Employment surge will force rethink on forward guidance …

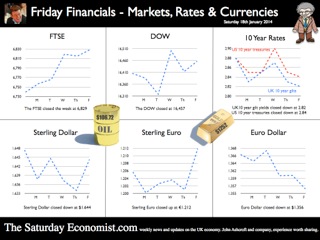

The governor went to Davos this week and also appeared on the Paxman Show. He was asked about unemployment, forward guidance and Bitcoins! Excellent. Unemployment Unemployment fell to 7.1% in the three months to November according to the latest data from the ONS. Over 30 million were in employment up by 280,000 on the prior three months. Good news for the economy and a measure of the strong recovery in the UK, particularly in the second half of the year. The claimant count measure fell by 24,000 to a rate of 3.7%. The unemployed (claimant count) will fall below the one million mark by the end of 2014 based on our current forecasts. This would be in with levels last seen in September of 2008. No need then to worry about household incomes, earnings will begin to recover significantly as the job market tightens through the year. Forward Guidance So what of forward guidance? “Mark Carney has torn up his original low interest rate policy after completely misjudging the speed at which unemployment would fall” according to Phillip Aldrick writing in The Times today. Well not really. It is true the Bank of England model assumed the 7% hurdle rate would be triggered in 2015 rather then by the end of 2013! Nevertheless, the overall parameters of forward guidance remain in tact. The major concern of central bankers is conditioned by the experience of The Great Depression and the Lost Decade. Monetary policy will remain accommodating until the recovery and “escape velocity” from recession is secured. Even then, rates will rise slowly and gradually. It will be some years before a return to equilibrium base rates of 4.5% is achieved, the additional guideline. In the Inflation Report due next month, the bank will consider a range of options to update Forward Guidance. The simplest solution, an update to the unemployment hurdle rate from 7% to 6.5%. The challenge of a more complex hybrid may prove irresistible. As for escape velocity, tapering in the US is expected to accelerate. There seems little justification, if indeed there ever was, to continue to spend Fed dollars on US Treasuries and mortgage debt. 3% growth in the USA economy appears possible this year. That’s a faster rate than in the years leading up to the collapse in 2008. Borrowing Figures The UK Government borrowing figures were released this week. The government is on track to reduce the level of borrowing to between £105 billion and £110 billion this year. Receipts are rising faster than spending and the overall level of borrowing in the first nine months of the year is down by over £5 billion. Inflation down, borrowing down, unemployment down, earnings will begin to rise later this year. The platform for the election is well set. Just the trade figures alone will continue to disappoint as problems in Europe persist. So what happened to sterling? Markets were disturbed by the possibility of more tapering, undermining stock market strength in the USA and destabilizing international capital flows across developing economies. Poor readings from manufacturing data in China and Japan, plus problems with the Argentinian peso created the “perfect storm” for markets at the end of the week. The CBOE Vix volatility index shot up from 13.8 to 18.14 at close. Some way off the 55 level recorded in the depths of despair in 2010 but a measure of late volatility nevertheless. The pound closed at $1.6481 from $1.6422 against the dollar and 1.2041 from 1.2127 against the Euro. The dollar closing at 1.3681 from 1.3538 against the euro and 102.34 104.23 against the Yen. Oil Price Brent Crude closed at $107.88 from $106.48. The average price in January last year was almost $113, so no real threat to inflation from crude oil prices Markets, moved down - The Dow closed at 15,879 from 16,458 and the FTSE closed at 6,663 from 6,829. 7,000 on the FTSE a soft call for the near term, requiring a little more work in progress. UK Ten year gilt yields closed at 2.78 from 2.84 and US Treasury yields closed at 2.72 from 2.82. Yields will test the 3% level as tapering accelerates into 2014 but for this week, the flight to quality led the market. That’s all for this week. No Sunday Times and Croissants tomorrow or for the rest of this year for that matter. We are taking a break in this pre election year. Join the mailing list for The Saturday Economist or forward to a friend. The list is growing as is our research team. John © 2014 The Saturday Economist by John Ashcroft and Company. Experience worth sharing. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice.

