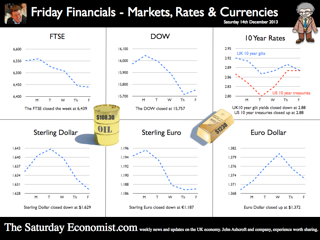

Economics news – the spirit of Christmas present is a cheerful spirit ... The spirit of Christmas Past - should not be forgotten. The spirit of Christmas Present - is a cheerful spirit. The spirit of Christmas Yet to Come suggests that it is unlikely that equilibrium interest rates will return to historically normal levels any time soon”. Excellent. Don’t you just love a central banker with a Christmas message. Governor Carney was speaking in New York this week at the Economic Club of New York. The Governor is anxious to secure the message, interest rates will not rise any time soon. The recovery will not be put at risk. The UK will achieve escape velocity from a liquidity trap, avoiding secular stagnation in the process. Forward guidance is the new policy mantra, secular stagnation the new spectre on the blog. The UK is set for recovery, despite the prophets of gloom on either side of the Atlantic. Forward guidance is integral to the central bankers response to the recession and setback. FG reduces uncertainty, providing reassurance that monetary policy will not be tightened before the recovery is sufficiently established. Businesses will have the confidence to invest. Households will have the confidence to spend. A liquidity trap is avoided. A liquidity trap occurs when the short-term nominal interest rate hits the zero lower bound. Typically in a liquidity trap, inflation is low, the equilibrium real interest rate is negative, creating a persistent inability to match aggregate demand and supply. Businesses won’t invest and consumers are reluctant to spend, aggregate demand continues to fall and a deflationary spiral develops. Fiscal constraints ensure Government spending cannot bridge the output gap. In the UK, the financial crisis pushed the equilibrium real interest rate to the lower bound. With nominal interest rates stuck at zero, and inflation low, monetary policy was unable to push actual real rates to a level low enough to generate growth allegedly. “Pushing on a string, is no way to wag the dog”. I think Keynes said that. Hence the emergence of QE on Planet ZIRP. Allegedly, a way to stimulate liquidity AND activity. In reality, a great way to undermine the gilt curve and returns to savers and investors in the process. So what of secular stagnation? Larry Summers had recently raised the spectre of secular stagnation at the IMF meeting in November in honour of Stanley Fischer, guru of monetary theory at MIT. Secular stagnation, a concept first developed by Alvin Hansen in the 1920s suggested the “new normal” in the USA (post depression) was of lower growth, primarily a result of lower population growth and technological exhaustion. No new things to boost productivity, that sort of thing. Larry Summers, resurrected the term, suggesting the short term real interest rate consistent with full employment may have fallen to -2% -3% in the middle of the last decade. “The natural and equilibrium interest rates may have fallen significantly below zero”. “We may have to think about how we manage an economy in which the zero nominal interest rate is a chronic and systemic inhibitor of economic activity holding our economies back below their long run potential.” he said. In theory, the Fed funds rate can be kept at ZIRP forever but it is much harder to do “extraordinary additional stuff” forever” either in the form of QE, or government deficit funding perhaps. This said Summers, is “my” lesson from this crisis which the world has “under internalised”. Actually Summers went on to say “Now this may all be madness and I may not have this right at all”. Mmm. Stuck on Planet ZIRP, QE was introduced, the effect of which, was to ensure we were marooned on the planet for longer. ZIRP creates of itself a problem which is compounded by QE. In the UK, QE has lost intellectual credibility and momentum but in the USA the persistent purchase of Treasuries and Mortgages (CMBS) continues, achieving no more for Uncle Sam, than a monthly dispensation into a NASDAQ tracker fund. It really is time to begin tapering in the US, end QE and return the equilibrium rate of interest to a natural rate. A natural rate for gilts and treasuries, which reflects an inflation hedge and a real rate of return to risk. In his speech, Summers said, “we have learned one thing, finance cannot be left to the financiers”. Perhaps but then I have always felt much the same about monetary economics. We should begin to think how we can manage an economy in which the academics are confined to campus and not allowed near policy levers. The concept of a negative equilibrium interest rate, which may have fallen to -3% pre recession is as incomprehensible, as life on Planet ZIRP without oxygen. The escape from ZIRP and the beginning of recovery can only be accelerated by an end to QE. Let the free markets free and end QE - the cry. It is time to suggest “Schools out for Summers” and the MIT class of 14462. The US is set to grow by over 2.5% next year or has no one noticed. Back in the UK Back in the UK, as expected the march of the makers picked up the pace in October. Manufacturing growth year on year increased to 2.7% in the month. Construction output grew at over 5% in the latest data for October. The trade figures on the other hand continued to disappoint. The UK's deficit on trade in goods and services was estimated to have been £2.6 billion in October 2013, unchanged from September. The deficit of £9.7 billion on goods, partly offset by an estimated surplus of £7.1 billion on services. Yes, the march of the makers is picking up pace, momentum is “building”, investment plans will be brought back to the board room, just the trade figures alone will continue to disappoint, as the UK recovery gains pace. What happened to sterling? The pound closed at £1.6294 from £1.6346. Against the Euro, Sterling closed at €1.1856 from €1.1922. The dollar moved down up the yen closing at ¥103.2 from ¥102.8 and closing at 1.3740 from 1.3700 against the Euro. Sterling is on a rally which has led to a break out above £1.60, but €1.20 still presents significant overhead resistance. Oil Price Brent Crude closed at $108.83 from $111.61. The average price in December last year was almost $110, so no threat to inflation. Markets, US moved lower - The Dow closed at 15,755 from 16,020. The FTSE closed at 6,434 from 6,552. 7,000 FTSE now a tough call before Christmas. The markets still nervous until tapering finally begins. UK Ten year gilt yields closed at 2.90 from 2.91 US Treasury yields closed at 2.87 from 2.86. Yields will test the 3% level over the coming months but this will await the New Year. Gold closed at $1,239 from $1,231. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow and watch out for news of our Monthly Markets updates coming in the New Year. John Join the mailing list for The Saturday Economist or why not forward to a colleague or friend? © 2013 The Saturday Economist. John Ashcroft and Company, Dimensions of Strategy. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice. It's just for fun, what's not to like! Dr John Ashcroft is The Saturday Economist.

