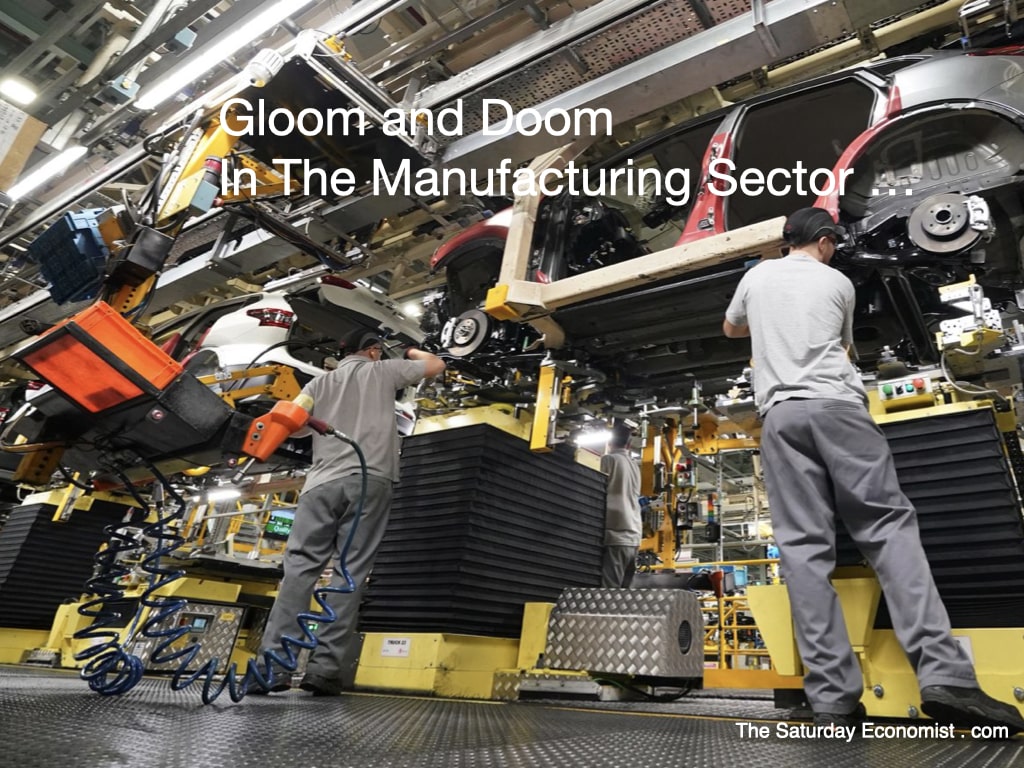

It was gloom and doom in manufacturing this week ...

According to the latest PMI data, Britain's manufacturing sector contracted in August at the steepest pace since Covid-19 lock down. The S&P Global / CIPS final purchasing managers's index (PMI) dropped from 45.3 points in July to 43.0 points last month, the worst reading since May 2020. It was the 13th month in a row the PMI has been below the 50 mark, indicating lack of growth in the sector. Manufacturers are reporting a weakening economic backdrop, as demand is hit by rising interest rates, the cost-of-living crisis, export losses and concerns about the market outlook. However, those firms with orders in hand enjoyed the fastest delivery times since January and the rate of inflationary pressures slowed to 2016 levels. Some price corrections eased the pain for manufacturers who registered a four month high in optimism about opportunities over the next 12 months. Better News from the Vehicle Sector ... It was better news from the vehicle sector. The latest update from Mike Hawes, Chief Executive of the Society of Motor Manufacturers and Traders was quite upbeat. UK car manufacturing notched up a sixth month of growth in July. Commercial Vehicles output knocked out a fourth month of growth. For CV production in particular, the year is turning into a real success story with soaring exports and a steady, stable domestic market driving volumes above pre-pandemic levels. Mike Hawes said "With the worst of recent supply chain difficulties behind us and plants ramping up production of electrified vehicles, the future is looking more optimistic." Vehicle manufacturing was up by 14% in the year to date. Output is expected to hit just under 900,000 vehicles in the year as a whole. A recovery perhaps, but still well down on the output peak of 1.7 million units in 2016. The era of Brexit overhang began. New registrations are expected to hit 1.9 million this year, generating a one million car import liability for the economy. EV's and hybrids will account for 55% of registrations creating a challenge for future growth as the SMMT explains ... Headwinds Ahead ... The changes to Rules of Origin thresholds are due in just four months time. "New Rules of Origin thresholds will pose a significant challenge to manufacturers on both sides of the Channel. The prospect of tariffs and, potentially, price increases on electric vehicles will inhibit sales, investment and production." The SMMT warns. Tougher rules, when applied, underline the critical need for the UK to increase its own battery and EV supply chain manufacturing capability. "Recent announcements are, of course, incredibly important and have helped rewrite the narrative around the UK sector. But we now need government to build on this momentum with a dedicated, cohesive strategy to attract further investment and a developed skills base in battery output and technology." said Mike Hawes. Meanwhile In China ... "Can anyone challenge China's EV Battery dominance", writes the FT last month. Technology breakthroughs and trade barriers will be need to take on CATL and BYD. It's going to be tough. CATL and Shenzhen based BYD have raced ahead of battery rivals in South Korea and Japan, leaving the US and Europe contemplating how to stoke an electric car industry without relying on China for the most important and costly piece of the puzzle. Louis Gave the CEO of Gavekal claims "China is now the biggest automobile exporter in the world, from nowhere five years ago. China now exports more cars than South Korea, Japan, or Germany." "BYD, is the biggest electric car company in the world in terms of production. BYD sells the BYD Seagull. It's a small hatchback, full electric, 220-mile radius, selling for 11,000 US dollars." "They just started selling them in Australia. They sold 10,000 in the first 24 hours, and then that was it. That's all they had. Like the first 10,000, gone, boom. So now they've got to send another 10,000 because, at that price point, you can put it on your credit card". UK Car production under threat ... Dominance in EV production, hegemony in battery supply. A monopoly in rare earth minerals. It is far too early to write off the Chinese economy. China is leading the world in new technology as we argued last week. Brexit overhang, the customs union circle, the rules of origin looming, the option to create a pan European solution for the UK no longer an option. The economies of scale required and the start up risks applying, a volt to British production would require, buyer forward commitments and a government underwrite to make the investment work. Car Production under threat, the SMMT warnings of headwinds to growth could be upgraded to a hurricane caution as the Brexit restrictions draw near ...

0 Comments

Leave a Reply. |

The Saturday EconomistAuthorJohn Ashcroft publishes the Saturday Economist. Join the mailing list for updates on the UK and World Economy. Archives

July 2024

Categories

All

|

| The Saturday Economist |

RSS Feed

RSS Feed

The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The presentation should not be construed as the giving of investment advice.

|

The Saturday Economist, weekly updates on the UK economy.

Sign Up Now! Stay Up To Date! | Privacy Policy | Terms and Conditions | |