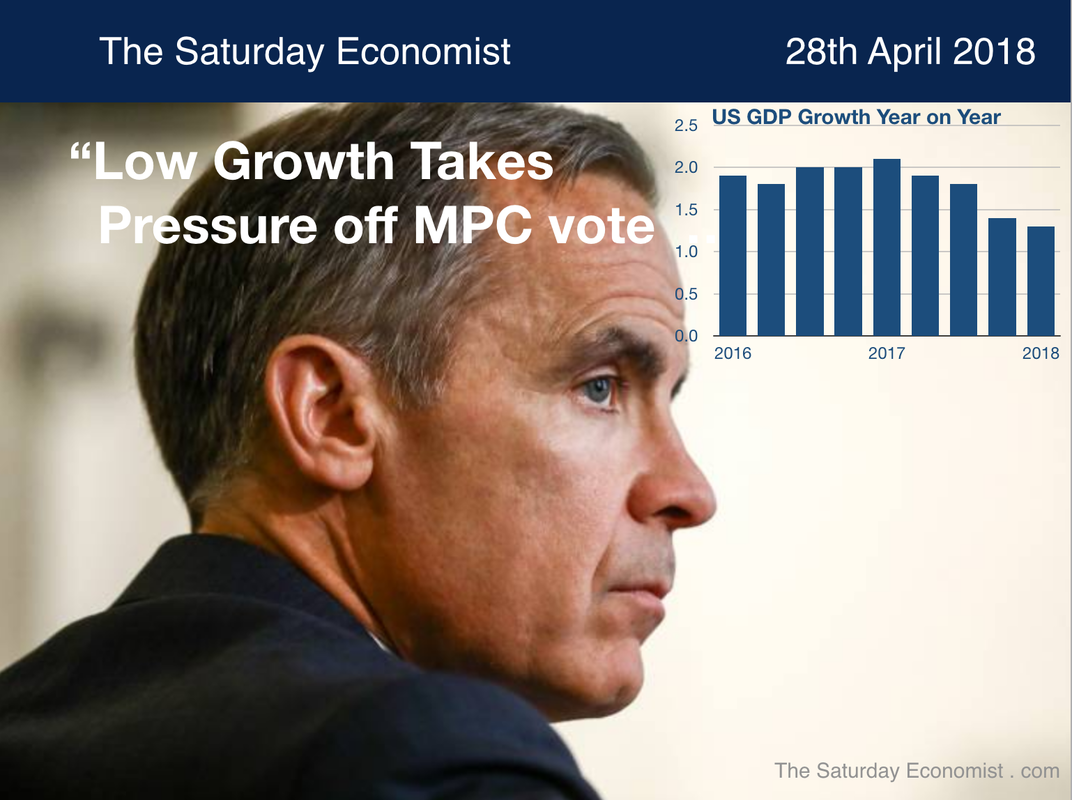

The Preliminary Estimate of UK GDP was released on Friday. Growth in the first quarter was up by just 1.2% compared to 1.8% for the year as a whole in 2017. The economy is slowing exacerbated by a big fall in construction output (down 3.3%).