0 Comments

“If inflation is the genie, deflation is the ogre that must be fought decisively...” Christine Lagarde head of the IMF was speaking to the National Press Club in Washington this week. With inflation below central bank targets in Japan, USA and Europe, the IMF believe the rising risks of deflation could prove disastrous for the world recovery. Western leaders, haunted by fears of the American Great Depression and Japan’s Lost Decade, are fearful of premature monetary tightening which could threaten the nascent recovery. In folklore, a genie is a supernatural creature who does the bidding once summoned. This may not have been the intentioned meaning by the boss of the IMF but Mark Carney Governor of the Bank of England, could be forgiven the interpretation. This week, the inflation figures for December were released by the ONS. CPI inflation increased by just 2%. For the first time in over four years, the genie returned to target, as would an obedient creature, undertaking the bidding of the new Governor of the Bank of England. The genie is working hard to obey. It has taken some time to get the message into the bottle and the genie back on message! Mission accomplished? With such success, it would be churlish to point out that in the same month, RPI increased from 2.6% to 2.7%, goods inflation actually went up and service sector inflation closed the year at 2.4%. For the moment the wild ride of the last four years has come to a close. As Christine Lagarde stated, “Optimism is in the air, the deep freeze is behind us and the horizon is much brighter.” In further good news, UK manufacturing prices increased by just 1% in December and input costs actually fell by just over 1%. Import prices of metals, parts and equipment fell, reflecting higher sterling values and lower world prices. For the moment, the inflation outlook for 2014 appears benign. Deflation is the ogre ... So what of ogres and deflation. Ogres are monsters in legends and fairy tales that eat humans and are particularly cruel, brutish or hideous. In the UK fears of deflation are not evident. We still expect inflation to hover slightly above target through the year. The ogre of deflation will be banished within the Kingdom. Particularly with earnings on the rise and a Chancellor of the Exchequer, as the handsome prince, up for re election, pledging an increase in the minimum wage to £7 an hour over the next couple of years. Inflation has fallen to target much faster than we had envisaged. The good news - as earnings rise, the boost to real incomes will lead to a sustained level of growth in consumer expenditure and retail sales. Higher but not quite as high as the latest UK data might suggest perhaps! Retail Sales the nymph spirit ... This week, the ONS released the retail sales figures for December. Sales volumes increased by 5.3% and values increased by 6.1% compared to December last year. Despite the fears of the major retailers, the consumer hit the high street with great gusto in the run up to Christmas allegedly. Internet sales, increased by 11.8% and small stores, experienced higher growth with sales increasing by just over 8%. Can retail sales have been so strong in December? Contractions in volume sales amongst food stores and petrols stations adds to the confused picture in the month. According to the ONS, in the three months prior to December, retail sales volumes averaged just 2%. So much for saving for Christmas. The surge in activity in December appears rather high and slightly at odds to the anecdotal evidence from retailers themselves. The BRC, British Retail Consortium suggests sales increased by just 1.8% in December as footfall actually fell. The BDO high street tracker reported sales down in the pre Christmas week with a recovery to 3.5% growth in the final week of the year. Debenhams, M & S, Morrisons and Sainsburys struggled in the Christmas period. Argos, Dixons, Halfords, Primark, Lidl and Ocado amongst the winners in the multi channel race. The 5% growth in volumes reported by the ONS appears to be a high call. So much for lies, damned lies and seasonal adjustment. Shrek shacking up with the Sleeping Beauty ... Ogres returned to the High Street this week as Sports Direct revealed a near 5% stake in Debenhams. Imagine Shrek shacking up with Sleeping Beauty, shudders must have swept around the Debenhams board room. The subsequent put and call option by Sports Direct, just added more confusion to the retail horizon. So what happened to sterling? The pound closed at £1.6422 against the dollar and 1.2127 against the Euro. The dollar closing at 1.3538 against the euro and 104.23 against the Yen. Oil Price Brent Crude closed at $106.48. The average price in January last year was almost $113, so no real threat to inflation from crude oil prices Markets, moved higher. The Dow closed at 16,458 and the FTSE closed at 6,829. 7,000 on the FTSE a soft call for the near term. UK Ten year gilt yields closed at 2.84 and US Treasury yields closed at 2.82. Yields will test the 3% level as tapering accelerates into 2014. That’s all for this week. No Sunday Times and Croissants tomorrow or for the rest of this year for that matter. We are taking a break in this pre election year. Join the mailing list for The Saturday Economist or forward to a friend. The list is growing as is our research and our research team. John © 2014 The Saturday Economist by John Ashcroft and Company. Experience worth sharing. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice.

