Ray Dalio founder of Bridgewater Associates was in Davos this week. Bridgewater manages about $160 billion of assets under management. He thinks investors should not miss out on the strength of the current market. "With too much money still on the sidelines, investors should dump cash for a diversified stock portfolio", with a little gold on the side.

"Cash is trash" Dalio said. "Get out of cash there is still a lot of money in cash". You have to balance with a certain amount of precious metals in the mix. Dalio has made the call before. In 2018, he warned that investors would feel pretty stupid if they remained on the sidelines during the market run up. Since then, the Dow and S&P have moved up over 20%, with Nasdaq showing a 40% gain. U.S. markets hit new highs this month, despite some profit taking during the week. The Dow is set to test the 30,000 level, the S&P and Nasdaq, looking a little over extended. "Say Goodbye to Old Highs" is the new mantra. The volume of activity suggests markets will push higher as the Senate denies the Democrats an impeachment victory next week. Google joined Apple, Amazon and Microsoft in the $ Trillion dollar club. Next step why not $2 trillion, the question asked. Strange when a PE of 30 is just chump change. Low interest rates are driving asset prices ever higher. U.S. ten year bond yields slipped 11 basis points this week to close at 1.71. US gilts closed down 6 points to 0.57 per cent. Life on Planet ZIRP is turning into a quarantine of international dimension. Jamie Dimon, Head of J.P. Morgan Chase warned this week, negative rates are the only thing worrying him in this otherwise "Goldilocks Place". "The only thing I have trepidations about are negative rates and QE. It's one of the great experiments of all time and we still don't know what the ultimate outcome is". "I would never buy a negative yielding bond" he added "In history, whenever we have seen anything like that, it didn't end well …" Risk of Great Depression … Kristalina Georgiva is the new boss of the IMF. Speaking at the Peterson Institute in Washington last week, Georgiva warned the latest IMF research compares the current economy to the "roaring twenties". We know that didn't end well. The Great Crash of '29 led to the Great Depression of the 1930s. The IMF thinks a similar trend is underway! "If I had to identify a theme at the start of the decade" she added "It would be greater uncertainty". Climate change and increasing trade protectionism would lead to greater social unrest and financial market instability. The IMF released their forecasts for growth in 2020 which were remarkably upbeat. World growth is expected to increase by 3.3% this year and by 3.4% in 2020. This compares with growth of just 2.9% last year. The U.K. is expected to grow by 2.4%, a higher rate than France and Germany, higher than the EU as a whole. In Davos, Trump declared the U.S. economy to be the strongest in the world. The IMF forecasts would beg to differ. Growth is expected to slow to just 2% this year and 1.7% next despite the tax cuts and spending plans. The President would like to blame the Federal reserve for raising rates too fast last year. "Without the rate hikes, the U.S. economy would be growing by 4%" Trump said.. Steve Mnuchin, Secretary of State at the Treasury, advised climate activist, Great Thornberg to "go to college and get an economics degree". Mnuchin graduated from Yale in 1985 with an economics degree, as if that helps when working with the Trump administration. With ballooning internal and external deficits, the U.S. is in danger of becoming a banana republic. The administration is preparing a second round of tax cuts to boost growth. Growth will be self funding and will mitigate the borrowing deficit, Mnuchin explained. The Fed is confused, confronted by fiscal irresponsibility AND financial repression, a heady cocktail for crisis, with the odd trade war on the side. Trump Tariffs Damaged U.S. growth ... So what went wrong? Gary Cohn former White House Chief Economic advisor explained on Sunday, how President Trump's tariffs hurt the U.S. economy and undermined the stimulative impact of the massive tax cuts passed in 2017. Trump's steel and aluminium tariffs "collided" with tax policy. The tariffs increased input costs reducing margins and profits, damaging investment plans and job expansion. Last week, the Federal Reserve confirmed the U.S. manufacturing sector was in recession. Output fell in 2019, despite the Trump claims to "Make American Manufacturing Great Again". Cohn, one of the "adults in the room" clashed with the President on the issue of tariffs and protectionism. The former Goldman Sachs President resigned in March 2018. Trump also faced push back from former State Diplomats over the conflict with China. "President Trump's lack of understanding of China, is to blame for the deteriorating relationship with Beijing" former diplomats explained. Doubts persist about the viability of the Phase One Trade deal with significant tariffs still in place. With "successful" trade deals concluded with Canada, Mexico, Japan and China, Trump will now turn his attention to Europe and the U.K. The dystopian disaster that is "Trump on Trade" will now inflict further damage on growth in the West. In the U.K. within days we shall be leaving the EU. The Prime Minister may claim we have crossed the line. Julius Caesar crossed the Rubicon but then became involved in a prolonged civil war. There is much to be done to understand policies on trade, immigration, investment, infrastructure and fiscal policy. Taking lessons from the Trump playbook on trade negotiations will not help ...

