The people have spoken. The mistake was to ask. The decision is clear. Britain will leave the EU. No second referendum. No special deal. So long and thanks for all this fish, the EU reaction, finally, rid of those troublesome Brits! Immigration has clarified the divide between the council estates of the UK and the leafy London Terraces. London voted remain, the people of Sunderland want out. Labour supporters face the brunt of the pursuit for better housing and jobs. The pressures on the NHS, housing, social services and education are blamed on Johnny Foreigner. Austerity cuts and badly designed economic policy are really to blame. UK births were near 700,000 last year, dwarfing the inflow of East Europeans from the far frontiers of the EU. Huge pressure on services is a function of low growth and cuts in spending. Osborne is perhaps the real villain in the piece. The threat of a punishment budget, should the people vote to leave, was as economically incoherent as it was political unwise. Osborne has delivered his last budget. He won’t make the move to the job next door. Cameron has resigned. There goes an honest man. Boris Johnson will be Prime Minister. An opportunistic move to back the Leave campaign satisfies political ambition but betrays the interests of the young people of Britain. Our young people, European and citizens of the world, voted predominantly to “Remain”. Great Britain or Little England ... The mission to "Make Britain Great Again", may distil to little England and the sheep farmers of Wales. The EU will make it tough for the UK to secure a deal. No free trade without the free movement of labour and a monthly payment plan will be the minimum deal. To better, is an impossible ask on either side.. The EU leaders must see Britain punished. They cannot afford the malaise to gather momentum in the Netherlands and the dissident states of the North. The Austro Hungarian empire is troubled. The old empire, may seek to reclaim a place in world affairs. Anschluss resentment from German imposition lingers on. Money will be offered to ensure the EU remains intact, albeit bereft of the troublesome Brits. The coffers will be opened to Edinburgh and Belfast (via Dublin) to secure expansion. London must be punished. Scotland will be pushed into a second separation referendum. What golden treasures and whisky whims will be offered to secure Scottish accession to Brussels? The case for a United Ireland has never been stronger. Dublin will receive the EU coin to seduce the reluctant participants in the North. The UK is no longer the fifth largest economy in the world. We slipped a slot as sterling fell. It’s a close call with France. Stripped of Scotland and Northern Ireland the position will be confirmed. How soon will it happen ....? For the moment, there is no rush to hand in our notice. A new Prime Minister will be in place by October. Article 50 will be triggered by the new dream team. EU leaders will not wait. Conversations behind closed doors have already begun to the exclusion of UK. Lord Hill’s position is under threat as the EU Commissioner for Financial Services. There will be no “going back”. No second referendum” No renegotiated deal before exit. The German Finance Minister has confirmed “Out is Out”. Jean-Claude Juncker, EU Commission President has said “The UK government should give effect to the referendum decision as soon as possible”. The witches of Macbeth have stirred their odious pot. “When 'tis done, then 'twere well It were done quickly”. So how bad will it be ...? Sterling - there are no fundamentals behind the fall in Sterling, just technical hedging and positioning. The pound had been hovering around $1.50 as polls closed, then collapsed to $1.32 as the reality of Brexit dawned. When when bulls short, markets overshoot. It’s nothing to do with prospects for the UK. More to do with month end bonus and funding finance for the Flaming Ferraris in the city. The fundamentals will remain for sterling over the medium term. There will be no structural shift in levels, accelerating domestic inflation and forcing an upward rate move. As markets settle, the stability will be restored. The overshoot will be eliminated. It will be business as usual. Moody’s have cut the UK outlook to negative ... More a statement on the prospects for the NHS under Boris Johnson, than it is a serious