No tapering, more tampering leads to more questions than answers at the FED. So much for forward guidance.

Despite clear indications “Tapering” may begin in the Fall, the Fed decided to continue the process of QE, purchasing mortgage backed securities at a pace of $40 billion per month and longer term Treasury securities at the rate of $45 billion per month, this week. The objective - to maintain downward pressure on longer term interest rates to support mortgage markets, a fragile housing recovery and to make broader financial conditions more accommodative in the short term, In that way, growth plans for the US economy are not derailed in the recovery phase. The Federal Open Market Committee had been concerned by the rapid rise in ten year Treasury rates by 120 basis points and evidence of low inflation and slightly weaker jobs market. Furthermore, fiscal consolidation and a higher tax burden were likely to damage growth this year. The FOMC reduced their own forecasts for 2013 to around 2.1% from 2.4% in the July review, as a result of recent developments. Should we be surprised by the decision? Should we be surprised by the decision? Well yes and no. In July the mood was more optimistic about the economy. The US economy was expected to growth by almost 2.4% in 2013 and by 3.3% next year. Unemployment was expected to fall towards 7% this year, then down to 6.5% next. Inflation was expected to average around 1.5% next year, with no obvious inflation threat on the horizon. The surprising thing is the revised forecasts haven’t changed the medium term outlook over much. The US recovery is still on track. The growth forecasts have been reduced to a more realistic level for the current year. We still think the USA will struggle to hit the 2% mark but nothing has changed of late to alter that view. So what’s changed? So what’s changed. The FOMC committee has been disturbed by the rally in long rates and the rise in ten year Treasury yields towards 3%. The labour market has seen moderate growth but no reason of itself to step back from tapering. Bernanke’s phone line must have been ringing off the hook by calls from central bankers in emerging markets. Faced with the repatriation of hot monies to the USA, capital outflows and plummeting exchange rates, Brazil, India, South Africa, Indonesia, Turkey and more have confronted the realignment of the US yield curve to some semblance of normality but not without some considerable cost to their own domestic economies. The BISTO kids would have welcomed the continuation of the QE gravy train for now. For the Fed and Bernanke, there is no fall back. They have to get the timing right to begin to tighten policy. “Monetary shocks played a major role in the Great Depression” said Bernanke in Essays on the Great Depression :Princeton 2000 and “Much of Japan’s [lost decade] can be attributed to exceptionally poor monetary policy making” writing in "Japanese monetary policy, A Case of Self Induced Paralysis Princeton in 1999. The Fed cannot be seen to move too soon and damage the recovery. Bernanke would rather hold the patient a little longer on life support, than allow the economy and the markets, to leave intensive care too soon. Will a few months or so make much difference? Not really, sooner or later, and better sooner, QE must be drawn to a close in the USA. What about Base Rates? Despite the delay on tapering, the FOMC believe base rates will be on the rise in 2015 towards 1%. The labour market is likely to hit the 6.5% hurdle rate at some stage next year. The tapering process may begin by the end of the current year or may await the cosmic flip from Planet ZIRP to Planet Janet in January. (Assuming Janet Yellen takes over as lead astronaut at the Fed early in the New Year.) By 2016, US rates are expected to rise to 2% on their way back to a 4% norm over the medium term. Indeed 20% of the fed votes would expect rates to be back at 4% by 2016. So what does this mean for the UK. Our guideline is watch the US and add six months. Fed rates are expected to remain on hold until the end of 2014, rising in 2015 to 1%. By 2016, they may be at 2% or above. In the UK, the MPC’s forward guidance suggests rates may be on hold for three years until 2016. That’s a long way off. For the moment, the decision not to taper but to continue to tamper, will please the markets but only in the short term. The traders will find a reason to test the Fed towards the end of the year. Tapering is coming and so are the rate rises in the USA and the UK. Posted by John Ashcroft. Keywords, Forward Guidance, Tapering, QE, FOMC, Bernanke. © 2013 John Ashcroft, The Saturday Economist, John Ashcroft and Company. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets.

0 Comments

Economics news – for a further week, the good news keeps on coming ... falling inflation, a fall in unemployment plus a boost to retail sales in July ...