0 Comments

The Chancellor warned this week, there will be no alignment with EU regulations following the exit from the European Union. "There will be no alignment, we will not be a rule taker, we will not be in the single market, we will not be in the customs union".

It was all going so well. The election result, produced a Boris Bounce in confidence among business and the markets.There was even talk of a "Brino" deal, Brexit in name only, trade secured with our biggest trading bloc. During the referendum campaign it was Boris Johnson who asked the question about EU regulations. In a lorry park in the South East he asked, "Why should Brussels determine the dimensions of our lorries and containers?". It's a fair question but if they are to travel safely across Europe, it is best if UK drivers are able to pass over motorways and under bridges without a problem. Size is everything after all ... For regulation, read standardization. Manufacturers like common standards on products and components in many markets. Common standards guarantee quality, generate lower unit costs, economies of scale and improve productivity. The Chancellor claimed the Treasury would not lend support to manufacturers favoring EU rules. That just does not make sense. The Chancellor is out of step with industries including car manufacturing, chemicals, food and pharmaceuticals. Javid admitted, that some businesses may not benefit from Brexit. "The UK economy would ultimately continue to thrive in the long term. Once we have this agreement in place with our European friends, we will continue to be one of the most successful economies on earth". This week, the new boss of the IMF, Kristalina Georgieva, warned the global economy risks a return of a Great Depression comparable to the thirties. The benchmark for success may just be getting lower ... the Chancellor's trade stance will assist the process ... Retail sales disappoint ... One of the most successful economies in the world, had a disappointing end to the year. In the three months to the end of November, growth in the UK economy slowed to just 0.9% year on year. Manufacturing output fell by almost 2%. Growth of 2.2% in the first quarter, slowed to 1.2% over the following six months. The economy is slowing. Retail sales are falling. In December retail volume growth year on year was just 1%. The value of sales increased by 1.5%. Online sales increased by almost 6% accounting for 20% of all volume activity. Exclude food and the number rises to 30%. Almost one in three sales have now been lost from traditional retail to online trading. Boohoo is one of the great beneficiaries. Sales jumped 44% in the four months before Christmas. The share price has risen over 70% in the last year. The business now has a higher market cap than M&S. The online platform has rescued Karen Millen and Coast, now in the stable along with Boohoo, Nasty Girl and Pretty Little Thing. M&S slipped out of the FTSE 100 last year, Moody's is warning off a credit rating adjustment to "junk". No change in retail trends any time soon ... Price pressure is easing in the economy. Retail prices CPI basis slowed to 1.3% in December from 1.5% prior month. Low oil prices, a stronger currency and a slowing economy led to lower prices in food, clothing and services. Markets began to price in a rate cut at one stage last week. Michael Saunders, and MPC dove, suggested a rate cut may be necessary citing a slowing economy and subdued inflation. Let's hope not. What on earth could a 25 basis point cut achieve as we await the maiden budget from the "No Alignment Chancellor". Google Joins the Trillion Dollar Cap Club ... Google shares moved higher this week, joining the $Trillion dollar club along with Apple, Amazon and Microsoft. Together the four stocks account for almost 20% of the total market cap of the S&P 500. U.S. markets moved higher as Trump signed the "phase one" trade deal with China. The "currency manipulator" tag was removed from Beijing before the signing. China committed to buy $200 billion of goods from Uncle Sam across four main sectors including manufacturing, energy, agriculture and services. Plans for further tariff increases have been cancelled, some tariffs have been cut. 25% charges on some $250 billion of goods remain in place. Trump is now free to turn his attention to Europe. Whatever the merits of the trade war, it is clear U.S. manufacturing has not been the beneficiary. Latest data confirmed the manufacturing sector moved into recession last year. U.S. economic growth is slowing, the US deficit is set to hit $1 trillion dollars. The Treasury is issuing a twenty year bond, last seen in 1986, to assist with the huge funding process. China reported growth of 6.1% in the past year, with a further 6% growth in prospect this year. Growth in the US slowed to 2.3% in 2019 , with growth of just 1.8% expected in the current year. So much for "Make America Great Again." Next week sees the release of "A Very Stable Genius: Donald J Trump's Testing of America" "Taut and terrifying, it reads like a horror story" according to the New York Times. "It is as if the President, as patient zero, has bitten an aide and slowly bite by bite an entire nation lost its wits and compass." "You're a bunch of dopes and babies" Trump launched a stunning tirade against his generals during a Pentagon briefing, the book reveals. Impeachment looms. This week the President beefed up his legal team to include two of the biggest celebrity lawyers of the 1990s. Some express surprise, the President just doesn't handle the whole thing himself ...  Markets rallied, Oil and Gold surrendered early gains, the prospects of war in Iran eased significantly, then both sides appeared to de-escalate the crisis. Neither the U.S. nor Iran are marching as to war, for very good reason, as we explain below.