commentary on the UK economic outlook in the short term. Market Movements- similarly there are no fundamentals behind markets moves for the moment. Foreign earnings and dividends are enhanced as sterling falls. So what’s the real problem in the short term. It will be take five years for a new trade deal to be secured with Europe. Status Quo Ante Referendum the guideline for now. Interest rates, there is no reason for our assumed path of rates to differ following the Brexit vote. The Governor of the Bank of England has stated all will be done to ensure liquidity and stability in the market. Speaking as he did from some Ibsen Doll's House in the city. The Old Lady adds a surreal "Alice in Wonderland" touch. House Prices - may moderate but over pricing was always likely to adjust at some stage especially in London and the South East. Deals on the table are subject to Brexit clauses, now to be consolidated. Government Borrowing - the reduction targets are already under pressure, after just two months into the financial year. The Treasury will struggle to meet the OBR target this year. The monies saved from the EU payments will confront a huge shopping list. It is unlikely the NHS will be a huge beneficiary. The Current Account Deficit at 7% of GDP in the final quarter of 2015 is already a huge problem. We expect the net trade impact to be neutral. But a fall in some foreign investment projects will damage the current account over the medium term. Jobs and earnings - we expect no impact on the jobs market in the short term. Uncertainty has been eliminated. Earnings will rise, as labour supply tightens further assisted by some form of immigration control. Household Spending - Buoyed by rising earnings and a strong jobs market, consumers will adjust to the UK place in world affairs. Consumer spending driven by a younger demographic will continue to expand. Investment - Businesses will begin their scenario planning. Investment spending plans on hold will be implemented assuming full separation from the EU. Areas most at risk will be motor, with tough decisions to follow at Nissan and Toyota. The Mini may make the move to Munich as part of any post Brexit deal. BA has warned profits would be hit by a decision to leave the EU. The travel sector may be damaged. Easy Jet may rebase out of the UK. Brits may travel less to Europe. More tourists may come from around the world if sterling does slump. The net trade impact would be beneficial to the UK. We have a huge tourism deficit. Aerospace will lose the next round of the Airbus contracts. In London, banking and finance will lose the Euro trade to Paris and Frankfurt. International banks will downsize slightly as “Passporting” rules are denied to UK domiciles. “Leaving the Eu will mostly eliminate manufacturing but this shouldn’t scare us” says Professor Patrick Minford. Well it sure scares me ... “We are in uncharted waters without a compass” according to Paul Johnson of the IFS in the Times today. Uncharted waters with nothing but the stars to guide us. We are on our own now, or will be soon. “So long and thanks for all the fish” the reaction from the EU. So what happened to Markets? Sterling fell against the Dollar at $1.375 from $1.432 and down slightly against the Euro at €1.230 from €1.269. The Euro was fell against the Dollar to 1.117 from 1.128. Oil Price Brent Crude closed at $48.70 from $48.70. The average price in June last year was $61.48. Markets, were down - The Dow closed up at 17,503 from 17,674. The FTSE closed at 6,138 from 6,021. Gilts - yields moved down. UK Ten year gilt yields closed at 1.09 from 1.14. US Treasury yields moved to 1.57 from 1.61. Gold closed at $1,316 from $1,292. John That's all for this week ... don't miss our what the papers review every morning @jkaonline. Don't miss our Masters of Strategy Series on Digital Disruption and the New Yahoo Case Study out now! Interested in Strategy? Join our Masters of Strategy on Digital Disruption... Don't miss our regular updates on Corporate Strategy in the Masters of Strategy Series. © 2016 John Ashcroft and Company, Economics, Strategy and Social Media, experience worth sharing. ______________________________________________________________________________________________________________ The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of advice relating to finance or investment..

