isn’t it. Nothing has actually happened yet re Brexit. Nor is it likely to for the next five years. OK there has been a vote and a surprise result. But we are not leaving the EU just yet nor are we “leaving Europe”. Article 50 will be triggered early in 2017, then will follow a tortuous series of trade negotiations which may be completed by 2022 at the earliest. The PMI Flash survey has no pedigree and is a one off survey, taken at the moment between the referendum result and the government interregnum. Later data will include the first moves by the May administration which may have improved business sentiment significantly. The latest data on retail sales, jobs and borrowing may also improve the reaction from business. Time also to factor in the possible relaxation of fiscal and spending policy as announced by the new May-Hammond axis. Waiting for Godot … The forecast models assume uncertainty will impact on investment, recruitment, housing and household spending. Waiting for something but what? Economic “Agents” are expected to behave like Vladimir and Estragon in Samuel Beckett’s allegory. Waiting in a dark place by a dead tree, for the elusive Godot, to appear always tomorrow with something better to offer. By the end of the play, even the tree returns to life, but for the luckless pair, inactivity and inertia remain the norm. Trapped in a prolonged moment of eternal despair. Business cannot wait for Godot. Consumers remain impatient to spend the leisure pound on Pokemon Go and other pleasures. Business opportunities must be taken as presented. No chance to wait for five years. The good deals will continue at best prices. The bad deals will flounder along with the overpriced. The Bank of England “Agents’ summary of business conditions” July suggests it is very much business as usual in the wider community. Uncertainty has risen but the majority of firms did not expect a near-term impact on investment or hiring plans. There was no clear evidence of a slow down in activity. Monetary and Fiscal reaction … The Governor of the Bank of England has made it clear the Bank will act to ease monetary conditions if necessary to support growth. Martin Weale and Kristin Forbes have argued against a rate cut this week. The likelihood of an August move to cut rates appears as unlikely as it is undesirable. Action should be taken to support Sterling from current over sold levels, not weaken the currency as we drift into the NIRP crevasse. The Chancellor has hinted there may be fiscal or spending moves to compensate for any reduction in domestic demand. More spending on infrastructure and housing the obvious move to compensate for investment and household spending weakness. The Audit Office issued a warning this week on over commitment to Heathrow, Hinckley, Trident, HS2 and the Northern Powerhouse! The borrowing figures released this week, offered a modest reduction of £1.6 billion over the first three months of the year. Treasury will struggle to near the ambitious target reduction headlined by the OBR for the year ahead despite the rise in employment and retail spending. Retail sales June … Retail sales data for June did not suggest any spending weakness. Retail sales volumes increased by over 4% in the month. The problems for the “High Street” exacerbated as values increased by just 1.5%. Online sales increased by 14.1%, accounting for 14.2% of all retail sales activity. The squeeze on bricks over clicks continues. Job Figures … The unemployment rate fell to 4.9% in May. The number of vacancies matched the number of people looking for work according to the claimant count in June. The number of people unemployed was 1.65 million down by 200,000 in the year. The number of people in work increased by almost 600,000 over the twelve months. Inflation … Inflation CPI basis increased to 0.5% in June from 0.3% prior month. A rise in airfares and motor fuels pushed the overall index higher. Service sector inflation increased to 2.8%. Goods inflation fell by -1.6%. The trend is turning for inflation. Clear signs of reversal are evident in producer prices both input and output. The weakness of Sterling, if sustained will exacerbate the swing. If oil prices hold at current levels, Brent Crude £ basis will increase by 25% in the final quarter of the year and by 50% in the first quarter of 2017. No time for the MPC to make the rate cut! The Fed look set to hike rates in September. That's all for this week ... don't miss our what the papers review every morning @jkaonline. Don't miss our Masters of Strategy Series on Digital Disruption and the New Yahoo Case Study out now! If you enjoy the Saturday Economist, you will love our research on strategy. Join the mailing list here! Don't miss out! Finally Don't miss the Economics Conference in October, our theme is Manchester China ! Book Now! Interested in Strategy? Join our Masters of Strategy on Digital Disruption... Don't miss our regular updates on Corporate Strategy in the Masters of Strategy Series. © 2016 John Ashcroft and Company, Economics, Strategy and Social Media, experience worth sharing. ______________________________________________________________________________________________________________ The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of advice relating to finance or investment.. ______________________________________________________________________________________________________________ For details of our Privacy Policy and our Terms and Conditions check out our main web site. John Ashcroft and Company.com _______________________________________________________________________________________________________________ Copyright © 2016 The Saturday Economist, All rights reserved.    So much for a two horse race. Theresa May romped home without challenge ...