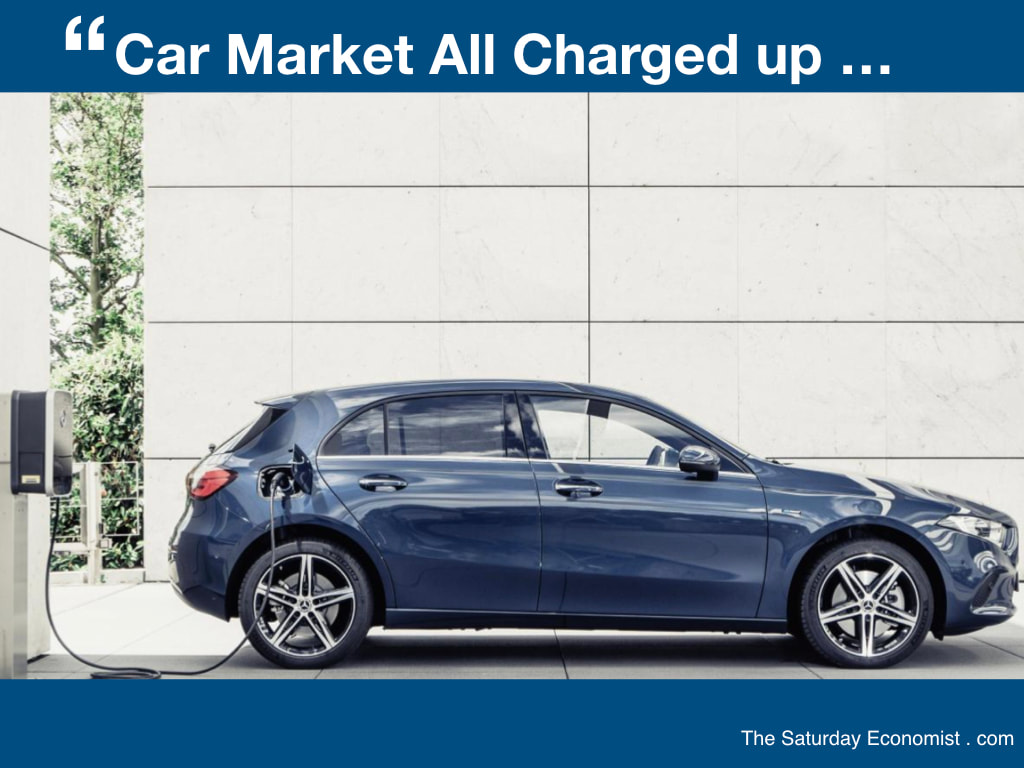

U.K. car sales ended the year down by just 2%, confidence among CFOs bounced back, following the election result. A modicum of clarity over Brexit appeared. The withdrawal bill passed through the house with a majority of 99 votes. Boris Johnson promised a deal with Europe by the end of the year. No extension will be considered, deal or no deal, the old "dead in a ditch" dictum still rules OK. Ursula von der leyen, the new President of the European Commission has made it clear, such a timetable is impossible. It will be a long and drawn out process before any deal is done. In the latest news from the SMMT, UK car sales ended the year down by 2.4% at 2.3 million units. Diesel sales were down by over 20% accounting for just 25% of total sales. Petrol sales were up by 2%, the share of sale increasing to 65%. Hybrid sales are charging up. Alternative fuel vehicle sales increased by 50% accounting for 10% of new registrations. Consumer confusion over diesel continues. Hybrids are sent to overtake the poisoned fuel source within three years. Despite the set back in the UK this year, car sales are charging up, here and around the world. What a difference a deal makes. The latest Deloitte CFO survey, shows an unprecedented rise in business sentiment. Brexit worries dropped to third place in list of concerns. Weak demand at home and geopolitical risks around the world moved ahead of Brexit and protectionism for the moment. Businesses are more optimistic, less uncertain, more confident about profits but still casting a cautious cloak on costs and cash flow. UK stocks closed down, Sterling slipped against the Dollar to hold at $1.30. Mark Carney caution on the year ahead, spooked markets as the prospects of more QE and rate cuts appeared possible. Oil prices Brent crude basis returned to our $65 dollar benchmark ... U.S. Wage Growth Disappoints ... In the U.S. markets rallied as the prospects of World War Three slipped. The Dow and S&P closed up, Nasdaq moved ever higher. Recession indicators moved lower. Markets expect growth of just 1.8% in 2020 compared to 2.3% last year. The U.S. trade deficit fell in November to $43 billion dollars compared to $47 billion prior month. Exports increased by 0.7% as imports fell by 1%. Whilst some rush to acclaim the Trump trade strategy, a slowing economy will provide the best explanation of the modest improvement for now. Latest data on jobs and earnings disappointed. U.S. non farm payroll growth came in lower than expected at 145,000. The unemployment remained steady at 3.5%. Wages increased by just 2.9%, the smallest annual gain since July 2018. More