Ten Predictions for 2014 We begin the year with our ten predictions for the economy in 2014. The professor and his team have dusted off the glass bowl and outlined the benchmark numbers by which we will judge the performance of the UK economy in the year ahead. Slideshare link. Growth up, inflation down, unemployment down, borrowing down, it will all look pretty good for the Chancellor this year - just the trade figures alone will continue to disappoint. The UK cannot grow faster than major trading partners in Europe without a deterioration in the inherent structural trade deficit. Forget rebalancing and the new normal, growth will return to trend rate, pushed by the household and consumer recovery with some contribution from investment later in the year. Working with the GM Chamber of Commerce as their Chief Economist provides huge insights into the business sector. We use the influential quarterly economics survey to develop powerful coincident economic indicators for growth, inflation and employment. Significant indicators of trends in the Greater Manchester, North West and national economies as a whole. Our models of the economy are improving year on year with empirical adaptation as a result. Growth We expect GDP growth in 2013 to be revised up to 2% for the year following a robust performance in the final quarter of the year. The influential NIESR GDP tracker suggests growth was up by 2.9% in the final quarter of the year. Our own GM Chamber of Commerce co-incident indicator confirms the strong growth pattern. Following revisions to GDP released at the end of December, the economy grew by 2% in the second and third quarters. We expect the preliminary estimate, later this month, for 2013 as a whole, to be around 1.8% or 1.9% with a final revision to 2% by the end of the quarter. Last week, the ONS released the manufacturing figures for November. Manufacturing slowdown hits recovery - the headline in today’s Times. Hardly! Growth year on year was up by 2.8% following a 2.5% growth in October. We expect the rally in manufacturing to continue into this year. In 2014, the strong growth in service sector activity will continue with support from manufacturing and construction. We expect overall GDP growth of 2.5% in 2014 possibly rising to 2.7% in the following year. Inflation Inflation CPI basis, fell to 2.1% in November. We are forecasting CPI inflation of around 2.3% in the year ahead. Service sector inflation remains a challenge to the 2% target averaging over 2.5% in the final quarter of 2013. International commodity prices, including oil, should be less of a threat to the UK inflation outlook and some improvement in sterling exchange rates will assist. The oil price outlook appears benign with US shale oil and a lower Chinese propensity to import, moderating Brent crude prices around $110 dollars per barrel for the year as a whole. Unemployment and base rates Growing employment will push the claimant count down to around 3.8% this year and 3.3% next year. The wider LFS indicator will fall to the 7% level by the middle of 2015. Then and only then will the forward guidance from the MPC come under review. We expect base rates to be kept on hold until the middle of 2015, thereafter rising in line with US base rates. Gilt yields on the other hand, we expect to be trading at fair value 4.5% by the end of the forecast outlook. Earnings Stronger growth and a lower claimant count will lead to an acceleration in earnings and household incomes as a whole. The “new normal” may well appear to be the “same old same old” recovery consumer led recovery by the end of the year. Government Borrowing We expect significant improvements in the borrowing figures for this fiscal year and in the years ahead. Revenues in the eight months to November were up by 7% with spending up by less than 2% over the same period. We expect borrowing for this year to be around £105 billion falling to less than £90 billion in 2014/15. Still much to do but growth will restore equilibrium over the next four years assuming spending plans remain under control. Trade Last week the ONS released the trade figures for November. Nothing changes in the outlook. Our forecast deficit trade in goods remains around £110 billion this year rising to £117 billion in 2014. The service sector surplus will offset (in part) the trade in goods deficit. The bad news, - there will be no “net gain to trade” in the years ahead. The good news, there will be no balance of payments constraint to growth, nor a balance of payment crisis and “run on sterling” either. Ten predictions So there you have it. Growth up, inflation down, unemployment down, borrowing down, it will all look pretty good for the Chancellor this year - just the trade figures alone will continue to disappoint. The full forecasts presentation is available below from the Saturday Economist web site or from the new Chamber of Commerce Economics web site. We will benchmark the economy using this forecast outlook as we move through the year. That’s all for this week. No Friday Financials this week and possibly no Sunday Times and Croissants tomorrow. The professor and his team are reviewing the Sunday strategy in this pre election year. Have a Happy New Year in any case. Join the mailing list for The Saturday Economist or forward to a friend John © 2013 The Saturday Economist, #TheSaturdayEconomist, by John Ashcroft and Company, Dimensions of Strategy and The Apple Case Study. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice. |

The Saturday EconomistAuthorJohn Ashcroft publishes the Saturday Economist. Join the mailing list for updates on the UK and World Economy. Archives

July 2024

Categories

All

|

| The Saturday Economist |

RSS Feed

RSS Feed

The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The presentation should not be construed as the giving of investment advice.

|

The Saturday Economist, weekly updates on the UK economy.

Sign Up Now! Stay Up To Date! | Privacy Policy | Terms and Conditions | |