0 Comments

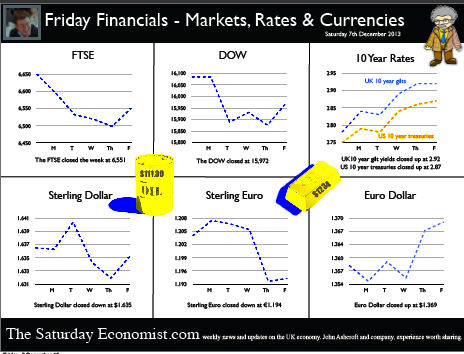

Economics news – fixing the roof whilst the sun is shining ... “Britain’s economic plan is working but the job is not done”, said Chancellor Osborne in the Autumn statement this week, “we need to secure the economy for the longer term”. Yes the Chancellor is intent on fixing the roof despite the sunny OBR outlook. The office for Budget Responsibility has revised up forecasts for the economy with growth of 1.4% expected this year and 2.4% next. Better still, borrowing is expected to fall significantly. The government is expected to borrow £111 billion this year, falling to to £96 billion next year, then down to £79 billion in 2015-16. By 2018-19, the OBR forecast the government will not have to borrow anything at all. Back from the brink of bankruptcy indeed. Growth is up, the deficit is down, unemployment is down, inflation is falling, spending will be kept under control, the government has an economic plan that is working. Who said the pasty tax was such a bad move? We even expect a much stronger performance from investment over the next two years. Just the trade figures alone will continue to disappoint. “Britain is currently growing faster than any other major advanced economy”, [which of itself will create a significant balance of payments problem for the UK economy]. "Exports are growing but they are not growing as fast as we would like", said the Chancellor. The Prime Minister’s visit to China this week is the latest step in this government’s determined plan to increase British exports to the faster growing emerging markets. We are even offering pig semen, to boost pork output in the Chinese economy apparently. So this Autumn Statement is fiscally neutral across the period. No giveaways. Government will ensure that debt continues to fall as a percentage of GDP. This means capping welfare to keep it under control and extending the working life to limit pension payments over the longer term. Business rates are to be capped, with some reduction in department spending to offset the revenue loss. The Bank levy will be increased slightly and the troops will be brought back from Afghanistan, saving lives and money in the process. All in all, this is a play it safe spending review, with a strong recovery in process. Fixing the roof, whilst the sun is shining. Yes, the sun has got his hat on and the Chancellor has a smile on his face” PMI Markit Surveys The good news continued from the PMI Markit Survey data this week, with manufacturing, construction and services all continuing to show strong growth. The recovery is extending across all sectors. Even the slow march of the makers will begin to pick up some speed this quarter. Over in the USA In the USA, growth figures for the third quarter reveal the economy grew by 1.8% year on year in real terms. The US economy will grow by around 1.8% this year, that’s actually faster than the UK but who would want to trouble an Autumn statement with facts. In the USA, more good news, unemployment data in the US fell faster than expected last month. 203,000 jobs were created in November pushing the unemployment rate down to 7%. Tapering is back on the agenda, with some speculation the cut back could begin this month. Courtesy would suggest the decision should await the move to Planet Janet in the New Year. Either way, tapering will begin soon and US base rate rises may be in prospect in 2015. What happened to sterling? The pound closed at £1.6346 from £1.6360. Against the Euro, Sterling closed at €1.1922 from €1.2045. The dollar moved down up the yen closing at ¥102.8 from ¥102.4 and closing at 1.3700 from 1.3582 against the Euro. Sterling is on a rally which has led to a break out above £1.60, but €1.20 still presents significant resistance. Oil Price Brent Crude closed at $111.61 from $109.65. The average price in December last year was almost $110. Markets, were tapered - The Dow closed at 16,020 from 16,086. The FTSE closed at 6,552 from 6,650. 7,000 FTSE now a tough call before Christmas. The markets are nervous until tapering begins. UK Ten year gilt yields closed at 2.91 from 2.78 US Treasury yields closed at 2.86 from 2.75. Yields will test the 3% level over the coming months but this may await the New Year. Gold closed at $1,231 from $1,252. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow and watch out for news of our Monthly Markets updates coming in the New Year. John Join the mailing list for The Saturday Economist or why not forward to a colleague or friend? © 2013 The Saturday Economist. John Ashcroft and Company, Dimensions of Strategy. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice. It's just for fun, what's not to like! Dr John Ashcroft is The Saturday Economist.

