Inflation falls, Sterling takes a hit. The headline rate of inflation CPI fell to 2.4% in April from 2.5% in March. Sterling closed lower against the Dollar. Prospects for a UK base rate rise faded. The Pound eased to $1.33 against the Greenback and eased to €1.14 against the Euro.

Will inflation fall further this year? it may be difficult. Energy prices are rising as Sterling falls. Import prices are rising again. The May headline figures were flattered by a fall in service sector inflation. Goods inflation remained at 2.6% but service sector inflation fell to 2.1%. Is this sustainable? I doubt that. Taking a holiday this year? Package holiday costs were up by almost 5%. Want to read a book, while away? Book prices were up by 11%. House Contents insured during the trip? Of course. That will be 9% more this year. Thanks! Petrol costs were up by 23% in the month. The largest downward contribution came from Easter apparently. So much for seasonal adjustment. Producer costs are on the rise. Input prices were up by almost 6%. Crude oil prices were up by 20%. Imported metals and fuel costs were significantly higher. So will inflation continue to fall during the year? Don't be deceived by the April shower. Inflation will still be near 2.4% by the end of year. At least one rate rise this year, should still be priced in. Inflation Forecasts are too optimistic. The rate will stay around 2.4% by end of year. Good news for the Chancellor this week. Borrowing in the first month of the financial year fell by over £1 billion. Government borrowing was just £7.8 billion compared to almost £9 billion last year. In the last financial year, total borrowing was revised down again to £40.5 billion. This makes nonsense of the forecasting performance of the Office For Budget Responsibility. In January the OBR were still expecting an out turn of around £50 billion. Oops! For the current year, we expect borrowing to fall further to around £32 billion. Growth forecasts may be revised up this year to 1.8% from 1.5%. Nominal GDP growth will be around 3.8%. The tax take will be boosted, as austerity continues. The absolute level of debt will continue to rise to £1.8 trillion by the end of the financial year. No end to austerity in sight. No austerity holiday. The package price remains too high for Spreadsheet Phil. [So early in the mid terms at least]. We expect borrowing to fall to around £32 billion in this financial year. The Bank will act if Brexit is a shambles. This, the reassuring message from the Governor. In a speech this week, Mark Carney explained a "disruptive" Brexit would give the British Economy a very nasty shock. If that were to be the case, the Bank of England would do its job and guarantee monetary and financial stability in the UK. We have the tools to do the job. Excellent. Negative rates and more QE? Bring it on ... Carney "We have the tools to do the job ..." Will Brexit be disruptive? Michel Barnier today warned Britain to stop playing "Hide and Seek". That's "Masquer and Chercher" in French. An option to "Chercher La Femme" ... "Find the Lady" who can do a deal perhaps. The EU's chief Brexit negotiator says the UK "must look the reality of the EU in the face". It's a fair point. CU Plus or Max Fac X. There is little point in a divided cabinet, devising models of co-operation, completely unacceptable to the EU. The Irish Border, the ECJ, the fundamental freedoms, all must be addressed, if a reasonable solution is to be achieved. Barnier explains, "The UK must refrain from attempts to recreate the advantages of a shared regulatory system from the outside." "It is the UK that leaves the EU. Britain cannot on leaving, ask us to change who we are and how we operate." Ouch. Over in the USA ... U.S ten year bond yield close below 3% In the U.S. ten year bond rates closed just under 3% this week. The Fed minutes were pretty ambivalent. "The committee expects that economic conditions will evolved in a manner that will warrant further gradual increases in the fed funds rate; the rate is likely to remain for some time, below levels that are expected to prevail in the long run. However, the actual path of the fed funds rate will depend on the economic outlook as informed by the incoming data." Central bank speak.Yep. Jerome Powell Chairman of the Federal Reserve is taking tips from Governor Carney perhaps. Talk of an inverted yield curve, a height to heady for market analysts. Forward guidance forgotten. A tool now discarded. Thrown out of the central bank tool box. So what of central bank independence? Central Banks should not take independence for granted said the Fed Chair in a speech in Stockholm this week. Central bankers should remain independent from political pressure. This enables them to to make unpopular decisions in the economy's long run interest. Raising rates to curb inflation. Turning a deaf ear to political leaders. Blocking Presidents on Twitter. That sort of thing. No one specifically in mind. Just a point in general to be made ...