The new Prime Minister moved into Number Ten on Wednesday. Heads rolled - Gove, Letwin and Osborne left government. Heads turned - Phillip Hammond became Chancellor of the Exchequer. Eyes rolled - Boris Johnson became Foreign Secretary. Ruthless with a sense of humour, the May Day tumbrils rolled along Downing Street. The Brexit boys have been moved to the front line. Boris Johnson will baffle the heads of Europe, David Davis is to assume responsibility for Brexit negotiations and Liam Fox will head up the department of international trade. No skulking in dark shadows, daggers drawn ... the Eurosceptics have taken the Queen's shilling. When the whistle blows on Article 50, the generals will step out of the trenches. The bombardment has already begun. It could all be over by Christmas. David Davis believes negotiation is "explaining to the other side the things you really would like to have". Access to free market, without paying the subs and finding jobs for the peoples of Eastern Europe. All over by Christmas? The lights are going out all over Europe. No one is taking his call. Liam Fox my have to boost the immigration figures. We have no trade negotiators to meet the enormous job of negotiating deals around the world. A few may return from Brussels but one thousand are needed. We may have to recruit from overseas, with a points system of course. Can you negotiate? Can you make a point". You are in! Welcome to the UK! Phillip Hammond in at Number Eleven ... Phillip Hammond has taken over as Chancellor of the Exchequer. No easy transition but no knee jerk "statement" in response to the rôle either. The chief financial minister will take time and counsel in the preparation of his first Autumn statement. Lots of advice there will be. Consumer confidence has been hit. Business spending plans are under review. House prices and commercial real estate prices have been marked down. Private car sales fell in June as overall sales slowed. Construction slows ... The construction figures for May released this week were disappointing. Overall output was down by 2% year on year. The good news - private sector housing was up by over 4%, commercial real estate was up by over 3%. Declines in public sector housing down 20% and infrastructure spending down 10% pushed overall output lower. So what is to be done ... With the financial fetters off, as spending targets are reviewed, the Chancellor could have some easy wins in the Autumn statement. A boost to housing and infrastructure, confirmation of spending on runways, rail and transport routes. "Business as usual" should be the guideline. Nothing may change for five years or more as trench warfare returns to Europe in Team Brexit negotiations with the EU. Business hates uncertainty. Clarify where we can. The Prime Minister should make it clear, there will be no enforced repatriation of EU citizens currently living and working in the UK. Let us make it clear, students from around the world are welcome and will continue to be so. It really is time to take education out of the immigration stats. Cuts to corporation tax, a boost to investment allowances, rethink the apprenticeship levy, it was just a payroll tax after all. Keep out of the board room and the bed room. Don't worry about executive pay, 50% goes to Treasury anyway. Oh yes and abolish that iniquitous bedroom tax. So much social misery for so little return. The Bank of England holds rates … This week the Governor of the Bank of England maintained his reputation as the unreliable boyfriend. Teasing markets with the hint of a rate cut, nothing changed on Thursday. The MPC voted 8-1 to maintain the base rate at 0.5% and to hold QE stocks at £375 billion. A hint of action to come in August? "Most members of the committee, expect monetary policy to be loosened next month". various easing points and combinations thereof were discussed. A rate cut, more QE, a boost to the funding for lending scheme? Perhaps, we shall have to wait and see. Taking a sledgehammer ... Andy Haldane, Chief Economist at the Bank of England has said "I would rather run the risk of taking a sledgehammer to crack a nut than taking a miniature rock hammer to tunnel my way out of prison". So much for attitudes to a working life in the Bank of England. The call is for a material easing of monetary policy in August. There should be no rush to action. No