The release of the second estimate of GDP in the 3rd quarter brought few surprises. Growth was confirmed at 1.7% year on year following growth of 1.4% in the second quarter.

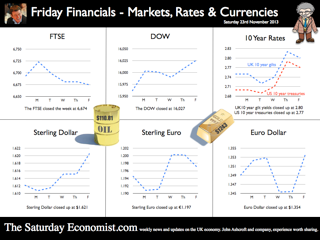

Service sector output continues to drive the recovery with particularly strong growth in the leisure sector. Construction output increased by 4% with manufacturing growth relatively flat in the latest three month period. In current value spending terms the economy grew by 3.8% as incomes of employees and businesses continued to show strong growth. Expenditure within the economy was driven by household spending up by 2.4% in real terms plus a build up in inventories. Government spending was up by just 1.1%, investment fell slightly and the trade figures continue to disappoint. Exports fell and imports increased as UK domestic demand exceeded the rate of growth in Europe and the USA. So what does this all mean? We expect strong growth to continue into the final quarter with overall growth around 2.4% bringing the year on year growth rate to 1.3%. We still think the economy is on track for growth of around 2.4% in 2014. Check out our latest publication “Modeling GDP(O)”. We release the forecasts of the ten key sectors and sub sectors in the UK economy over the next two years. Should we too worried by the lack of investment? Not really. At this stage in the cycle we would expect investment to be weak. Plant and machinery accounts for just 20%, of total investment. Spending on commercial real estate will continue to be subdued for some time yet as the overhang continues. We expect strong growth in productive capacity in the final quarter of the year and into next year. The four year capital stock model is down by just 15% from the peaks of 2008. No need to worry about “lost output” for the years ahead, trend rate of growth can be recovered and maintained. Investment will receive a significant boost in the final three months of the year and into next. Our UK investment model will be released next week. Prospects for the UK look good, but without a strong recovery in Europe and sustained growth in the USA, the trade figures will continue to be a net drain on overall performance. This should be no surprise to regular readers! The trade deficit in goods will increase largely (but not entirely) offset by a strong performance in service sector exports. Is this the wrong kind of growth? The UK economy has been dependent on domestic consumption since our records began. Growth based on investment and exports a policy dreamboat. There will be no rebalancing of the economy just more of the same to come. Bank moves on mortage lending Which is perhaps why the Bank of England modified the terms of FLS away from mortgage lending towards business loans. The old lady is no fan of the help to buy votes scheme. The Governor has made it clear the Bank of England will move to prevent another housing boom. The policy response includes several options this time around including post code selective spread and capital provisions to curb excessive movements in house prices if necessary. What happened to sterling? The pound closed up at £1.6360 from £1.6215. Against the Euro, Sterling closed at €1.2045 from €1.1966. The dollar moved down up the yen closing at ¥102.4 from ¥101.3 and closing at 1.3582 from 1.3555 against the Euro. Sterling is on a rally which has led to a break out above £1.60, pushing through resistance at €1.20 euro basis. Oil Price Brent Crude closed at $109.65 from $111.05. The average price in November last year was almost $110. The average price just $106 this year. Markets, US pushed higher - The Dow closed at 16,086 up from 16,065. The FTSE closed at 6,650 from 6,674. 7,000 FTSE still the call before Christmas. UK Ten year gilt yields closed at 2.78 from 2.79 US Treasury yields closed at 2.75 from 2.74. Yields will test the 3% level over the coming months but this may await the New Year. Gold closed at $1,252 from $1,244. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow and watch out for news of our Monthly Markets updates coming in the New Year. Join the mailing list for The Saturday Economist or forward to a friend UK Economics news and analysis : no politics, no dogma, no polemics, just facts. John © 2013 The Saturday Economist, #TheSaturdayEconomist, by John Ashcroft and Company, Dimensions of Strategy and The Apple Case Study. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice.  Economics news – no Flowers by arrangement ... Treasury Enquiry ... The Treasury has ordered an independent investigation into events at the Co-op Bank including the circumstances surrounding the appointment and governance of Paul Flowers. The former Chairman of the Bank was arrested on Thursday night, days after he was filmed handing over money for cocaine and exotic substance. Mr Flowers issued a statement apologising for doing some “stupid things” claiming, it had been a difficult year. Unfortunately, for lots of loyal workers and stakeholders at the Co-op bank the difficult years will roll on for some time yet. The Treasury enquiry will be led by an independent person appointed by the PRA and the FCA which of course replaced the FSA (which allowed the Flowers appointment in the first place). How the process of “Regulatory Scrabble” moves forward. The enquiry should ask what system considered Bob Diamond so unacceptable as a career banker, yet allowed Flowers to flourish when clearly out of his depth both managerially and professionally. Answers on a PRA, FCA postcard please. Borrowing Back to the economics, more good news for the Chancellor this week as the borrowing figures fell to £8.0 billion from £8.5 billion in October. The underlying data is much stronger than top line figures suggest. Expenditure year to date is up by just 2% but revenues have increased by almost 8%. Income tax and VAT revenues are increasing by over 5% as the recovery gathers momentum. Total borrowing at £115 billion last year will fall towards £100 billion in the current year. CBI and the March of the Makers The CBI survey reported a strong rise in output in the manufacturing sector in the latest survey data released this week. Growth in the manufacturing sector was the strongest for 18 years. Both the size of order books and the pace of output were the highest recorded since 1995. In other news, the SMMT reported a 17% increase in car manufacturing for the month of October. Output for domestic sales increased by over 50%. Don’t get too excited, year to date output growth is up by just over 5%. So what does this all mean? We expect a strong rally in manufacturing output in the final quarter of the year around 2.5% continuing into 2014. Borrowing figures for the year will be much better than expected. The median forecast of the HM Treasury panel is now just £100 billion for the current financial year, falling below £90 billion next year. Growth up, unemployment down, inflation down, borrowing down, only the trade figures will continue to disappoint the coalition platform as the election looms. What happened to sterling? The pound closed up at £1.6215 from £1.6113. Against the Euro, Sterling closed at €1.1966 from €1.1940. The dollar moved up against the yen closing at ¥101.3 from ¥100.1 and closing at 1.3555 from 1.3494 against the Euro. Oil Price Brent Crude closed at $111.05 from $108.50. The average price in November last year was almost $110. We expect Brent Crude to average $110 in the month, with no material inflationary impact. Markets, US pushed higher - The Dow closed at 16,065 up from 15,962. The FTSE closed at 6,674 from 6,693. 7,000 FTSE still the call before Christmas. UK Ten year gilt yields closed at 2.79 from 2.75 US Treasury yields closed at 2.74 from 2.70. Yields will test the 3% level over the coming months. Gold closed at $1,244 from $1,288. The bulls may have it may just have to wait for now. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow and watch out for news of our Monthly Markets updates coming in the New Year. John Join the mailing list for The Saturday Economist or please forward to a colleague or friend. UK Economics news and analysis : no politics, no dogma, no polemics, just facts. © 2013 The Saturday Economist. John Ashcroft and Company, Dimensions of Strategy. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice. It's just for fun, what's not to like! Dr John Ashcroft is The Saturday Economist.