women than men were on the payroll for the first time in ten years. The data marks ten years of continued job expansion in which 22.6 million have found work. Last year employers added 2.1 million jobs, slightly down on prior year. Major job expansion is in the service sector. With education, health and business services featuring. Leisure and hospitality also strong, significant gains were made in construction, distribution and financial services. Any gains in manufacturing, were offset by losses in the mining sector. So much for "Make America Great Again" the blue collar workers are not the beneficiaries of Trump's economics. With continued expansion in prospect and inflation subdued, the Fed is unlikely to make any move on base rates. Ten year bond yields were up by just one basis point at 1.84%. The economy is moderately set for the election in November ... bring on impeachment ... Marching as to war ... Tensions were heightened following the Iranian missile strikes on American bases in Iraq this week. China called for for restraint and the pursuit of a peaceful resolution of conflict. Neither side seeks war, least of all the Iranian government. The Iranian economy is in poor shape following the imposition of sanctions by the U.S.A. in 2018. Economic growth fell by 10% last year following a contraction of 5% in the prior year. Inflation is increasing at 30%, unemployment is rising to just under 20%. Oil exports are falling, the trade deficit is increasing, the internal fiscal deficit is also on the rise. The economy is measured at around $400 billion in the current year. The defense budget at around 3% of GDP is valued at some $12 billion dollars. Compare that to Uncle Sam's coffers and it is clear Iran is in no shape "marching as to war". The US economy is worth about $22 trillion dollars this year. Defense spending at around 3.6% of GDP is expected to increase to $800 billion dollars. that's twice the size of the economy of Iran and well over fifty times the money spent on defense. This week, the Baghdad government called for the withdrawal of all U.S. troops in Iraq. The strategic prize is within reach for the leaders of Iran. Russia is the dominant great power in Syria, China is set to become the soft influencer in the East. It is said President Trump would like to see the return of all troops from the Middle East. For the moment the administration is reserving the right to maintain "whatever force is required to achieve its goals there". If only we knew just what they were ... That's all for this week, have a great weekend. We will be back with more news and updates next week.  What to expect in 2020 ...