0 Comments

Churlish to be taking about economics on the day of the Royal Wedding but why not! Old habits die hard. It's a beautiful day in Windsor and in Manchester for that matter. We will be watching the ceremony. Just love those Blues and Royals ...

The latest data on jobs and unemployment were released this week. So what can we learn from the data? Unemployment fell to 1.425 million. The level is down by 120,000 compared to the same period last year. Unemployment fell by 45,000 in the first quarter of 2018 ... This encourages further doubts about the suggested weakness of growth figures in the first quarter. The initial estimate of growth was just 1.2% in Q1. Our forecasts for the current year had to be reduced from 1.8% to 1.5% as a result. The Bank decided to keep rates on hold following the weakness of the data. The implication of the latest data is, growth estimates may have been too pessimistic, especially in construction. Growth estimates may have been too pessimistic, specially in construction ... The unemployment rate was 4.2%. That's the lowest level since 1975. The economy has created 397,000 jobs over the past twelve months. The number of vacancies in the economy was over 800,000 in April. At peak in 2008, prior to the recession, there were just 700,000 vacancies in the economy. Get the picture? There are no signals the economy is in trouble. Growth forecasts will be revised up. The Bank mantra will revert to the February MPC stance. "Rates set to rise, earlier and to a somewhat greater extent". So what of inflation? The Bank of England assumes the worst is over. Inflation will fall through the year. Back on target within the forecast horizon. It was ever thus ... but is this correct? Oil price Brent Crude tested $80 dollars per barrel this week. Sterling fell below $1.35 against the dollar. Imported oil inflation is on the rise again. Earnings increased to 3% in March. Construction wages were up by 6%. Minimum wage rates have been increased. The genie is out of the bottle as far as public sector pay is concerned. Public sector pay is up by 2.4% in March, up from just 1.2% a year ago. Real earnings will be positive in the month of April and May. The squeeze on incomes will be relaxed, stimulating household spending in the year ahead. Inflation forecasts are too optimistic. Inflation will remain around 2.4% by the end of the year. Inflation Forecasts are too optimistic. The rate will stay around 2.4% by end of year. So what can we learn from the latest jobs data? Well quite a lot actually ... so what of the U.S.A. ... U.S. ten year bond rates closed just under 3.1% this week. Mortgage rates, (thirty rate year fixed rate average) jumped to 4.6%. The return to 4.5% ten year bond yields will materialize within a two year time frame. The Fed Blue Dot forecast is for short rates to rise to over 3% by 2020. The Fed is worried about the implications of Trump economics. The GOP fiscal stimulus will exacerbate inflation and the twin deficit dilemma. Trump economics policy is forcing US rates to rise, creating problems in the developing world especially in South America. Argentina has already booked a date with the IMF borrowing team. Such is the requirement to match the currency outflows as a result of the lure of the dollar yield. Trump foreign policy is creating chaos around the world. Old alliances are under threat in South East Asia and in Europe. Merkel and Putin exchange flowers and gifts. "The enemy of my friend is is my enemy" As Trump attempts to become the enemy of all. Peace in the Middle East will not be secured by moving the Embassy in Israel nor by moving the goal posts in the nuclear deal with Iran. Threats on trade and defense spending will not ease tensions within NATO. Threats on trade and defense spending will not ease tensions in South East Asia as far as Japan and South Korea are concerned. Progress on peace in Korea will not be secured by references to Libya and Gadaffi as a threat or a promise in securing talks. Kim Jong-un will not be swayed by promises of White House support to the regime post de nuclearization. Trump has already been seen to walk away from too many international agreements in his tenure in office. NAFTA, TPP, NATO, climate deal, Iran nuclear deal ... mean, petty and vindictive is no basis for policy at home and abroad. Mean, Petty and Vindictive - no basis for policy at home and abroad. Rex Tillerson this week said "I observe a growing crisis of ethics and integrity in the state of American Democracy". Left unconfronted, American democracy will enter its twilight years. Tillerson's relationship with Trump was fraught. His time in government was limited when NBC reported in October, Tillerson had called Trump a "moron". He denied making the remark. The evidence is emerging for the world to see. The theory of countervailing power is in sway. Old allies will develop new friendships accordingly. Trump has his eye on the prize, it's the Nobel peace prize ... strange that ... just a "medal for a moron" perhaps ... That's all for this week, have a great week-end, John Join me at the Big Social Media Conference in July ... Another great event in the pro-manchester calendar!  The Monetary Policy Committee voted to keep rates on hold this week. Given the latest data on GDP growth in the first quarter and the slowdown in inflation, the decision came as no surprise in the end.