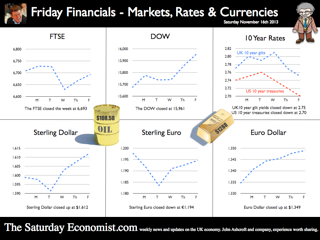

Economics news – you don’t have to be an optimist to see the glass is half full .. Yes it's the Inflation Report “You don’t have to be an optimist to see the glass is half full”, the opening remarks from Governor Carney’s Inflation Report presentation this week. The Governor went on to say, “the glass is half full and it will be filled”. A clear reference the recovery will be allowed to gain momentum before the Bank of England and the MPC will intervene “to take away the punch bowl” and begin the rise in base rates. The MPC are sticking with forward guidance. Rate rises will not even be considered until the level of unemployment hits 7% or even lower. [Subject to caveats on inflation expectations and market stability]. When will this be? In August the Bank assumed this would be in 2016 at the earliest. On Wednesday, the Governor admitted there was a 40% chance this could be by the end of 2014 with a 60% chance it would be by the end of 2015. Such has been the strength of the economics data over the last three months. Our own models assume the knock out unemployment rate will be hit by the third quarter of 2015. Thereafter rates may rise by around 50 basis points in short time. For the moment, the MPC are on a learning journey. The path of productivity, earnings, job creation and unemployment so unclear, we are all embarking on a “learning journey” suggested the governor. The £5m recently spent on the Bank of England model, of little value in the new world it would appear. Charlie Bean appeared most discomfited by the trip. Economics from Cambridge, a PhD from MIT and teaching at Stanford and LSE in the knowledge pack. One could be forgiven the reluctance to take the Mark Carney refresher course. But then why not? Having seriously failed to understand the impact of low rates on investment and depreciation on the trade balance, it is time to denounce the omniscient stance of the Oxbridge collective. Yes send them back to school. Martin Weale was indeed sent back to school this week. The MPC member was delivering a speech on the role of monetary policy and forward guidance to A-level students in London. “To cut a long story short, our job is to ensure that people buy coats when they need them”. Excellent. I am sure that cleared things up. Martin once worked in a shop apparently. Yes the black cloud gang disbanded, it’s back to school for all. Fill up your glasses, the punch bowl is on the table, the Carney Credit card is behind the bar. Inflation Good news for the Governor, inflation fell in October CPI to 2.2% from 2.7% in the prior month. Education hikes last year fell out of the index as we expected but the fall in transport costs pushed the index even lower. 2.4% CPI inflation was our call and still seems to be a reasonable target by the end of the year. Manufacturing prices suggest there is little cost pressure in the economy but retail energy prices are moving significantly higher. Retail Sales Retail sales figures in October were slightly disappointing, an increase of 1.8% in volume and 2.5% in value, slightly down on the averages in Q3. The demise of Barratts Shoes and Blockbuster a reminder, conditions remain tough on the high street as household real incomes remain under pressure. Internationally Janet Yellen, the new head at the Fed is still worried about the strength of the US recovery. Tapering may be postponed still later into the New Year. Growth in France and Japan in the third quarter a further warning the world recovery still requires accommodation. QE tapering US style is not the answer. Buying treasuries and Mortgage Backed Securities to support asset prices makes no sense. Blend a NASDAQ tracker fund into the purchase mix would follow the logic and demonstrate the folly. What happened to sterling? Sterling closed at £1.6113 from £1.6018. Against the Euro, Sterling closed at €1.1940 from €1.1982. The dollar moved up against the yen closing at ¥100.1 from ¥99.1 and closing at 1.3494 from 1.3368 against the Euro. Oil Price Brent Crude closed at $108.50 from $105.12. The average price in November last year was almost $110. We expect Brent Crude to average $110 in the month, with no material inflationary impact. Markets, pushed higher - The Dow closed at 15,962 up from 15,762. The FTSE closed at 6,693 from 6,708. UK Ten year gilt yields closed at 2.75 from 2.77 US Treasury yields closed at 2.70 from 2.75. Yields will test the 3% level over the coming months. Gold closed at $1,288 from $1,284. The bulls may have it may just have to wait for now. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow and watch out for news of our Friday Financials Feature with Monthly Markets updates coming soon. John Join the mailing list for The Saturday Economist or please forward to a colleague or friend. UK Economics news and analysis : no politics, no dogma, no polemics, just facts. © 2013 The Saturday Economist. John Ashcroft and Company, Dimensions of Strategy. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice. It's just for fun, what's not to like! Dr John Ashcroft is The Saturday Economist.

