According to the Times this week, when Rishi Sunak returned from his holiday he had a list of priorities for the second phase of his premiership. Such was the desire for secrecy that each of them was given a code name.

The code name theme for the policy group was trees. Net zero was cedar, education was elm, HS2 was redwood and health was hawthorn. “It’s been quite surreal,” a Downing Street official said. “People keep saying things like: ‘I’ve just got to go into a meeting on elm.” "Off to a session on Dead Wood". "Health is a thorny subject". That sort of thing. The first of those plans began to emerge this week as Sunak unveiled the result of Project Cedar, a significant watering down of green policies on the route to net zero. The ban on the sale of petrol and diesel cars has been put back to 2035. There will be no ban on buying new boilers. Households will not be required to sort the rubbish into seven bins. There will be no new taxes for eating meat, no travel tax for frequent flyers, no compulsory car sharing. As Sunk explained in his speech ... "The proposal for government to interfere in how many passengers you can have in your car. I’ve scrapped it. The proposal that we should force you to have seven different bins in your home. I’ve scrapped it. The proposal to make you change your diet by taxing meat. I’ve scrapped it. The plan to create new taxes to discourage flying or going on holiday. I’ve scrapped that too. The good news, there will be bigger grants for new boiler installations and assistance with home installation. I know people in our country are frustrated with our politics. I know they feel that much gets promised, but not enough is delivered. It's a bit like HS2 ... Rishi Sunak set to scrap the second leg of HS2 to Manchester ... Apparently [I] am considering scrapping the second leg of HS2, which would have linked Manchester to Birmingham and London. Concerns are rising that costs of the project are “out of control”. My Ministers have also discussed terminating trains at Old Oak Common in west London about six miles short of Euston. Passengers will be able to use bus or tube to complete the journey. A new terminal "Uber on the Common"" is under consideration. This will save money and be very handy for Tory voters in the South East. The Prime Minister has been told by Boris Johnson and David Cameron to drop plans to scale back HS2. Johnson has warned amid warnings that a “mutilated” line would be “insanity”. George Osborne has also made clear his opposition to abandoning the northern leg. He has spotted that scaling back the project would be a “big blow” to the leveling-up agenda. There are also divisions within the government over the plans for the second leg, which have been code named "The Dead Wood Stage". Michael Gove, the leveling-up secretary, is said to be pushing for the line to be built in full. "It would be “very stupid” to scrap the northern leg entirely. Education Education is also under review. The Times disclosed this week that Sunak was planning a radical reform of A-levels with a new style of British baccalaureate. The Prime Minister could announce plans to scrap A-levels entirely. English and Maths would become compulsory until the age of 18. This, it is said, would assist in the future with cost calculations and forecasts for large scale infrastructure projects, if more people could add up. The cheaper option would be to avoid another radical change in education just for change sake. Keep the A levels in place, just allow students to use excel and AI as part of the curriculum. But then some policy planners just can't see the wood for the trees ...

0 Comments

Welcome to the Nèijuǎn 内卷 World Economy ... "An economy twisting inward without real progress ...