Inflation figures were reported on Tuesday. The CPI inflation index fell to 2.8% in July from 2.9% in the prior month. By the end of the year we expect inflation to fall below the 2.5% threshold but the 2% target will be elusive for many months if not years ahead. In October the hefty tuition fees will fall out of the index providing a drop of 20 - 30 basis points. The 2% target will be a challenge - goods inflation averaged 2.4% and service sector inflation averaged 3.1%. Bad news for rail travelers, the rail fares will be indexed to RPI plus 1%. A 4.1% increase in fares is in prospect for 2014, placing additional pressure on retail prices and disposable incomes. The unemployment picture continues to improve, for those who can find work at least. The claimant count fell by 29,000, to a rate of 4.3% in July. The wider LFS data suggests a more modest fall in the three months to June. The rate of unemployment at 7.8% was unchanged, still way above the 7% threshold that may signal a change in monetary policy. Retail sales volumes increased by 3% in July as sunshine and consumer confidence provoked a spending rush, stimulated by sunny weather, a Murray win at Wimbledon and the Royal baby allegedly. Sunny weather boosted sales across a range of products including food, alcohol, clothing and outdoor items. By value retail sales increased by almost 5%. After a slow start to the year, the retail outlook has improved in the summer months. Will this continue? Why not! Employment is increasing and earnings are improving. A further 400,000 are in work compared to this time last year and earnings increased by 2% in the three months to June. We expect the retail rally to continue, though perhaps not at the 3% rate for the rest of the year. Housing - The big story continues to be the housing market. Prices are rising, mortgage activity is increasing, the help to buy scheme is providing a boost to first time buyers. New home build is set to increase by almost 30% this year. The housing market is on the move, time to lock up your fixed rates, as prices rise, the real cost of borrowing is zero, capital appreciation - the bonus. So what does this mean for the year? Our forecast is for growth of around 1.2% plus, rising to 2% in 2014. The economy has turned, the real risk - monetary policy is behind the curve. It is difficult to believe rates will be kept on hold until 2016, watch the US and add six months the best guide as always. Markets were equally sceptical, gilts and treasury yields are rising - gold is beginning to glitter again. What happened to sterling? Sterling responded to the economics news, moving higher. The pound closed at $1.5633, from $1.5505 against the dollar and at €1.1713 from €1.1617 against the euro. The dollar up against the yen closing at ¥97.5 from ¥96.24 Oil Price Brent Crude closed up at $110.40 from $108.22. The average price in August last year was almost $115. We expect oil to average $112 in the current quarter. Markets, were troubled - The Dow fell to 15,081 from 15,425. The FTSE closed down at 6.499.99 from 6,583. It’s a chance for market makers to clean out the bear pit. A good time to make a move. We still think the FTSE will clear 7000 within ten weeks. UK Ten year gilt yields closed at 2.72 from 2.45, US Treasury yields closed up at 2.83 from 2.58. Yields are moving higher, despite the wishes of central bankers. The name is Carney not Canute after all. Gold closed up at $1,377 from $1,315. Still waiting for the next big move but which way? Last week we said, the arguments are building for the bulls. It looks like they have made a decision. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow. Check out The Saturday Economist web site, and the new Chart of the Day Page. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow. The Saturday Economist.com is mobile friendly, no need for a special app any more! Join the mailing list for The Saturday Economist or forward to a friend to let them share the fun! John John Ashcroft is the Saturday Economist, Chief Economist at the Greater Manchester Chamber of Commerce, Economics Adviser to Duff & Phelps and Chief Executive of pro.manchester. The views expressed are personal and in no way reflect the policy statements of organisations with which we work. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice. It's just for fun, what's not to like! Dr John Ashcroft is The Saturday Economist.  Economics news – news in the droppings - understanding market movements