Economics news – import drive and the march of the makers ...

Import Drive ... “Sales of European cars drive trade gap wider” is the headline in the Times today as Britons “flocked” to buy cars built on the continent. The trade figures released this week, reveal the September deficit (trade in goods) increased to £9.8 billion from £9.6 billion last month. The trade deficit with the EU reached a record £6.0 billion as imports increased by £0.4 billion to £18.6 billion. “Half of the increase is attributed to cars”, according to the ONS, hence the slightly unbalanced headline from the Times. In reality, Britons have been flocking to the showrooms since the start of the year. Car sales are up by 10% this year. The deficit was offset as usual by a trade in services surplus of £6.5 billion. This is a familiar pattern which should come as no surprise to readers of The Saturday Economist. The trade deficit will deteriorate further especially if the UK continues to grow at a faster rate than major trading partners in the EU and USA. We are forecasting an overall trade deficit this year of £110 billion offset by a service sector surplus of almost £80 billion. The residual overall deficit easily financed. The September figures are confirmation of the trends within our well established trade model. Depreciation damages UK trade in goods performance. Imports do not react significantly to price changes. There will be no rebalancing of the economy. March of the makers picks up pace ... Did the march of the makers pick up the pace in September? Not really. According to the latest figures from the ONS. Manufacturing output increased in the month by just 0.8%. Output for the quarter was flat as signaled in the Markit/CIPS PMI® survey data last week. Nevertheless we still expect manufacturing growth of almost 2.5% in the final quarter of the year. Last year was such a dismal quarter, even the stumbling marchers will make progress. Watch out for the headlines heralding the rebalancing over the next few months and tie me to a chair. Other survey news ... The service sector continues to drive growth in the economy according to the Markit/CIPS UK Services PMI® for October. The headline Business Activity Index reached a level of 62.5 in October. “The UK service sector maintained its recent run of strong growth during October, with activity expanding at the fastest pace since May 1997 as levels of incoming new business rose at a survey record rate”. The construction rally also continues according to the Markit/CIPS UK Construction PMI® index. The sharp rebound in UK construction output continued in October. The lead index posted 59.4, up from 58.9 in September, above the 50.0 no-change threshold for the sixth consecutive month. So what does this all mean? The economy is recovering and growing at a much faster rate into the final quarter. The pick up in manufacturing output will add to the growth in services and construction. Higher growth, more jobs, lower borrowing, inflation falling, investment will pick up in the second half of next year, it’s all looking pretty good for the Chancellor. Just the trade figures will continue to disappoint. We now think base rates are now more likely to rise by around 50 basis points in 2015. Higher growth will result in unemployment hitting the 7% hurdle rate in the third quarter of 2015, several months after the election. What happened to sterling? The Euro rate cut weakened the hybrid and Sterling strengthened as a result. The pound closed at £1.6018 from £1.5912. Against the Euro, Sterling closed at €1.1982 from €1.1814. The dollar moved up against the yen closing at ¥99.1from ¥98.7 and closing at 1.3368 from 1.3484 against the Euro. Oil Price Brent Crude closed at $105.12 from $105.91. The average price in November last year was almost $110. We expect Brent Crude to average $110 in the month, with no material inflationary impact. Markets, pushed higher - The Dow closed at 15,762 up from 15,616. The FTSE closed at 6,708 from 6,721. The rally continues with a stronger Santa rally in prospect over the next five weeks. UK Ten year gilt yields closed at 2.77 from 2.66 US Treasury yields closed at 2.75 from 2.62. Yields will test the 3% level over the coming months. Gold closed at $1,284 from $1,312. The bulls may have it may just have to wait for now. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow and watch out for news of our Friday Financials Feature with Monthly Markets updates coming soon. John Join the mailing list for The Saturday Economist or please forward to a colleague or friend. UK Economics news and analysis : no politics, no dogma, no polemics, just facts. © 2013 The Saturday Economist. John Ashcroft and Company, Dimensions of Strategy. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice. It's just for fun, what's not to like! Dr John Ashcroft is The Saturday Economist.  Housing Market and Leisure Sector continue to lead recovery ...