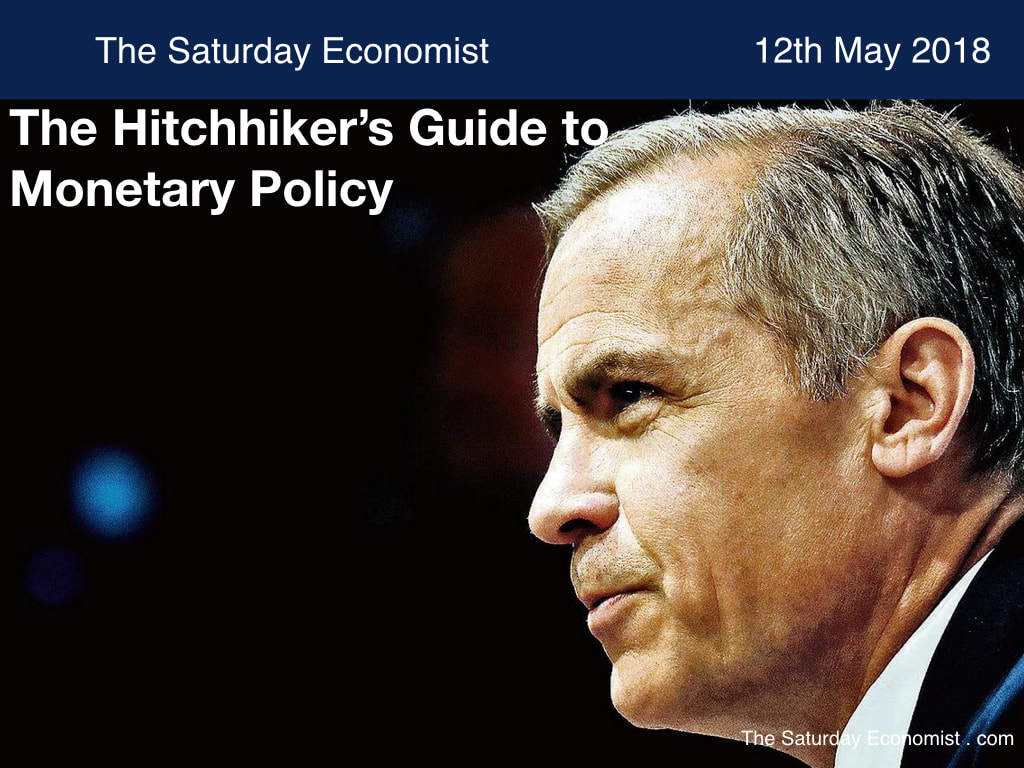

Even so, markets reacted with a further fall in Sterling against the Dollar and the Euro. So what can we make of monetary policy when real short rates are negative, ten year gilts offer a negative real return, with a bonus offer of significant capital loss to redemption? Some comfort may be drawn from the Hitchhiker's Guide to the Galaxy. There is a theory therein, which states that if ever anyone discovers exactly what the Universe is for and why it is here, it will instantly disappear and be replaced by something even more bizarre and inexplicable. I am beginning to feel the same way about monetary policy. If everyone discovers what current monetary policy is for and why it is in place, it will instantly disappear and be replaced by something else. There is a further theory within the Hitchhiker's Guide - the Universe has already been replaced by something even more bizarre and inexplicable. This is probably more evident in monetary policy. Conventional monetary policy has already been replaced by something more bizarre and inexplicable. Alas poor Taylor rule, we knew him well. What is this process of rate normalization, taking place as the economy recovers, that can be blown so easily off course by a bit of snow on the line and ice on construction sites in March? The ONS suggest the Q1 GDP figures were weakened by the harsh weather and snow impacting on the construction sector. The phenomenon will not be reflected in the shape of recovery for the rest of the year as the Governor explains. The Bank now expects growth of 1.4% (1.8%) this year, then modeled at 1.7% for the next three years. Inflation averaging 2.4% this year will return to target within two years. Interest rates are modeled (based on the path inferred by forward market rates) at 0.9% next year and 1.2% by 2021. Forward guidance from the Governor may be dead. Some guidance is offered within "Hitchhikers' ... "the chances of finding out what’s really going on in the universe are so remote, the only thing to do is hang the sense of it and keep yourself occupied". So it is with monetary policy, the chances of finding out what's really going on are so remote, hang the sense of it and keep yourself occupied. Mark Carney has one year left in the role. He is unlikely to take risks with the recovery during his tenure. The Bank is nervous, to say the least, about the impact of Brexit and any decision to leave the customs union. Further caution may prevail before the Governor makes his next career move. In the meantime Hitchhiker's offers some insight into Quantitative Easing ... “Since we decided a few weeks ago to adopt the leaf as legal tender, we have, of course, all become immensely rich.” Excellent ... Beyond the Customs Union ... Thanks for the feedback on the Customs Union piece last week. Economics should not be too complicated especially when it relates to matters of trade. My gravity trade model was further enhanced this week. Attraction based on size of country GDP was exchanged for size of country based on the level of imports. It is an obvious substitution. Import dependencies vary from country to country. (Defined as the ratio of imports to GDP). The UK for example has an import dependency of 24%, China 15% and the USA 12%. The correlation between UK exports and size of country imports improves to 85% from 77% using GDP as the demand variable. Size of country imports determines the pattern of UK trade. Distance also assists the process. Free to trade with countries around the world outside of the customs union will not improve the level of exports. As we explained last week. There are no new territories with which to trade. There are no real gains to be made from opportunities thought to be lost inside the customs union. Theresa May continues to play the long game. The divisions within cabinet persist. The Prime Minister has set up two working groups to develop the options for the Customs Union deal. One team will work on the "Customs Partnership" deal, the other team will work on the "Max-Fac" proposal. The brief to "work towards a joint solution". Some chance. Robot wars would have a better chance of resolving the conflict peacefully. Cabinet is like a troupe of late night drinkers, creating a cocktail with ingredients which do not exist, unavailable at the eleventh hour, with a barman who could never put it together, in a Brussels pub which has already called time. Germany's EU commissioner Günther Oettinger, played down the chances of progress. "Madame May is weak. Boris Johnson has the same hairdo as Trump" he explained. Details of his own interpretation of the gravity trade model were omitted. "We can only hope that sensible citizens will put Madame May on the path to a clever Brexit". Clever Brexit? It is a contradiction in terms. We return to The Hitchhiker's Guide to the Galaxy for the last word ... "It is a well known fact that those people who most want to rule people are those least suited to do it." It must also be true those who would seek to determine the future pattern of UK international trade, in defiance of market forces, are particularly least suited to do it ... "ça va sans dire" ... That's all for this week, Have a great week-end, John  The Conservative Party may have survived the mid term local elections without too much damage. The torture continues in Cabinet. The schism over the Customs Union continues to threaten the future of the Prime Minister.

