Earlier this month is his speech at the Mansion House, Mark Carney, Governor of the Bank of England, referenced the Sterling Crisis of 1931 and imbalances within the economy.

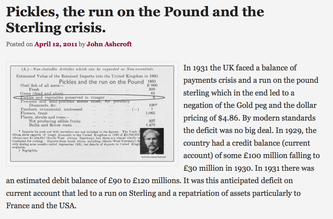

“We need balance. One has only to look back to 1931 when Britain’s economic prospects were strained by a large budget deficit and a deteriorating balance of payments. In 1931 the UK faced a balance of payments crisis and a run on the pound sterling which in the end led to a negation of the Gold peg and the dollar pricing of $4.86. By modern standards the deficit was no big deal. In 1929, the country had a credit balance (current account) of some £100 million falling to £30 million in 1930. In 1931 there was an estimated debit balance of £90 to £120 millions. It was this anticipated deficit on current account that led to a run on Sterling and a repatriation of assets particularly to France and the USA. The problem for the balance of payments was a deterioration in the net receipts from invisible exports largely as a result of the fall in international trade and collapse of shipping revenues. The government was unwilling to raise interest rates to defend the currency given the overwhelming concern re unemployment. The visible account had long been in substantial deficit, despite a surplus on manufactures and semi manufactures. Imports of raw materials and food, particularly food, meant that exports of manufactures and a surplus in invisible earnings had to finance the food bill of the UK population. In 1931, food exports totalled £39 billion but the import bill was £377 billion producing a deficit of £338 million. The proposition to remedy the balance of payments problem was to eat less, import fewer manufactures and export more. Food, drink and tobacco imports should be reduced by 7%, manufactured goods imports should be reduced by 25% and exports of manufactures increased by 25%. A combination of import tariffs and duties would assist in the process. Certain items were considered to be non-essential including shell fish, game, pickles and pickled vegetables, precious stones, feathers, flowers, plants and bulbs. The category of non essentials, totalled £13 million. The “pickled imports” alone cost the UK £6,000 such was the level of detail in the analysis. In 1930 and 1931, the deficit on merchandise trade was £386m in both years and this was offset by invisible receipts of £400m – £420m in 1931, falling to £285m to £315m in 1931 largely as a result of the fall in income from overseas investments. In 1930, the visible deficit was equal to almost 9% of GDP but thanks to the surplus on invisible account the current account was in balance. It was argued there is no problem of the balance of trade so long as the “£ is free to move” as, if the balance is adverse, sterling will automatically fall to the point necessary to maintain equilibrium. “The real problem is to secure such a balance of payments as is consistent with a reasonable exchange values of the £.” (Committee on the Balance of Trade – report January 19th 1932). In September 1931 the British Government suspended obligations due under the Gold Standard Act of 1925 which required the bank to sell gold at a fixed price. As the statement from the Prime Minister Ramsay MacDonald explained. “In the last few days the international financial markets have been “demoralised” and seem intent on liquidating their foreign assets in a sense of panic. Since the middle of July, funds amounting to more than £200 million have been withdrawn from the London market. The withdrawals have been met partly from gold and foreign currency held by the Bank of England, and short term credits of £130 million from the USA and France.” By September 1931, reserves were exhausted. In a chilling note from the Bank of England to the Prime Minister, the Deputy Governor E M Harvey reported : Gentlemen, I am directed to state that the credits for $125,000,000 (£25.7m) and FFs. 3,100,000,000, (£25m) arranged by the Bank of England in New York and Paris respectively, are exhausted, and that the credit for $200,000,000 arranged in New York by His Majesty's Government, together with credits for a total of FFs. 5 millions negotiated in Paris, are practically exhausted also. The heavy demands for exchange on New York and Paris still continue. Under these circumstances, the Bank consider that, having regard to the above commitments and to contingencies that may arise, it would be impossible for them to meet the demands for gold with which they would be faced on withdrawal of support from the New York and Paris exchanges. The Bank therefore feel it their duty to represent that, in their opinion, it is expedient in the national interest that they should be relieved of their obligation to sell gold under the provisions of Section 1 subjection 2 of the Gold Standard Act, 1925. I am, Gentlemen, Your obedient Servant. And so it was, the UK abandoned the Gold Standard, the Pound was left to float, to a level which will automatically produce equilibrium. The rest “as they say” is history. This article was originally posted in April 2011

0 Comments

Leave a Reply. |

The Saturday EconomistAuthorJohn Ashcroft publishes the Saturday Economist. Join the mailing list for updates on the UK and World Economy. Archives

July 2024

Categories

All

|

| The Saturday Economist |

RSS Feed

RSS Feed

The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The presentation should not be construed as the giving of investment advice.

|

The Saturday Economist, weekly updates on the UK economy.

Sign Up Now! Stay Up To Date! | Privacy Policy | Terms and Conditions | |