Nationwide House Prices House prices increased at a rate of almost 6% in October according to the Nationwide House Price Index. Access to finance, a result of FLS and H2B have improved the willingness of buyers to step into the market. The housing market is up, up and away as our October review of the UK Housing market confirms. Is there a boom in prospect? Robert Gardner, Nationwide's Chief Economist, points out that “while house price growth has picked up - prices remain 7% below their 2007 peak.” Houses are generally affordable - ‘typical mortgage servicing costs remain modest by historic standards thanks to the ultra-low level of interest rates. A typical mortgage payment for a first time buyer is currently equal to around 29% of take home pay, in line with the long term average.” Well it won’t take long for the price lag to be wiped out, even on the Nationwide index. The “real cost of borrowing” is negative - borrowing rates are lower than asset price rises. The essential conditions for market expansion. We expect transactions to increase above one million this year, still well below the peak of 2007. No boom in prospect but a healthy recovery is in train, the house market is up, up and away on a sustainable growth path. Service Sector Growth The service sector continues to provide the back bone of growth in the economy, with growth accelerating to over 2% for the year as a whole. The leisure sector is now the fastest growing sector of the UK economy. Distribution, hotels and leisure have expanded at a rate of 4% in the year. Check out our Service Sector Update for November. Six slides to explain just what is happening in the UK economy. Manufacturing Not the march of the makers, that’s for sure. The latest Markit/CIPS UK Manufacturing PMI® survey was released on Friday. The index slipped to 56.0 in October, down from a revised reading of 56.3 in September. “The UK manufacturing sector continued a strong third quarter performance into the final quarter of the year according to the summary”. Yet manufacturing growth in the third quarter was pretty flat. Nevertheless we still expect growth of over 2% in the final quarter of the year (in manufacturing). Last year was such a dismal quarter, even the stumbling marchers can make progress. So what does this all mean? The economy is recovering and growing at a much faster rate into the final quarter. We still think base rates are now more likely to rise by around 50 basis points in 2015 rather than 2016. We still say this, despite the decision by the Fed this week to hold rates and continue with QE. Growth in the US is weak, inflation is below target and the housing market is confusing analysts. We expect tapering will be back on the agenda in the New Year as we migrate to Planet Janet. What happened to sterling? It was all about the dollar this week. Sterling slipped against the dollar but moved up against the Euro. The pound closed at £1.5912 from £1.6166. Against the Euro, Sterling closed at €1.1814 from €1.1713. The dollar moved up against the yen closing at ¥98.7 from ¥97.4, closing at 1.3484 from 1.3803 against the Euro. Oil Price Brent Crude closed at $105.91 from $106.93. The average price in November last year was almost $110. We expect Brent Crude to average $110 - $115 in the month, with no material inflationary impact. Markets, pushed higher - The Dow closed at 15,616 up from 15,570. The FTSE closed at 6,7351 from 6,721. The rally continues. UK Ten year gilt yields closed at 2.66 from 2.63 US Treasury yields closed at 2.62 from 2.51. Gold closed at $1,312 from $1,352. The bulls may have it but are pegged and penned for the moment. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow and watch out for news of our Friday Financials Feature with Monthly Markets updates coming soon. Join the mailing list for The Saturday Economist or forward to a friend UK Economics news and analysis : no politics, no dogma, no polemics, just facts. John © 2013 The Saturday Economist, #TheSaturdayEconomist, by John Ashcroft and Company, Dimensions of Strategy and The Apple Case Study. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice.  On the road to prosperity