Free of the EU and the Customs Union, the UK will be able to set up trade agreements around the world without the restrictions imposed by European tariffs and regulation. Truly global Britain will thrive on the world stage. The world will become our oyster, or so we are led to believe. Martin Donnelly, former permanent secretary in the trade department, said recently, "swapping the benefits of full EU membership in exchange for bilateral trade deals at some future date was rather like rejecting a three-course meal now in favor of the promise of a packet of crisps later." A little harsh? Perhaps. The risk is, we will lose trade with the EU but struggle to compensate with new deals in other trade areas. We reject a three course meal, not for a packet of crisps, but for a two course set menu option at a much lower price. In a recent paper, we analyse UK exports in 2017 with the Gravity Trade Model. We ask the question to what extent does the Gravity Trade Model explain the pattern of UK trade? Will we really be better off outside of the EU and the Customs Union? Not really. You can read the more complete note with data sets here. It doesn't bode well for Brexit. Beware, it's a bit geeky! What does the gravity model tell us about UK trade. The *gravity model of international trade* in international economics is a model which predicts bilateral trade flows based on the economic sizes, using GDP and distance between two countries. We analyze the pattern of UK exports in 2017 using the model and conventional regression analysis. The model works well. Size of country GDP is the dominant determinant of trade. Distance adds to the performance of the model. "There are no new territories behind a magic wardrobe..." There are just 195 countries in the world. Together they have a combined GDP of $80 trillion dollars in 2017. The top 50 economies account for over 95% of world GDP. There are no new territories behind a magic wardrobe once we leave the Customs Union. The UK trades with all of the countries among the top 50. In 2017 UK exports of goods were valued at £342 billion. Using the model we can determine in which countries the UK trades well. Conversely we are able to determine in which countries the UK under performs. Barriers to trade ... Using the parameters within the regression model we can determine which are the countries in which we are over performing and those in which we are relatively under performing. As one might expect, the UK over performs in the major EU countries including Germany, France, Ireland and the Netherlands. The UK also over performs in trade with Hong Kong, Singapore and Australia. Trade with North America i.e. the U.S.A. and Canada is adequately represented. There are some surprises in the list. Qatar, Oman, Hungary, Morocco, Macedonia and Kuwait are surprisingly ranked in the UK top 50 trading countries. Some are missing or suggest we are under weight in Argentina, Colombia, Venezuela, Peru, Iran, Philippines, Vietnam and Bangladesh. Sanctions and embargoes can be a barrier to trade sometimes! "Dropping a BRIC..." Significant shortfalls in performance can be identified in trade with Brazil, Russia, India and China. However, membership of the EU does not explain the shortfall. Germany does much better than the UK in the BRIC countries despite the so called restrictions imposed by European tariffs and regulation German Exports to the China, India and Brazil were over four times higher than that of the UK last year. German exports to China were valued at almost $100 billion dollars compared to less than $25 billion for the UK. Exports to Brazil were valued at almost $10 billion compared to $2.5 billion for the UK. Exports to India for the UK were valued at $6 billion dollars, German exports to India were valued at $12 billion dollars. Trade with Russia for the UK was worth just $4.4 billion dollars. For Germany, trade with Russia was valued at almost $30 billion dollars. Product mix and capacity may provide a better explanation of the comparative shortfall in UK performance in the BRIC countries. Neither of which will be enhanced by the decision to leave the EU. There is no economic nor business argument to leave the customs union... Analysis of UK trade and the Gravity trade model suggests there is no business argument, nor is there an economic argument to leave the EU. Neither is there an argument to leave the customs union, in fact quite the reverse. We divide the arguments for Brexit into four boxes, Social, Political, Economic, and Business. The Social, largely about immigration, the Political, about who governs Britain. Argue about this as you will. For the Economic and Business case, there is no argument to leave the EU and certainly no argument to leave the customs union. No need for a ring fence around the Irish Sea. The existing ring fence around the EU customs union will enable truly global Britain to thrive. That's all for this week ... have a great weekend. |

The Saturday EconomistAuthorJohn Ashcroft publishes the Saturday Economist. Join the mailing list for updates on the UK and World Economy. Archives

July 2024

Categories

All

|

| The Saturday Economist |

RSS Feed

RSS Feed

The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The presentation should not be construed as the giving of investment advice.

|

The Saturday Economist, weekly updates on the UK economy.

Sign Up Now! Stay Up To Date! | Privacy Policy | Terms and Conditions | |