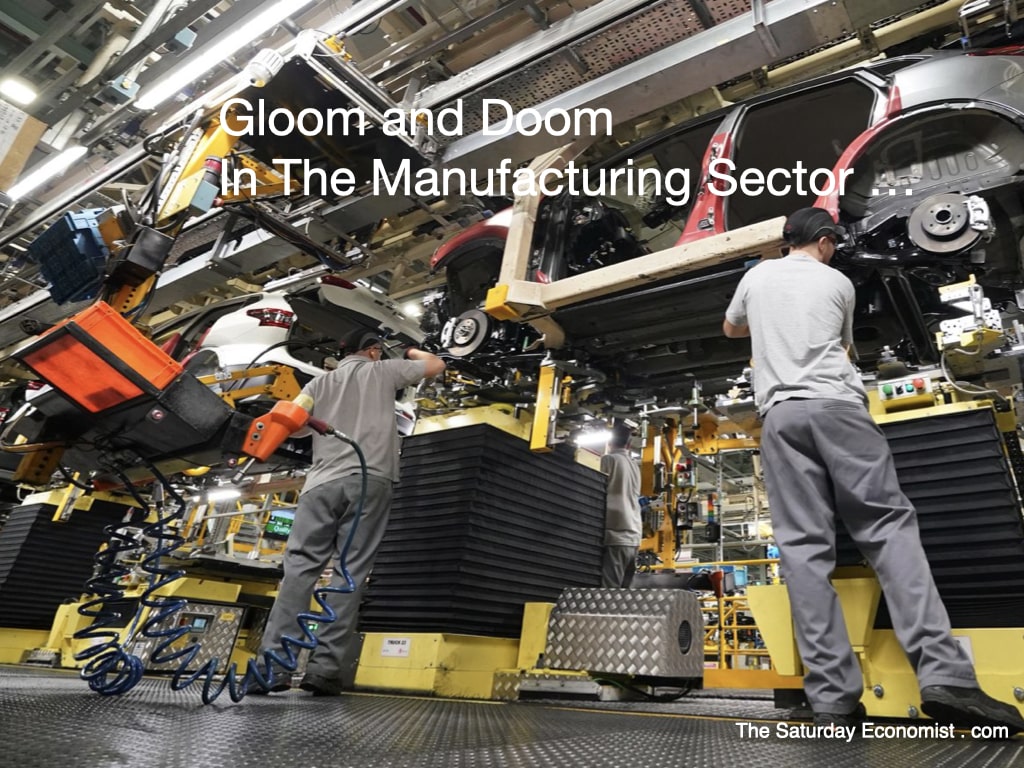

Neijuan has featured in analyses of life in China in the recent years, due to the uneven distribution of social, economic, and educational resources and ongoing economic malaise in terms of higher education, labor markets and youth unemployment. Neijuan reflects a life of being overworked, stressed, anxious and feeling trapped. A lifestyle where many face the negative effects of living a very competitive life for for apparently little gain. “A prevalent sense of being stuck in an ever so draining rat race where everyone loses.” Nèijuǎn 内卷 is made of two characters which mean “inside” and “rolling”. Ian Johnson, senior fellow at the council on foreign relations translates this as "life twisting inward without real progress". A world economy, twisting inward without real progress .... At the moment, it feels like the world economy is moving toward "Nèijuǎn 内卷 ... a world economy, twisting inward without real progress. World trade growth is slowing. World growth is stagnating. A world which includes the UK post Brexit, European stagnation in the face of energy cost acceleration, China and the U.S. decoupling and a setback for globalization as a cold war mentality returns with an East West axis. "Guns or Butter" takes in a new meaning as Moscow barters maize for munitions with Pyongyang. China develops BRICS Plus, a new trading block no longer to be Dollar dependent. This week news of the China ban on iPhone use for government workers in a Tik for Tok reaction to U.S. and European restrictions on Huawei, sent tech stocks tumbling. Huawei launched a new smartphone which appears to have bypassed or surpassed chip restrictions by the Biden administration. CNN reports, the United States government is seeking more information about the Huawei Mate 60 Pro, a Chinese smartphone powered by an advanced chip which China cannot have produced! The new flagship phone, includes a 5G Kirin 9000s processor developed specifically for Chinese manufacturer Huawei. Industry experts could not understand how the company would have the technology to make such a chip following sweeping efforts by the United States to restrict China’s access to foreign chip technology. SMIC makes waves of progress and Huawei demonstrates the futility of sanctions. Lessons to be learned from the 12th century when Canute demonstrated his inability to control the progress of tides. The futility of Sanctions ... The futility of trade sanctions is adequately demonstrated by the experience of the Trump administration. Trump’s tariffs have cost Americans tens of billions of dollars. Despite claims that China will pay, border taxes were passed on to consumers by import agents. Following the imposition of tariffs on Chinese imports. The goods trade deficit with China did dip when Trump launched his tariff campaign in 2018. At the same time, however, the deficits with Mexico and the rest of the world went up. Since 2017, when Mr. Trump entered the Oval Office, goods imports to the U.S. in nominal dollars have increased 174% from Vietnam, 116% from Taiwan, 96% from Bangladesh, 89% from Thailand, 76% from India, and 62% from South Korea. China Exports are falling this year ... There are some suspicions China product is being redirected from Vietnam and Mexico to bypass restrictions. China’s exports fell by 8.8 per cent in August compared with a year earlier, while imports fell by 7.3 per cent last month. Exports to most of China’s major trading partners continued to shrink in August, though the declines narrowed from July. Export values continued to contract but export volumes continued to hold up well and are still above their pre pandemic trend. Trade Surplus Remains ... China’s total trade surplus in August stood at US$68.4 billion, down from US$80.6 billion in July. The surplus narrowed as imports accelerated more than exports. China’s customs authorities highlighted an expanding trade surplus with the Asean bloc, while China’s trade surplus with the US and European Union declined. Analysts expect China’s exports to decline over the coming months before bottoming out toward the end of the year. Expect further consolidation with the ASEAN bloc and BRICS+. In Europe ... In the Euro area growth in the second quarter was up buy just 0.1%. There was zero growth in Germany and a 0.5% drop in Italy. France appeared to be the bright spot with 0.5% growth. In the UK, the latest signals from the PMI Markit surveys suggest a slowdown into the third quarter from growth of around 0.4% in the first half. We eagerly await the Chancellor's Autumn statement on the 22nd November. By then there should be good news on inflation and the direction of monetary policy. We don't expect much from the November statement. Little suggestion of growth plans for the UK economy to indicate we can escape from Nèijuǎn, an economy twisting inward without real progress ... References ... "China’s “Involuted” Generation" A new word has entered the popular lexicon to describe feelings of burnout, ennui, and despair. By Yi-Ling Liu The New Yorker May 14, 2021. 'Involution': The anxieties of our time summed up in one word Zhou Minxi CGTN December 4th 2020. The US government is investigating China’s breakthrough smartphone Samanthan Murphy CNN Business September 6th 2023. According to What's On Weibo, The popular use of the Chinese translation of ‘involution’, nèijuǎn 内卷, started to receive attention in Chinese media in 2020. It is meant to explain the social dynamics of China’s growing middle class. References include "Involution": The Anxieties of Our Time Summed Up in One Word” by Zhou Minxi (CGTN) and "China’s “Involuted” Generation" a new word to describe feelings of burnout, ennui, and despair and by Yi-Ling Liu*.  It was gloom and doom in manufacturing this week ...