We look at the options ... No peace prize for the President, no trip to Stockholm any time soon. No flowers from Tehran, no vases from Pjongyang, Trump has set the tone for his tangent with the axis of evil. It doesn't bode well. How do you like your foreign policy? Sunni side up with a hint of oil on the side. Troops withdrawn from Syria are moving in to Iraq. As the cavalry arrives, US citizens are urged to leave "by plane whilst possible, by any other means when not". Iran has vowed "severe revenge" for the assassination of Major General Quasem Soleiman. Trump has explained this was action to stop a war. "We did not take action to start a war" the President explained. World leaders called for calm. Dominic Raab, called for de-escalation of tensions in the region. Yep that should do it. Markets acted with cynical response. Defense stocks, Lockheed, Northrop and Raytheon moved higher. Oil prices moved up but not by much. Brent crude closed at $68 dollars per barrel. WTI closed up a few dollars more at $62.90. The Dow, S&P and Nasdaq surrendered early New Year gains. It had been a great start to the New Year following gains of around 30% in 2019. In 2019, our major concerns were of Trump and Tariffs, Boris and Brexit. The President has promised to sign a deal with China by the 13th of January. The Prime Minister has promised a deal with the EU by the end of the year. During the past year, world trade growth slowed to standstill, manufacturing output slumped. Output was damaged in North America, the Far East and Europe. The world needs a trade deal. It does not need a major geopolitical conflict played out in the Straits of Hormuz. US growth slowed to around 2.3% in 2019. A further slow down is expected in 2020. The Fed has indicated no changes in rates during the year as a whole. No recession in sight. Election looms in the second half of the year. Following gains of 30% over the last twelve months, we expect little or no market action for the year as a whole. It had looked pretty straight forward as the New Year fireworks exploded. A positive outlook overshadowed by trade tensions with China and Europe. Then down came the drone strike just to add to the uncertainty in the year ahead ... High Street Losses Set to Double ... In the New Year, Debenhams announced the closure of nineteen stores. A further thirty Debenhams units are planned to disappear from the high street this year. Analysts expect some 7,000 shops will be closed in 2020 with the loss of 125,000 jobs. High street losses are set to double, according to the Centre for Retail Research. The rate of closure and job losses last year was 3,300 stores closed and over 62,000 jobs lost. According to official data from the ONS, some 20% of retail transactions take place on line. Exclude food and the number increases to almost one in three transactions lost to the high street. Add price pressures, a margin squeeze, rising staff costs, rent and rates just compound the crisis. The sector faces a severe structural crisis which does not reflect a wider economic malaise. Latest update for growth confirms of just 1% growth in the third quarter. For the year as a whole we expect growth of 1.3% in 2019 with similar growth an upside possibility this year. Want to know more? Don't miss our Brabners Quarterly Economics Updates in Manchester and Liverpool later this month. Investment is unlikely to provide a stimulus to growth as our latest update explains. Output will remain muted, we expect manufacturing output to be just 0.5% in the year. Service sector growth will slow to just 1.2% with some hope for the construction sector, rising by 1.6%. No change in base rates, as inflation remains below the 2% target. We assume Sterling will trade in the $1.30 - $1.35 band with Brent Crude trading around $65 dollars per barrel. The unemployment rate will hover around current levels. A continued deterioration in the trade deficit is expected. We await details of government spending plans and targets for the period of parliament. An increase in annual debt to around 3% of GDP is expected if election promises are to be maintained. Dominic Cummings may be recruiting "weirdos and misfits" into Whitehall, let's hope not too many end up in Treasury ... Fed rates set to stay on hold ... The Fed minutes gave a clear indication base rates are likely to remain on hold during the year. Election purdah will inhibit any action during the second half of the year. Inflation will remain below target, unemployment will remain at current levels, despite the slow down in the manufacturing sector. No need for Fed action despite pressure from the White House. Ten year U.S gilts closed down five points at 1.83% this week. Markets are unsure about the shape of the yield curve by the end of the year. We expect little or no movement in real levels by close of period. It has been a great year for U.S. markets. Nasdaq gains of 36% over the year overshadowed the performance of the Dow (23%) and the S&P (23%). The FTSE was a straggler in comparison, rising by just 12% compared to 25% gains in Germany and France. Of course all gains were flattered by the setbacks in December 2018. Falls of over 10% presented a great buying opportunity. Evidence of over extension in the Nasdaq will moderate our New World enthusiasm in the medium term, we expect limited upside in the year ahead. Our "Empires of the Cloud" Fund (see below) posted gains of almost 50% led by Apple, Facebook, Microsoft and Alibaba. Baidu our only setback, the omission of Adobe (up 47%) our only regret. Markets expect further upside as the race for Artificial Intelligence and Streaming intensifies. That's all for this week, have a great weekend. We will be back with more news and updates next week. Wishing you a Happy and Prosperous New Year, John |

The Saturday EconomistAuthorJohn Ashcroft publishes the Saturday Economist. Join the mailing list for updates on the UK and World Economy. Archives

July 2024

Categories

All

|

| The Saturday Economist |

RSS Feed

RSS Feed

The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The presentation should not be construed as the giving of investment advice.

|

The Saturday Economist, weekly updates on the UK economy.

Sign Up Now! Stay Up To Date! | Privacy Policy | Terms and Conditions | |