This week it doesn’t get more exciting for economists. The first set of minutes of the MPC under the Mark Carney regime were released on Wednesday. Looking for nuggets of information, amidst the download. A bit like the scene in Jurassic Park when Dr Ellie Sattler is digging with her hands through a pile of dinosaur droppings. Nuggets of information, amidst the download! How did the new Governor vote on QE? How did the other members vote? What was the guidance on forward guidance? Would the ten page minutes be worth the ten thousand minute wait? They were! The death of QE was foretold! “Regarding the Bank Rate and the stock of asset purchases, the Committee voted unanimously in favour of the proposition that base rates and Quantitative Easing (QE) should be kept on hold.” The MPC were united - Carney called time on QE. The epoch of Quantitative Easing draws to a close. David Miles [MPC member] and Paul Tucker [Deputy Governor Responsible for Financial Stability] fell into line with the “new reality”. The pair had been the two QE stalwarts who had “stuck it out” with Mervyn King right to the end of the line. With the economy recovering and inflation rising, it was time to say goodbye to QE. Time for the MPC to wash it’s hands of the monetary experiment, just as Dr Sattler, post examination of the dung, washed her hands before tucking into dinner, we hope. Now we enter the era of forward guidance and intermediate thresholds. The Governor is not ruling out a quantum of additional stimulus. He just needs time to think about the form it may take, plus guidance on the time frame and “triggers” for the new monetary policy framework. Can’t wait for the August deposit. Monetary policy is a bit like genetic experimentation. We have tried M3, shadowing the Deutschmark [An old Germanic monetary medium] and QE. Time for a cautionary word from Jurassic Park’s Dr. Ian Malcolm [Jeff Goldblum], “The kind of control you're attempting simply is... it's not possible. If there is one thing the history of evolution has taught us it's that life will not be contained. Life breaks free, it expands to new territories and crashes through barriers, painfully, maybe even dangerously, but, uh... well, there it is.” And so it is with gilt yields, sooner or later the market will break out, back to equilibrium value, as the period of financial repression and life on Planet ZIRP draws to a close. For the moment, rejoice. QE is dead, it ran out of intellectual currency long ago. In other news ... The good news for the UK economy continued. In jobs data, the claimant count fell by 20,000 in the month to June, an unemployment rate of 4.4%. The wider unemployment rate fell 6,000 to 2.51 million in the three months to May, a rate of 7.8%. Retail sales also presented a positive picture with volumes rising by 2.2% in June after 2.1% in May. On line sales continue to force the pace of change in the high street, with internet sales up by 18% in the month. In the first quarter of the year, retail sales were pretty flat but the second quarter (up 1.7%) offers promise for the rest of the year. Government borrowing figures were also released this week. Good news as the figures for last year were revised down by £2.1 billion to £116.5 billion last year. Not so good news as the borrowing figure for June was slightly higher than June last year. The net figure flattered by the transfer of almost £4 billion from the Bank of England Asset Purchase Facility. The old lady mugged again for gilt coupons under the Treasury - “Money for nothing, gilts for free” campaign. Public sector debt was £1.2 trillion at the end of the month equivalent to 75% of GDP. For the year as a whole, the recovery, if maintained will positively impact on net borrowing. The tax take is rising but spending is resilient to austerity. Nevertheless, the Chancellor may be in a much stronger position by close of year. Inflation, proved to be the real negative in the week. Inflation CPI increased to 2.9% in June from 2.7% in May. The Governor narrowly avoided having to write an explanatory letter to the Chancellor, explaining the missed target. Not to worry, the 2% target is off the agenda for now. We may not see the like in Mark Carney’s term in office. 2.5% by end of year will be challenge enough. Producer prices suggested inflation pressures are rising but not intense. Output prices increased to 2% in June as input costs increased to 4.2%. Home food prices along with energy and oil prices to blame for the latter. What happened to sterling? Sterling recovered further this week closing at $1.5258 from $1.51 against the dollar and up against the euro to 1.1608 from 1.1560. The Euro dollar closed relatively unchanged at 1.3411 and against the Yen, the dollar closed up 100.3 from 99.01. Oil Price Brent Crude closed relatively unchanged at $108.1. The average price in July 2012 was $103 approximately. Markets, were up - The Dow closed up 15,543 from 15,464. The FTSE closed at 6,630 from 6,545. Markets continue to rally. This is the time to average in, albeit slowly into August. UK Ten year gilt yields closed at 2.29 from 2.33, US Treasury yields closed down at 2.48 from 2.59. The feral hogs back in the pen. Yields are set to move higher, the financially repressed will break free from their golden fetters. Gold closed up at $1,292 from $1, 277. Bernanke admitted this week, he didn’t understand gold? I think he was referring to the movements, our theme of the week. That’s all for this week. Check out The Saturday Economist web site, and the new Chart of the Day Page. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow. The Saturday Economist.com is mobile friendly, no need for a special app any more! Join the mailing list for The Saturday Economist or forward to a friend to let them share the fun! John The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice. It's just for fun, what's not to like! Dr John Ashcroft is The Saturday Economist.  Economics news – Don't worry about the double dip ...