According to the latest PMI data, Britain's manufacturing sector contracted in August at the steepest pace since Covid-19 lock down. The S&P Global / CIPS final purchasing managers's index (PMI) dropped from 45.3 points in July to 43.0 points last month, the worst reading since May 2020. It was the 13th month in a row the PMI has been below the 50 mark, indicating lack of growth in the sector. Manufacturers are reporting a weakening economic backdrop, as demand is hit by rising interest rates, the cost-of-living crisis, export losses and concerns about the market outlook. However, those firms with orders in hand enjoyed the fastest delivery times since January and the rate of inflationary pressures slowed to 2016 levels. Some price corrections eased the pain for manufacturers who registered a four month high in optimism about opportunities over the next 12 months. Better News from the Vehicle Sector ... It was better news from the vehicle sector. The latest update from Mike Hawes, Chief Executive of the Society of Motor Manufacturers and Traders was quite upbeat. UK car manufacturing notched up a sixth month of growth in July. Commercial Vehicles output knocked out a fourth month of growth. For CV production in particular, the year is turning into a real success story with soaring exports and a steady, stable domestic market driving volumes above pre-pandemic levels. Mike Hawes said "With the worst of recent supply chain difficulties behind us and plants ramping up production of electrified vehicles, the future is looking more optimistic." Vehicle manufacturing was up by 14% in the year to date. Output is expected to hit just under 900,000 vehicles in the year as a whole. A recovery perhaps, but still well down on the output peak of 1.7 million units in 2016. The era of Brexit overhang began. New registrations are expected to hit 1.9 million this year, generating a one million car import liability for the economy. EV's and hybrids will account for 55% of registrations creating a challenge for future growth as the SMMT explains ... Headwinds Ahead ... The changes to Rules of Origin thresholds are due in just four months time. "New Rules of Origin thresholds will pose a significant challenge to manufacturers on both sides of the Channel. The prospect of tariffs and, potentially, price increases on electric vehicles will inhibit sales, investment and production." The SMMT warns. Tougher rules, when applied, underline the critical need for the UK to increase its own battery and EV supply chain manufacturing capability. "Recent announcements are, of course, incredibly important and have helped rewrite the narrative around the UK sector. But we now need government to build on this momentum with a dedicated, cohesive strategy to attract further investment and a developed skills base in battery output and technology." said Mike Hawes. Meanwhile In China ... "Can anyone challenge China's EV Battery dominance", writes the FT last month. Technology breakthroughs and trade barriers will be need to take on CATL and BYD. It's going to be tough. CATL and Shenzhen based BYD have raced ahead of battery rivals in South Korea and Japan, leaving the US and Europe contemplating how to stoke an electric car industry without relying on China for the most important and costly piece of the puzzle. Louis Gave the CEO of Gavekal claims "China is now the biggest automobile exporter in the world, from nowhere five years ago. China now exports more cars than South Korea, Japan, or Germany." "BYD, is the biggest electric car company in the world in terms of production. BYD sells the BYD Seagull. It's a small hatchback, full electric, 220-mile radius, selling for 11,000 US dollars." "They just started selling them in Australia. They sold 10,000 in the first 24 hours, and then that was it. That's all they had. Like the first 10,000, gone, boom. So now they've got to send another 10,000 because, at that price point, you can put it on your credit card". UK Car production under threat ... Dominance in EV production, hegemony in battery supply. A monopoly in rare earth minerals. It is far too early to write off the Chinese economy. China is leading the world in new technology as we argued last week. Brexit overhang, the customs union circle, the rules of origin looming, the option to create a pan European solution for the UK no longer an option. The economies of scale required and the start up risks applying, a volt to British production would require, buyer forward commitments and a government underwrite to make the investment work. Car Production under threat, the SMMT warnings of headwinds to growth could be upgraded to a hurricane caution as the Brexit restrictions draw near ... |

The Saturday EconomistAuthorJohn Ashcroft publishes the Saturday Economist. Join the mailing list for updates on the UK and World Economy. Archives

July 2024

Categories

All

|

| The Saturday Economist |

RSS Feed

RSS Feed

The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The presentation should not be construed as the giving of investment advice.

|

The Saturday Economist, weekly updates on the UK economy.

Sign Up Now! Stay Up To Date! | Privacy Policy | Terms and Conditions | |