Chancellor Osborne greeted the GDP figures this week with the confident claim we are on the road to prosperity. “Britain’s hard work is paying off, we see that in the economic numbers today”. Indeed we do. Growth in the third quarter increased by 1.6% year on year, exactly as we had expected. Service sector growth continues to underpin the recovery, increasing by 1.9% with particularly strong growth in the distribution, hotels and leisure sector (3.8%). Construction output, boosted by developments in the housing market, increased by almost 5%. Manufacturing output was flat in Q3 up by just 0.1%. Of itself this is a measure of recovery. Output (goods) fell by almost 3% in the first quarter of the year. We expect the recovery in manufacturing to continue with strong growth of over 2% in the final quarter of the year. Our forecast for growth in the year as a whole is unchanged at 1.5%. We expect the economy to be running at trend rate (around 2.5%) in the final quarter. We are on the road to recovery, with prosperity for some, but not all, as growth will continue at 2.5% into 2014. Open for Business Open for business was the theme of a Mark Carney speech this week. The Governor of the Bank of England is shaking up the Bank of England significantly. Last week, Spencer Dale Chief Economist was on Twitter, in an online Agony Aunt economics session. This week, the Governor hired McKinsey and Deloitte to review the central bank's resources and identify cost savings. There will be blood, sweat and tears in Threadneedle Street, as the Old Lady sheds a few layers. The UK is at the heart of a renewed financial globalisation the headline of the Governors speech to celebrate the 125th anniversary of the Financial Times in London. The UK has a strong financial services sector which is to be sustained and developed. [Don’t kill the Golden Goose just because it bit the postman? is the message, if not the exact central bank wording on the subject.] To help the process, the Bank of England is open for business in supporting the banking sector. Facilities will be made available at lower coupon rates and covering a wider risk profile. “The Bank of England today is the friend of resilient banks, continuous markets, and good collateral”. Hurray! Now we have a sensible grasp on economics strategy from the Chancellor and a central banker who talks to the bankers. Whatever next? Borrowing Figures Well lower borrowing figures for one thing. This week, the ONS released the PSNBR figures for the month of September. In September 2013, public sector net borrowing excluding temporary effects of financial interventions (PSNB ex) was £11.1 billion. This was £1.0 billion lower than in September 2012, when it was £12.1 billion. There is more good news to come. Public Sector borrowing is set to fall to £104.5 billion in the current financial year compared to £115 billion in 2012/13. Given the acceleration of growth in the economy into the second half of the year, we believe borrowing could possibly fall below the £100 billion threshold for the year as a whole and below £90 billion in the following year. Good news for the Chancellor as tax receipts including VAT, capital gains and income tax increased by almost 5% in the first six months of the year. Spending on the other hand was up by just 2.4%. Public sector debt was £1.2 trillion at the end of September, equal to 76% of GDP. Of itself a prosperity challenge for the grandchildren. So what does this all mean? The economy is recovering and growing at a much faster rate into the final quarter. Base rates are now more likely to rise by around 50 basis points in 2015 rather than 2016. A short rate rise by the end of 2014 still has low odds given the prevarications in the USA. What happened to sterling? Sterling steadied against the dollar and moved down against the Euro. The pound closed at £1.6166 from £1.6174. Against the Euro, Sterling closed at €1.1713 from €1.1816. The dollar moved down against the yen closing at ¥97.4 from ¥97.7, closing at 1.3803 from 1.3682 against the Euro. Oil Price Brent Crude closed at $106.93 from $109.94. The average price in October last year was almost $112. We expect oil to average less than $110 in the month, with no real inflationary impact. Markets, pushed higher - The Dow closed at 15,570 up from 15,399. The FTSE closed at 6,721 from 6,623. The US debt deal is done. The rally is on. UK Ten year gilt yields closed at 2.63 from 2.72, US Treasury yields closed at 2.51 from 2.58. Gold closed at $1,352 from $1,313. The bulls have it, at least for last week. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow and watch out for news of our Friday Financials Feature with Monthly Markets updates coming soon. Join the mailing list for The Saturday Economist or forward to a friend UK Economics news and analysis : no politics, no dogma, no polemics, just facts. John © 2013 The Saturday Economist, #TheSaturdayEconomist, by John Ashcroft and Company, Dimensions of Strategy and The Apple Case Study. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice.  Economics news – news from Washington and Beijing ...

Washington Good news from across the Pond, a Washington truce has been achieved. The US government has returned to work, Yosemite National Park is open, international creditors will be paid. The debt crisis is over. A twenty week truce has been secured. Markets rallied, the dollar slipped, Google shares breached the $1,000 level and the S&P 500 hit a new high. What more could we ask? Beijing In China, growth continued at 7.8% into the third quarter up from 7.5% in the second. For those fearing a hard landing, crash landing, soft landing, end of the world scenario, it is time to stop shorting the markets and buy in, the world is not coming to an end any time soon. London - Mortgages In the UK, mortgage lending increased by 32% in the third quarter compared to Q3 last year. FLS and Help to Buy are boosting the market. We expect house prices to rise by 5% this year and almost 8% next year before a normalized escalation returns. Prices are beginning to rise across the UK. Yes Prices will move across the UK, like a tidal wave across the flood plain. Check out The Saturday Economist Housing Market Review for more information. Inflation Tuesday, the ONS released the latest inflation figures for September. CPI inflation was unchanged at 2.7% as RPI moved down slightly to 3.2% from 3.3%. We expect a further fall in CPI inflation around 30 basis points next month, as education fees drop out of the data series. Thereafter prices will be pretty sticky around 2.5%. Energy costs are set to rise and service sector inflation at 3.4% up from 3.0% last month will create problems for policy makers. As we have long pointed out, service sector inflation has averaged 3.7% for the last twenty years. Manufacturing prices Manufacturing Prices, on the other hand, have averaged around 1% over the same period, boosted by falls in clothing and footwear specifically. The immediate outlook for manufacturing prices is pretty benign, Output prices increased by just 1.2% in September and input costs increased by 1.1%, down from 5% in July. Retail sales Retail sales were also released this week. Retail sales volumes were up by 2.2% in September and by 2.4% in the third quarter. Sales values increased by almost 4% in the three months boosted by on line sales and department store sales. Is the housing market stimulating footfall? Quite probably. We expect the volume of housing transactions to increase significantly this year, boosting sales of carpets, furniture durables and DIY goods in the process. Employment The employment figures were also released this week. The claimant count fell by over 40,000 in September to a rate of 4% compared to 4.2% last month. The wider FLS count fell in the three months to August, to 2.87 million, a rate of 7.7% from 7.8% last month. Lagging as it does, the broader unemployment rate could fall to around 7.5% by the end of the year. The Bank of England “knock out rate” under forward guidance at 7% could be in sight by the end of 2014. So what of base rates? Interesting Spencer Dale the Bank of England’s chief economist was on Twitter this week in a hashtag #AskBoE “open hour” adventure. The telling tweet - a rate rise in 2014 was unlikely. Just as unlikely as a rate rise in 2016 no doubt. The markets expect a move in 2015 but will it wait until after polling day? We will have to ask next time the bank is online, perhaps using Facetime or Skype? What would Governor King have made of it all! So what does this all mean? The economy is recovering and growing at a much faster rate into the final quarter. The first estimate of GDP in Q3 will be released next week. We expect growth year on year to be over 1.5% rising to trend rate in the final quarter of the year. Inflation is falling, employment is rising, even the debt figures due next week will look much better. Energy costs may provide a problem for households but “wear a jumper”, the ministerial advice could keep bills down and boost retail sales in the process. What happened to sterling? Sterling moved up against the dollar and against the Euro as the dollar slipped. The pound closed at £1.6174 from $1.5954. Against the Euro, Sterling closed at €1.1816 from €1.1772. The dollar moved down against the yen closing at ¥97.7 from ¥98.5 and closing at 1.3682 against the Euro. Oil Price Brent Crude closed at $109.94 from $111.28. The average price in October last year was almost $112. We expect oil to average less than $112 in the month, with no inflationary impact. Markets, pushed higher - The Dow closed at 15,399 up from 15,237. The FTSE closed at 6,623 from 6,487. The US debt deal is done. The rally is on. UK Ten year gilt yields closed at 2.72 from 2.74, US Treasury yields closed at 2.58 from 2.69. Gold closed at $1,313 from $1,270. The bulls have it, at least for the week. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow. Join the mailing list for The Saturday Economist or please forward to a colleague or friend. UK Economics news and analysis : no politics, no dogma, no polemics, just facts. John © 2013 The Saturday Economist. John Ashcroft and Company, Dimensions of Strategy. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice. It's just for fun, what's not to like! Dr John Ashcroft is The Saturday Economist If you do not wish to receive any further Saturday Economist updates, please unsubscribe using the buttons below. If you enjoy the content, why not forward to colleague or friend.  Economics news – Building recovery one brick at time ..