Good news - no need to worry about a triple dip, the double dip has been eliminated from history according to the latest release of the National Accounts data from the ONS this week. The hint of a double dip has been smoothed away. The good news continued as the increase in activity was up held at 0.3% growth into the first quarter of 2013. The economy is "healing"! Slightly concerning, the recession in 2008/9 was now worse than we had believed. The economy fell by 5.5% in 2009 compared to the 4% last feared. Despite the rally into the year, the economy remains some 4% below peak in the first quarter of 2008. Worse still the comparison of year on year growth is much lower than first thought. In the first quarter of the year growth was up by just 0.3%. We have to be less bullish about the year as a whole as a result but 1% growth still remains a possibility. Relying on data from the ONS is like planning a mountain trek with a dodgy GPS device. Every so often you tap the tracker and find out you are not exactly where you were led to believe, having arrived by a different route from that last chosen. Who would have thought for example, between 2000 and 2008, the economy grew by almost 3% a year. Had only we known, we had it so good, the Governor could have taken away the punchbowl much earlier. In the USA, the feral hogs could have been put out to grass and the heavy drinkers could have been weaned from Wild Turkey to cold turkey much earlier in the process. For lovers of nominal GDP targeting the revisions should be a clear warning. Nominal GDP grew by an average 5.5% over the period 2000 - 2008. The problem for policy makers, the GPS device was on the blink, with only a sporadic reading available. For lovers of forward guidance, the reaction of bond markets to Bernanke’s comments on QE and tapering, should also be a warning. The statement led to a 100 basis point jump in Treasury yields. The market “over reaction” led to criticism of by the Dallas Fed chief, “Traders are behaving like feral hogs”. “Investors shouldn't overreact to the central bank's plan to reduce the pace of asset purchases”, the Dallas Fed chief Richard Fisher said in an interview with the Financial Times this week. Investors behaved like "feral hogs" after the comments by Bernanke. "What we're talking about here is dialling back," said Fisher, president of the Federal Reserve Bank of Dallas. “I don’t want to go from Wild Turkey to Cold Turkey”. For the more technically inclined. Wild Turkey Bourbon is super-premium American bourbon, made in Lawrenceburg, Kentucky by Master Distiller Jimmy Russell. Forward guidance is a market feed programme by which feral hogs can increase market volatility and trading volumes. Dialling back, is a wish that Bernanke would make a few telephone calls before making a few market calls. After all, we all love to hedge, even Fed chiefs. Back to the ONS stats, by the end of 2012, the economy was some 11% below trend rate at a cost to the economy of some £200 billion in lost output and a cost to Treasury of over £80 billion in lost revenue. Hence the challenge of the spending review this week. The Chancellor obliged to cut a further £15 billion from spending in 2015/16. Radical changes to the level and composition of public spending will continue but spending cuts will achieve little without significant economic growth. For a more detailed analysis check out the IFS web site. In the absence of growth, the IFS warn that further consolidation may require tax rises and spending cuts to hit the targets in the future. Furthermore there appears to be little boost to infrastructure spending, according to Paul Johnson Director of the IFS, “What the Chancellor, did not announce was an increase in public sector net investment. Despite the hype net capital spending is not set to rise”. Jonathan Portes and the Krugmanites will just love that. What happened to sterling? Sterling fell further on dollar strength to 1.5220 from 1.5425 and slipped against the euro to 1.1687 from 1.1757. The Euro dollar closed at 1.302 from 1.3115 and against the Yen, the dollar closed up 99.12 from 97.8. Oil Price Brent Crude closed at $102.16 from $101. Average prices in June were some 9% higher than June 2012. Markets, The Dow closed up 14,910 from 14,799. The FTSE closed at 6,215 from 6,116. Markets have rallied from lows, could be time to average in. UK Ten year gilt yields closed at 2.46 from 2.42, US Treasury yields closed down at 2.49 from 2.54. The feral hogs will have their say. Yields are set to move higher. Gold closed down at $1, 232 from $1293. Worshippers of the old relic at a loss, as we begin the exodus from Planet ZIRP. Check out The Saturday Economist web site, and the new Chart of the Day Page. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow. The Saturday Economist.com is mobile friendly, no need for a special app any more! Join the mailing list for The Saturday Economist or forward to a friend to let them share the fun! John The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice. It's just for fun, what's not to like! Dr John Ashcroft is The Saturday Economist.  Andy Haldane warned this week : “Let’s be clear, we have intentionally blown the biggest government bond bubble in history” speaking before the Treasury Select Committee. Andy Haldane is the director of financial responsibility at the Bank of England. His views were quickly distanced by Old Lady of Threadneedle Street, as very much a “personal view”. OK bond markets may be the main risk to financial stability but best not to speak of it in public.