0 Comments

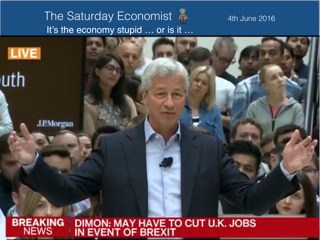

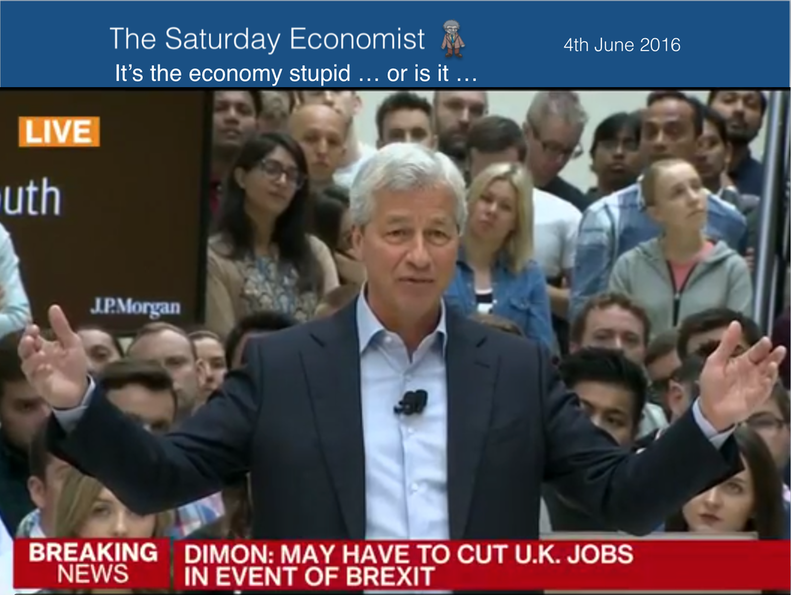

Days before the referendum vote and the Leave camp have momentum. Research by Ipsos Mori this week has Leave on 53% and Remain on 47%. Compare that to a month ago and the figures were reversed. Are we really going to leave the EU? It’s hard to believe but then nearly half of voters think Britain sends £350 million to Brussels every week and Turkey will be fast tracked into the EU. Boris Johnson and Nigel Farage are more trustworthy, it would appear, than the Bank of England, the WTO and the IMF. A simple message, of dubious authenticity, stated with intense frequency is the winning formula. Better still put it on the side of a battle bus and it must be true. Immigration ... Immigration is the touch point issue. The root of all evil it would appear. Problems with the NHS, welfare, schools and housing, then blame immigration and the EU. Make Britain Great again, shut the borders. Deny the economy, the workforce it needs to secure the growth, to fund the services and facilities, we need now and in the future. In the US sanity is prevailing. Hillary Clinton is opening up a six point lead over Donald Trump. Clinton is leading in the polls and in the campaign pot. Republican funding is drying up in the face of the right wing invective. There is no business case to leave the EU. There is no economics case to Leave the EU. The political argument is a Hobson’s choice. The Social argument mainly about immigration. Building a wall along the border with Mexico makes no more sense than building a wall along the white cliffs of Dover. Let the people decide but give them the facts, not some neofacist rhetoric, we will all live to regret. Time is running out to explain why immigration is a good thing for the economy … our universities need the students and our businesses need the workers. Quod Erat Demonstrandum. Jobs and Unemployment … Britain’s unemployment rate fell to the lowest level in more than a decade according to data from the ONS this week. The number of people without a job fell to 1.67 million in the three months to April, 148,000 fewer than for a year earlier. The rate of unemployment fell to 5% from 5.1% prior period. The number of vacancies increased to 749,000 in May. The claimant count in the month was 746,000. The number claiming job seekers allowance was just 591,000. There are more vacancies than people looking for work. There were over 670,000 vacancies in the service sector, predominantly in retail (143,000) and health, welfare and social work. (120,000). Sooner or later labour compression rates will impact on pay … Pay Growth … Pay growth has begun to pick up, suggesting a hike in interest rates by the Bank of England could be on the agenda in the Autumn. Average earnings including bonuses increased by 2.5 per cent in April. Private sector pay increased by 2.7%. Public sector pay was held at just 1.8%. Business services pay increased by 2.6%. The boost in wages was most pronounced in the construction sector, where pay leapt by 10% in the month. If only more East Europeans were bricklayers, then would there be no complaint. Retail Sales … Consumers are spending. Retail sales increased by 6% in May, up just over 3% in value. Online sales increased by almost 22%, now accounting for 14.3% of all retail spending. In food stores, volumes increased by just over 4% but prices fell by 2.5% generating an increase in the value of sales by just 1.6%. It's tough on the street and in the retail parks. Inflation Inflation CPI basis held at 0.3% in May. Goods inflation fell -1.8% driven lower by a drop in food and clothing prices. Service sector inflation increased to 2.6% from 2.4% in April. Education, restaurants, hotel bills and financial services continued to place pressure on the overall service sector price level. Producer prices remain subdued but demonstrating clear evidence of a turning point. If oil holds above $50 through the summer, the Autumn inflation outlook will be materially different. Bank of England … At its meeting ending on 15 June 2016 the MPC voted unanimously to maintain Bank Rate at 0.5%. The Committee also voted unanimously to maintain the stock of purchased assets financed by the issuance of central bank reserves at £375 billion. No surprise there but the bank issued another warning about Brexit. Brexit’ Warnings 'As the Committee set out last month, the most significant risks to the MPC’s forecast concern the referendum. A vote to leave the EU could materially alter the outlook for output and inflation, and therefore the appropriate setting of monetary