"You can't lay bricks when the snow is falling", the obvious explanation. But you won't secure real growth in the absence of government activity. Construction may have been hit by the "Beast from the East". But the absence of government expenditure on infrastructure and public sector housing has been the real blight to growth in the sector for some time now. The construction data is incredibly volatile and subject to revision. Remember the preliminary estimate is made with less than half of the data to come as the series is revised in the months ahead. Even so we expect little growth this year from the sector as a whole. "You can't lay bricks when the snow is falling" Without the distortion in construction, growth would have been around 1.5% in the first quarter. One reason we now expect UK growth of around 1.5% for the year as a whole. Manufacturing output increased by 2.5% year on year, despite the drop in car output, where fears about the economy and the "damnation of diesel" persist. Service sector growth was down to just 1.2% with zero contribution from the public sector. The leisure sector increased by less than 1%, attributed to pressures on real incomes and fears about the economy in the months ahead. Business services were up by 1.8% plus there was a heady 2.8% contribution from transport and distribution. "For the economy to stall it is sufficient that good government does nothing ..." For the economy to stall it is sufficient that good government does nothing. Zero growth in the public sector, an absence of real commitment to infrastructure and public sector housing, pressures on local authority cuts. The list is mounting as the process of misdirection continues. The government may blame the "Lack of Investment" in the private sector or "Lack of Productivity Gains" in the labour sector. It is the conjuror's trick of misdirection.There is little or no thought to what's happening in the real economy, as government twists and turns with the torture of Brexit and the Customs Union. What folly there lies within ... Last week we said "It is time to fix the roof, now the snow has blown away". It is clear, low growth in the first quarter will take the pressure off the MPC to raise rates next week ... it will remain an opportunity missed … High growth puts pressure on the Fed to hike rates ... In the U.S.A., growth increased by 2.9% in the first quarter of 2018. Growth has been accelerating since the second quarter of 2016. We expect growth of almost 3.5% this year as the Trump tax give away provides a real stimulus to growth. High growth will put pressure on the Fed to continue the rate hike programme this year and into next. The Blue Dot forecast predicts rates at 3.5% within three years. It seems far more plausible now, as US growth progresses above trend rate. Ten year bond rates closed down, just below the 3% level this week. Why? The headlines in the USA and the UK talk of "slowing growth" not accelerating growth. "U.S Growth Cooled In First Quarter", the headline in today's Wall Street Journal. It is nonsense, based on the bizarre obsession with quarterly growth rates then annualized. The year on year arithmetic is simple and straightforward. The pattern of growth is clear. We expect bond rates to rally into 2018 hitting 3.5% by the end of year. Talk of the inverted yield curve is premature. Ten year bond yields will normalise, long before short term Fed rates. Inversion may occur but not for some time yet. If the yield curve really is the predictor of recession as some insist, it will not be speaking out for some time yet. For now enjoy the ride. Peace in Korea is our footnote this week ... Trump Play or Trump being played ... The historic meeting between Kim Jong-Un and Moon Jae-In bodes well for peace in the Korean peninsula. Trump stands ready to take credit for the progress. Talk of the Nobel peace prize maybe a little premature. But tough talk from Trump is thought to be the catalyst for peace. Is that really the case? Is peace in Korea a Trump play, or is Trump actually being played by the Koreans and the Chinese? Beijing has much to gain from a nuclear free Korean peninsula and a formal end to the war. Unification would open the peninsula to the parasol protection of the expanding Chinese empire and the withdrawal of U.S. troops. The White House is demanding Seoul meets a bill, it will no longer need to pay. Demands to reduce the trade deficit with the U.S. would be facilitated by trade with China to the North. Unification would be as beneficial to Beijing as German Unification was to Bonn. U.S. international policy is conflicted and confused. Moon Jae-In will hedge the risk of a Trump tantrum on trade.The Koreans are mindful China will become the largest economy in the world within ten years. The expansion of the mighty people's navy will guarantee control of the Taiwan straits. Peace in Korea is a win win for Beijing. The dragons will be dancing long before the Trump administration hears the music. That's all for this week, Have a great week-end, John

0 Comments

It all seemed so straightforward. Just a few weeks ago, markets expected rates to rise in May. Two gradual rate rises of around 25 basis points this year would mean base rates around 1% by the end of the year. Two further rate increased of similar dimension in the years ahead, would suggest rates would be around 2% by the end of 2020. All is clear, or so it seemed.