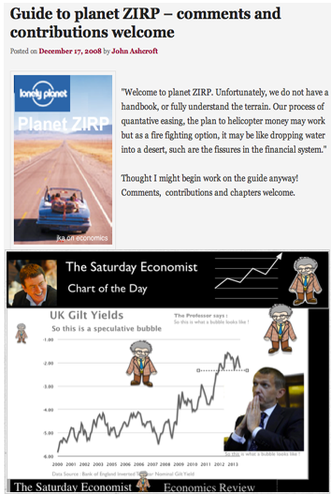

Not to worry, the markets will get the message in the end. High bond prices and absurdly low yields are a by product of life on Planet ZIRP. With short rates at or near the zero interest rate policy level, undermining long term rates was considered to be the next great step. Who could possibly think that creating a financial climate with negative long term real rates, would encourage lending, in an uncertain business world. Well Ben Bernanke for one. There is no “Lonely Planet” Guide to life on Planet ZIRP as we pointed out in December 2008. Commenting on a paper by Bernanke - we said then - “OK it’s official, the effects of QE remain quantitively quite uncertain. Welcome to Planet ZIRP. We don’t have a hand book or fully understand the terrain. We cannot be sure QE is going to work at all. The process of quantative easing, the plan to helicopter money may work but as a fire fighting option, it may be like dropping water into a desert, such are the fissures in the financial system” We also said, “This is your captain speaking, Welcome on board flight QE 2009. I hope you have a nice flight, I am relatively new at this, haven’t actually flown before, we shall be flying by the seat of our pants but have every confidence, we will get somewhere, but not sure where, in the end.” QE was an experiment which is still five years late unproven. We warned then, Planet ZIRP, would be a desiccated sterile planet where a liquidity crisis is exacerbated and prolonged. Now, five years on, the US markets are beginning to fret about the end of the Bernanke flight, with fears of a crash landing in prospect. As Sam Fleming, warns in The Times today, “the Governor of the Bank of England, in 2009, described the process of reversing QE as completely straightforward. It is proving to be a nightmare. “ In the Saturday Economist we pointed out last week, The Bank of England has mopped up almost 75% of UK gilt purchases since QE began. There can be no reversal of QE in the UK. The gilts will be held to redemption. The real challenge - who will buy the gilts at negative real rates, now the Old Lady has to stay off the street. For earlier posts Google “Planet ZIRP - John Ashcroft” , or check out this post you had been warned! What happened to sterling? Further dollar weakness the story, this week as fears over QE3 increase. Sterling rallied to 1.5703 from 1.552 dollar basis and held at 1.1763 against the Euro. The Euro dollar closed at 1.3345 from 1.3216. Against the Yen, the dollar closed once again below the critical 100 level at 94.06 from 97.60. Oil Price Brent Crude closed at $105.93 from $104.56. In June last year Brent Crude averaged $95! The best for inflation may be over, oil prices will be up 10% this month compared to last year. Markets, The Dow closed at 15,070 from 15,248. The FTSE closed at 6,308 from 6,411. The easy calls have been made, time to stand aside whilst the markets consolidate and fret about QE. UK Ten year gilt yields held at 2.08 from 2.09 - US gilt yields closed down at 2.13 from 2.18. The great rotation - in a bit of a spin. As for gold, closed at $1,390 from $1,384. The excitement is over for now, this is a hung chart. Really pleased this week to be appointed as the Chief Economist at the Greater Manchester Chamber of Commerce. Looking forward to working with Clive Memmott, and the team in Manchester. John The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice. It's just for fun, what's not to like! Dr John Ashcroft. |

The Saturday EconomistAuthorJohn Ashcroft publishes the Saturday Economist. Join the mailing list for updates on the UK and World Economy. Archives

July 2024

Categories

All

|

| The Saturday Economist |

RSS Feed

RSS Feed

The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The presentation should not be construed as the giving of investment advice.

|

The Saturday Economist, weekly updates on the UK economy.

Sign Up Now! Stay Up To Date! | Privacy Policy | Terms and Conditions | |