policy. Households could defer consumption and firms delay investment, lowering labour demand and causing unemployment to rise.' Which way would rates go? We can’t be sure. Lower growth, higher inflation with a fiscal squeeze from the Chancellor? Maybe we should move to the EU ... Over in the U.S. … The US Federal Reserve kept interest rates unchanged this week. Two rate increases are still possible this year, despite a reduction in economic growth forecasts for 2016 and 2017. Fed policymakers gave no indication of when they might raise rates but rate rise next month is still a remote possibility assuming the US jobs market strengthens. Members of the federal open market committee left the target range for overnight lending rates between banks at between 0.25 per cent and 0.5 per cent. Updated forecasts mark annual GDP growth at just 2 per cent for the foreseeable future, slightly lower than the 2.2 per cent projections at the March policy meeting. So what of rates? In the UK, we still expect rates to be at least 0.75% by the end of the year, with two rate hikes to 1% a further (remote) possibility. That’s assuming we vote to “Remain” on the 23rd June. So what happened to Sterling? Sterling held against the Dollar at $1.432 from $1.433 and down slightly against the Euro at €1.269 from €1.2781. The Euro was unchanged against the Dollar to 1.128. Oil Price Brent Crude closed at $48.74 from $50.69 The average price in June last year was $61.48. Markets, were down - The Dow closed up at 17,674 from 17,881. The FTSE closed at 6,021 from 6,115. Gilts - yields moved down. UK Ten year gilt yields closed at 1.14 from 1.23. US Treasury yields moved to 1.61 from 1.64. Gold closed at $1,292 from $1,272. That's all for this week. Don't miss Our What the Papers Say, morning review! Follow @jkaonline and download The Saturday Economist App! Our review of the Brexit facts and figures out now! Download Here! John © 2016 The Saturday Economist from John Ashcroft : Economics, Corporate Strategy and Social Media ... Experience worth sharing. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of advice on investments or finance.   Good news for the economy this week. Manufacturing output increased by 2.5% in April, exports increased by 9% and construction output increased by 2.5%. Great news for the Chancellor, or is it? Some would claim it is good news for the “Leave” campaign. The latest economics data presents clear evidence there is no slow down ahead of the referendum, despite the poll swings over the last few weeks. “Leave” are not focusing on the economy. The Big (I) in the Sky is Immigration, Immigration, Immigration. Voters are worried about the unfettered influx of migrants from the EU and Eastern Europe specifically. The prospect of 76 million Turks living in Torquay and a city the size of Newcastle flashing their EU passports past the douaniers every year, is a real downer for many voters, of left or right. Leave campaigners have found the pressure point. The Prime Minister is in a hole. Having promised to bring down immigration to the “tens of thousands” he is now unable to talk up the real economic benefits of a growth in population of working age. Immigration would be resolved … Don’t worry about immigration. If we were to Leave the EU the economy would slump to such an extent, living and working in the UK may no longer be attractive. An Australian points system would be redundant. Pressure on health, education, welfare and housing would ease. Just as well, there would be no money to fund expansion and no staff to run health, welfare and build the houses in any case. Close run thing … The referendum will be a close run thing. Do “Leave” have the edge? We analyse the arguments into Business, Economics, Political and Social. The latter largely about immigration, the political, largely about sovereignty and who runs Britain. On business and economics we find there is no business case, nor economics case to leave the E.U. Most of the businesses we talk with are of the same view. On politics and social the arguments are much more finely balanced, but that's politics. As for the economics … Manufacturing output increased by less than 1% year on year. The increased driven by developments in transport, pharmaceuticals and food. Most other sectors including metals and capital goods were down year on year. There is no march of the makers and we do not expect much of a revival in the year ahead. If we leave and adopt Free Trade WTO rules in the process, this would mean the end of manufacturing in the U.K. according to Professor Patrick Minford. Patrick is fast becoming the Pol Pot of economics in a post EU world. 