perceived panic measures. Business as usual with clear support as the lender of last resort, in the event of a liquidity challenge in property and finance. I can think of of one young nut in Threadneedle Street, to be cracked with a sledgehammer Inflation set to rise ... Inflation is set to rise ... if sterling and oil prices stay at current levels, the cost of oil will increase by 15% in next month and by almost 40% by the end of the year. No time to ease monetary policy. Business as usual the mantra. Time to support the return of Sterling to normality from current oversold levels. So what happened to Markets? Sterling rallied against the Dollar to $1.316 from $1.296 and also against the Euro at €1.189 from €1.171. The Euro held against the Dollar to 1.106 from 1.105. Oil Price Brent Crude closed at $47.58 from $46.82. The average price in July last year was $56.56. In August it was $46.52. Markets, were up - The Dow closed up at 18,479 from 18,120. The FTSE closed at 6,669 from 6,590. Gilts - yields moved up. UK Ten year gilt yields closed at 0.84 from 0.73. US Treasury yields moved to 1.59 from 1.37. Gold closed at $1,327 from $1,352. John That's all for this week ... don't miss our what the papers review every morning @jkaonline. Don't miss our Masters of Strategy Series on Digital Disruption and the New Yahoo Case Study out now! If you enjoy the Saturday Economist, you will love our research on strategy. Join the mailing list here! Don't miss out! The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of advice relating to finance or investment …  It’s a two horse race to be the next Prime Minister of Britain. Gove is a goner. Osborne gone missing. Theresa May versus Andrea Leadsom the run off. We can but hope the race will be over soon and we can get on with doing - whatever it is we are going to do … It is too early to understand the impact of Brexit on the UK economy. It could take five years yet. Some believe we may never get to know. The hope, a deal may be struck before the end is nigh. A sort of three for four deal. Freedoms on trade, services and capital with restrictions on immigration. All this without a contribution to EU coffers. An end to the Nanny State. An end to euro regulation and bureaucracy. Well good luck with that. We are handing in our Article 50 notice before the end of the year. Team EU are forewarned and are already taking evasive action. The referendum is impacting on the UK economy … The referendum decision is impacting on the UK economy, in ways in which were expected. Sterling has fallen against the Dollar and the Euro. Markets have reacted to the downside with the broader FTSE 250 in decline. Consumer confidence has taken a hit. Car sales are lower in June. High Street sales will slow further. Retailers are complaining about the impact of sterling’s fall and higher prices in store. Economics models suggest a 10% fall in sterling will lead to a 2% - 3% rise in consumer prices over the next few years. The models are dated, unlike the real time line action. Inflation will begin to rise pretty quickly. There is little scope for margin absorption in the manufacturing, wholesale or retail channels. The impact of sterling’s decline will impact before the end of the year, compounded by a rise in dollar denominated oil and commodity prices. Property funds have been hit … Property prices in the South East have been hit. Commercial real estate confidence has been damaged by the “gating of funds”. Major funds including Aviva, M&G, Standard Life, Henderson have stemmed the flow of withdrawals by shutting doors and marking down prices. Bold moves isolate the threat to the financial system. Time for investors to reflect on fundamentals. Confidence will return and prices will recover. Investment plans are subject to revision. Sectors at risk are banking and financial services in London; Motor manufacturing across the UK and in the North East particularly; JP Morgan threaten to leave London. Paris and Frankfurt will compete to entice relocation for London’s big players. We expect a negative impact on aerospace, chemicals and big Pharma but not for some years yet. Ironic this week Tata steel announced a possible deal with ThyssenKrupp. The steel industry dependent on imports of ingots and coke to feed the furnaces will not benefit from the vagaries of currency. So what of trade … and the other two horse race … This week the ONS released trade figures for the UK economy. The deficit trade in goods increased in May. For the year as whole we expect the trade gap to increase to £130 billion this year. There will be no trade amelioration as a result of sterling’s decline. [As we have explained at some length and for many years.] The current account deficit according to the ONS was 7.2% in the final quarter of 2015 and 6.9% in the first quarter 2016. The Bank of England has warned that the UK’s large current account deficit poses a threat to financial stability. The UK is financing this deficit by an inflow of foreign investment - if investors lose their appetite for UK assets they will demand higher risk premia, pushing up the financing costs for the deficit. No real evidence of a gilt strike so far. Ten year yields have fallen below 1%. The governor is threatening to cut base rates still further. The move would undermine, not support sterling and do nothing to encourage positive capital flow. Current account deficits of such dimension, have never been experienced before in our post war history and never on Planet ZIRP with base rates at 0.5%. Over in the US, payroll numbers increased by 287,000 in June. The Fed indecision about the rate rise may be eased by the news. The Fed is likely to move in August placing greater pressure on Sterling. The next move for the Bank of England should be to push rates higher. So what happened to Markets? Sterling fell against the Dollar to $1.296 from $1.326 and down against the Euro at €1.171 from €1.191. The Euro fell against the Dollar to 1.105 from 1.113. Oil Price Brent Crude closed at $46.82 from $50.15. The average price in July last year was $56.56. Markets, were up - The Dow closed up at 18,120 from 17,954. The FTSE closed at 6,590 from 6,577. Gilts - yields moved down. UK Ten year gilt yields closed at 0.73 from 0.86. US Treasury yields moved to 1.37 from 1.45. Gold closed at $1,352 from $1,335. John That's all for this week ... don't miss our what the papers review every morning @jkaonline. Don't miss our Masters of Strategy Series on Digital Disruption and the New Yahoo Case Study out now! If you enjoy the Saturday Economist, you will love our research on strategy. Join the mailing list here! Don't miss out! Interested in Strategy? Join our Masters of Strategy on Digital Disruption... Don't miss our regular updates on Corporate Strategy in the Masters of Strategy Series. © 2016 John Ashcroft and Company, Economics, Strategy and Social Media, experience worth sharing. ______________________________________________________________________________________________________________ The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of advice relating to finance or investment..   When elephants fight, the grass roots suffer. It is as true in Africa, as it is for political parties in the U.K. Disputes must be over quickly. Leader selection is an unseemly process. Much is to be done, to deal with life post Brexit. Jeremy Corbyn is confined to some ivory tower in Westminster. Rapunzel without the hair, rescue awaited from grass root activists. Elected labour MPs have mounted a silent coup. The tree has fallen in the forest. No one appears to have heard. No one appears to know what to do next in the red tent ... In the blue camp, Boris Johnson will not be Prime Minister. Gove has delivered the stilleto's kiss. Not fit for purpose, the damning claim. Michael Gove makes out his case - "I never thought I’d ever be in this position. I did not want it". Sounding more like Evita Peron, "I had to let it happen, I had to change", Gove confessed "Whatever charisma is, I don't have it." Not to worry, there is a man with guile and cunning in spades, to offset any charm deficit. Theresa May is the bookies favourite. Taking the stance of a headmistress at the start of a new term. "No more fighting in the playground. We are leaving the EU." Anthea Leadsom is making an early run. "The next leader of the party must be a "Brexiteer". Ouch. Gove is a goner. Conservatives love assassination, they just don't like the blood it makes. Nor do they love the bloodied hand that bears the knife. Even though it was plunged into Boris Johnson. So what happens next ... Markets bounced. The FTSE closed up 400 points near 6,600. Sterling fell against the dollar and the