Michael Saunders is a hawk. He voted for a rate rise in March along with Ian McCafferty. At a speech in Strathclyde this week, Saunders argued future increases may be "gradual" but they need not be "glacial". It is a subtle distinction. It must have been very cold in the North of Scotland, the only way to make sense of this. Interest rates would be likely to rise in a series of modest and measured steps. Since Bank of England independence, the MPC has experienced four tightening cycles. Rates on average have increased by 100 basis points over a period of eight months. That is the equivalent of 150 basis points per annum. Now the new "norm" for escalation, is just 50 basis points each year. A 2% level has become the new "neutral" target rate for monetary policy. It is all very strange. A 2% neutral rate is inconsistent with a 2% inflation target. Fisher must be turning in his grave. The neutral rate should be twice as high at least. Even so, with the new "neutral rate", ten year gilt yields would increase to around 3% over two years, from current levels of 1.5%. The implicit capital loss for gilts is around 50%. Andy Haldane has made it clear, QE has created the biggest bond bubble in history. No wonder the MPC is reluctant to pop the balloon with £400 billion of government debt on the balance sheet. Mark Carney made it clear this week, a rate rise in May is no longer a certainty. The economics data is mixed. Unemployment fell to 4.2%, there are 1.4 million out of work. There are over 800,000 vacancies in the economy. Wage growth averaged 2.8% in the three months to February. Recruitment difficulties are increasing. All good reasons for pursuing the path of monetary tightening. On the other hand, the latest retail sales figures were pretty gruesome. Snow kept shoppers at bay, (or on ebay). Car sales are taking the hit from tighter consumer spending and the "Demonisation of Diesel". Growth is expected to have slowed to around 1.4% in the first quarter. Worries about Brexit persist ... and with good reason ... The good news inflation fell to 2.5% in March. Real earnings are increasing again. The outlook for households and consumer spending is improving. If the government committed to spending on housing and infrastructure, growth would be much improved this year. So what happens next? "It is time to fix the roof, now the snow has blown away" U.S. Markets look to higher rates ... In the US markets are expecting rates to rise three or four times this year. Inflation increased to 2.4% in March, growth is expected to be almost 3% in 2018. The unemployment rate is just 4.1% with expectations this will fall to 3.9% by the end of the year. The Trump administration has embarked on a spending spree of $1.3 trillion dollars at exactly the wrong stage in the economic cycle. Both the internal and external deficits are set to expand significantly pushing base rates and bond yields higher and the dollar lower. The government deficit was over $200 billion in February and again in March. For the year as whole the deficit is likely to increase to over $1 trillion dollars. Government borrowing will increase to $20 trillion dollars, that's around 100% of GDP. Within four years, the government will be spending as much on interest payments as it does on the Pentagon and the FBI! The external trade deficit is heading towards $600 billion this year, that's around 3% of GDP. Trump behaves like the Leader of a Banana Republic and is on the economic path to create one. Trump behaves like the Leader of a Banana Republic and is on the right economic path to create one. The Federal reserve "Blue Dot" guideline anticipates rates to increase to 3.5% in 2020 before falling back to around 3% over the longer term. Ten year bond yields are testing the 3% level. 4.5% seems quite attainable in the next couple of years. Our guideline remains, to understand UK rates, follow the Fed and add six months at most. The Bank really should make the move in May and begin the path of "normalisation". The Vera Lynn" School of Economic Thought I am announcing the creation of "The Vera Lynn" School of Economic Thought" with a series of MP3 downloads. Top hits include "Recession Again, Don't Know Where, Don't Know When"; "There will be J curves over the white cliffs of Dover"; "Auf Viedersehen EU" and "It hurts to say goodbye". More tracks to follow ... The Saturday Economist WhatsApp Group On a more serious note, I have created The Saturday Economist WhatsApp Group. If you are on WhatsApp and would like to be involved, just click on this link to sign up! We plan to have some fun with this. That's all for this week, have a great week-end, I had a great break in Gran Canaria, with ten days of sunshine. I have returned refreshed, I missed the key board and the economics! The great thing about addiction, now I know I can stop anytime I like ... John |

The Saturday EconomistAuthorJohn Ashcroft publishes the Saturday Economist. Join the mailing list for updates on the UK and World Economy. Archives

July 2024

Categories

All

|

| The Saturday Economist |

RSS Feed

RSS Feed

The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The presentation should not be construed as the giving of investment advice.

|

The Saturday Economist, weekly updates on the UK economy.

Sign Up Now! Stay Up To Date! | Privacy Policy | Terms and Conditions | |