2016 would become Year Zero for UK manufacturing and farming if we vote to leave on the 23rd June As for trade … Great news on trade, exports increased by 9% in April. Don’t get too excited. Imports increased by 6%. The trade deficit improved slightly but we still expect the deficit, trade in goods to be around £130 billion this year up from £125 billion last year. The vagaries of Sterling offer little variance. Exports are relatively inelastic with regard to price, even assuming full pass through. Exports are import dependent. We need imports to export. The correlation between goods imports and exports is over 99.3% [1955:Q1 - 2016Q1]. The deficit on goods and services is likely to increase to a record £40 billion plus this year. The prospect of capital flight and pressure on Sterling will become a real risk were we to leave the EU. We are dependent on the influx of capital from the EU and elsewhere to offset the burgeoning current account deficit. (A record 7% of GDP in the final quarter of 2015) As for Free trade, be careful, that for which you might wish. The trade deficit with China was £25 billion last year, up from £10 billion just five years ago. The deficits would deteriorate with free trade rules in place. As for construction … Construction may have increased month on month but output fell by 3.7% compared to April 2015. Public sector housing and public sector infrastructure spending were down by 20%. Private sector industrial build was down by 8%. Commercial real estate increased by just over 1%. The strong growth area was private sector housing up by 15%. Without government spending and a surge in investment, the dismal outlook for construction will continue this year ... So what of rates ..? In the USA, Janet Yellen talks of the resilience of the U.S. economy despite the weakness of the jobs figures last week. Rate rises still an option fro the Autumn? In the UK, we still expect rates to be at least 0.75% by the end of the year, with two rate hikes to 1% a further (remote) possibility. So what happened to Sterling? Sterling closed down against the Dollar at $1.433 from $1.452 and down against the Euro at €1.271 from €1.281. The Euro moved down against the Dollar to 1.128 from €1.133. Oil Price Brent Crude closed at $50.69 from $49.45 The average price in June last year was $61.48. Markets, were mixed - The Dow closed up at 17,881 from 17,782. The FTSE closed down at 6,115 from 6,209. Gilts - yields moved down. UK Ten year gilt yields closed at 1.23 from 1.28. US Treasury yields moved to 1.64 from 1.72. Gold closed at $1,272 from $1,239. That's all for this week. Don't miss Our What the Papers Say, morning review! Follow @jkaonline and download The Saturday Economist App! Our review of the Brexit facts and figures out now! Download Here! John © 2016 The Saturday Economist by John Ashcroft and Company : Economics, Corporate Strategy and Social Media ... Experience worth sharing. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of advice on investments or finance.   Bill Clinton’s 1992 presidential campaign was built on three key platforms, the economy, change and healthcare. It was for Clinton a winning trilogy. In the main, it was the economy. The economy and jobs determine votes. For the EU referendum, the economy may not be sufficient to bring victory to the Remain campaign. The business and economic arguments largely won, the sovereignty options, a Hobson’s choice for many. Immigration is proving to be a big issue with voters. Michael Gove on Sky this week, couldn’t give a guarantee about job retention if the “Leave” campaign was successful. “A group of UK MEPs (and the Prime Minister) may be on the list for starters” he jibed. Jamie Dimon at JP Morgan was explicit. A quarter of his London workforce, would face the chop if the UK were to leave the EU. For sure we know, more jobs in London financial services will go to Frankfurt and Paris if we vote “Leave” on the 23rd June. It’s immigration stupid … or is it? The referendum campaign is focusing on immigration. Control the borders, take England back, make Britain Great again. The prospect of 96 million Turks living in Torquay looms. Turkish accession will just open the doors to the Middle East and North Africa. Where will it all end for Southend? The EU offers a MENA option by the Syrian back door. No wonder voters are confused. Many are unable to distinguish between the immigration agenda and illegal immigrants crossing the Med. "Dinghies in Dover" with illegals aboard are not a function of EU membership. The “Remain” campaign must do better on the immigration. Growth, revenue