Euro. Gilt yields slumped below 1%. How the gods of Planet ZIRP scoff mere mortals as we continue to misprice capital. The Governor of the Bank of England made a "no need to panic" speech. Now we know how policy is formulated. Above the central arch, there is a weather vane. Originally installed in 1805, it has played a central part in monetary policy. When the wind blew from the East, ships would travel up the Thames. Merchants would need finance to purchase the cargo. When it blew from the West, credit would need to be withdrawn, the boats were not coming in! Forward guidance and a demand for money function determined by which way the wind is blowing. The Governor is convinced the wind is blowing in the wrong direction. Economic conditions have deteriorated. Some monetary easing will be required over the Summer. More QE and a rate cut! Surely not. Inflation is set to accelerate into the second half of the year. Oil and commodity prices are rising. Sterling weakness will exacerbate domestic inflation. Lest we forget the yawning current account deficit. 7% of GDP in the first quarter of the year. Time to stay the hand of monetary policy .... There will be time soon enough to act.. And what of fiscal policy ... Give us the money or the cow gets it! The Chancellor has accepted, enough of fixing the roof. Time to accept the inevitable. We no longer plan to achieve a budget surplus by the end of parliament. Enough of fixing the roof whilst the sun is shining. Time to bring in the roofers before the storm begins. Theresa May has made the call. An end to austerity. So what really happens now? Well not much. The new Prime Minister will be installed in September. A working party will determine the "new deal" to negotiate with the EU. Article 50 may be triggered before the end of the year. Or may be not. It will then take up to two years to determine the exit process and much longer to determine the new trade deal. It could be five years before the changes begin to hit the UK in a big way. Lots of time to condition the electorate to a deal which will offer free trade at the price of a weekly subscription and free movement of labour. What can be done ...? Cut immigration? Re classify students and those in pursuit of further education. Slash the numbers with one strike of the pen. Guarantees must be offered to farming, universities, big pharma and the regions. No money to be lost over the next five years and beyond as a result of any loss of EU deal. Status Quo Ante Referendum the guideline. Greater commitment to schools, education and the health service to follow. The people have spoken ... and they have had enough for now. So what happened to Markets ...? Sterling fell against the Dollar to $1.326 from $1.375 and down against the Euro at €1.191 from €1.230. The Euro fell against the Dollar to 1.113 from 1.117. Oil Price Brent Crude closed at $50.15 from $48.70. The average price in July last year was $56.56. Markets, were up - The Dow closed up at 17,954 from 17,503. The FTSE closed at 6,577 from 6,138. Gilts - yields moved down. UK Ten year gilt yields closed at 0.86 from 1.09. US Treasury yields moved to 1.45 from 1.57. Gold closed at $1,335 from $1,316. John That's all for this week ... don't miss our what the papers review every morning @jkaonline. Don't miss our Masters of Strategy Series on Digital Disruption and the New Yahoo Case Study out now! Interested in Strategy? Join our Masters of Strategy on Digital Disruption... Don't miss our regular updates on Corporate Strategy in the Masters of Strategy Series. © 2016 John Ashcroft and Company, Economics, Strategy and Social Media, experience worth sharing. ______________________________________________________________________________________________________________ The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of advice relating to finance or investment..  |

The Saturday EconomistAuthorJohn Ashcroft publishes the Saturday Economist. Join the mailing list for updates on the UK and World Economy. Archives

July 2024

Categories

All

|

| The Saturday Economist |

RSS Feed

RSS Feed

The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The presentation should not be construed as the giving of investment advice.

|

The Saturday Economist, weekly updates on the UK economy.

Sign Up Now! Stay Up To Date! | Privacy Policy | Terms and Conditions | |