and job creation are part of the immigration deal. Foreign workers in healthcare, farming and elsewhere are not taking “our jobs”. After all the UK economy created 400,000 new jobs last year. The economy and jobs are vote winners. The Remain campaign must demonstrate, immigration is a positive thing for both. Our forecasts for 2016 … This week we released our forecasts updates for 2016. Growth in 2015 was 2.3% down from 2.9% in 2014. We now expect growth of 2.2% in 2016, following the disappointing performance of manufacturing and construction in the first quarter. The inflation outlook is still muted, with the fall in world oil, energy, food and commodity prices continuing to dominate headline inflation. The UK economy grew by 2.0% in the first quarter, revisions to construction and manufacturing growth pulling total output lower. The service sector continues to drive growth. UK Inflation will average just 0.6% over the balance of the year 2016, with an increase in the second half. Unemployment will continue to fall, government borrowing will also fall. The service sector will lead the recovery as manufacturing and construction output falls slightly. We are forecasting a modest fall in manufacturing of around 0.2% in 2016 with a 0.9% fall in construction activity based on the latest data. The trade figures will continue to disappoint, offset by a further £2 billion oil dividend, despite a moderate oil price recovery. The challenge to the current account following the drop in overseas investment income continues and will present a significant problem to the outlook for sterling over the medium term, in or out of the EU. Growth in the economy is driven by household spending especially in the leisure and retail sector. Manufacturing, construction are foundering. Investment and government spending is slowing. The trade deficit is increasing, the current account deficit looms large. No time to “go it alone”. No re-balancing, no march of the makers, no export surge ... Sterling will be under pressure in or out of the EU. Our forecast is based on a "remain" referendum outcome. To access the update Check out The Saturday Economist Latest Forecast Page. and download the update. Over in the U.S.A … May’s non-farm payrolls figure increased by just 38,000, 73,000 after adjusting for 35,000 striking Verizon workers. The figure, the lowest since September 2010, were below consensus estimates by 122,000 jobs. A June rate hike from the Fed is now “very unlikely”, according to Paul Ashworth, chief US economist at Capital Economics. Job gains in the preceding two months were revised down by a cumulative 59,000. The weakness in May’s payrolls was widespread. Manufacturing lost 10,000 jobs, construction shed 15,000 jobs and temporary help fell by 21,000. The average monthly job gains are now around 110,000 since the start of the year. So what of rates? In the USA, the job figures would suggest a rate rise this month is off the agenda. July remains a possibility but we now may have to wait for the Autumn. In the UK, we still expect rates to be at least 0.75% by the end of the year, with two rate hikes to 1% a further (remote) possibility. So what happened to Sterling? Sterling closed down against the Dollar at $1.452 from $1.464 and down against the Euro at €1.281 from €1.314. The Euro moved down against the Dollar to 1.133 from €1.140. Oil Price Brent Crude closed at $49.45 from $49.22 The average price in May last year was $61.48. Markets, moved down - The Dow closed at 17,782 from 17,867. The FTSE closed at 6,209 from 6,270. Gilts - yields moved down. UK Ten year gilt yields closed at 1.28 from 1.43. US Treasury yields moved to 1.72 from 1.83. Gold closed at $1,239 from $1,213. John That's all for this week. Don't miss Our What the Papers Say, morning review! Follow @jkaonline and download The Saturday Economist App! Our review of the Brexit facts and figures out now! Download Here! John © 2016 The Saturday Economist by John Ashcroft and Company : Economics, Corporate Strategy and Social Media ... Experience worth sharing. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice.  |

The Saturday EconomistAuthorJohn Ashcroft publishes the Saturday Economist. Join the mailing list for updates on the UK and World Economy. Archives

July 2024

Categories

All

|

| The Saturday Economist |

RSS Feed

RSS Feed

The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The presentation should not be construed as the giving of investment advice.

|

The Saturday Economist, weekly updates on the UK economy.

Sign Up Now! Stay Up To Date! | Privacy Policy | Terms and Conditions | |