Construction data Good news this week from the construction sector. Output in August was up by 4% compared to August last year. New work increased by almost 6% driven by developments in the housing market. FLS and Help to Buy are stimulating new mortgage activity on a really significant scale. The Council of Mortgage Lenders announced home-owner house purchase lending was up by 15% on August last year. First-time buyers took out 27,100 loans in August, an increase of 33% compared to August 2012. The house market is on the move. We expect the surge in housing activity to continue into the final quarter of the year and into 2014. Do we really need “Help to Buy Phase 2” probably not. No need to pay for a landslide, the economic recovery secured. We have increased our forecasts for GDP growth this year to 1.5% increasing to 2.5% next year. NIESR monthly GDP data Our estimates are in line with the NIESR monthly GDP tracker for September, released this week. The (NIESR) GDP rate of growth in the third quarter was 1.6% year on year. We expect the rate of growth to accelerate further into the final quarter towards trend rate of 2.4%, driven by a steady recovery in the service sector and a big push in construction output. Monetary Policy No surprise this week the MPC voted to keep interest rates and QE on hold. Forward Guidance is the new mantra. UK base rates will not rise until the U rate falls to 7%, assuming no shocks to the monetary system and the inflation outlook. In the USA, the Fed continued with the monthly asset purchases of $85 billion. What is it about the USA? The Fed might as well commit dollars to a NASDAQ tracker fund to sustain confidence in the markets. “Tapering will not begin until the DOW hits 17,000 could be the new forward guidance. Janet Yellen is to replace an exhausted Bernanke. Such a dove, they should “paint her white and give her wings”, the markets will love Planet Janet orbiting, as it will, around Planet ZIRP. So what of the UK recovery? The trade figures and manufacturing data were also released this week. Remember, "the march of the makers, rebuilding the workshop of the world, rebalancing the UK economy away from domestic consumption with an improvement in net trade"? Well forget that. The professor (Milton Keynes) invested in a sandwich board and spent his summer holidays in Cornwall this year. Stationed at Land’s End, facing Western traffic, the sign read “sail on - the earth is not flat”. “We get the message” shouted a wise cracking grockle. The professor turned to reveal the message on the other side, “Exports will not lead a UK recovery”, “yeah but how long did it take”, replied the perspicacious prof. Trade Data And so it proved with the trade data this month. The trade in goods deficit was £9.6 billion in August. We expect a deficit of £29 billion in the quarter compared to £26 billion last year. Our forecast for the year, is now at the top end for the year as a whole around £110 billion. The UK recovery will exacerbate the deficit. Monthly data can be erratic but fifty year trends provide a certain guide. The UK cannot grow faster than Europe and the USA without a significant deterioration in net trade in goods. Is this such a problem? Not really. The surplus on services will mitigate the deficit to around £30 billion. At 2% of GDP this is neither a threat to sterling nor a constraint to growth. Manufacturing The march of the makers skipped a drum beat in August as output fell by -0.2% compared to August last year. Consumer goods output fell by just over 2% as capital goods growth slowed to a similar level. We expect a better performance in September and in the final quarter of the year. Housing new build and a higher level of transactions will stimulate direct related construction output, (bricks & mortar). Housing related spending on products including furniture and carpets will also stimulate growth. So what does this all mean? The economy is recovering and growing at a much faster rate into the final quarter. Will US debt intransigence derail recovery? We assume not. If you lived through the Cuban missile crisis and the era of an international nuclear strategy underwritten by the concept of Mutually Assured Destruction, (They call it MAD), You assume sooner or later, the Republican ships will turn around and avoid the disaster that could unfold. Failing that, the President can always mint a few Trillion Dollar Platinum coins, develop section four of the fourteenth amendment or invoke the 1861 Feed and Forage Act. Union soldiers were allowed to “eat your crops, kill your chickens and water their horses”. The Act ensured, sooner or later, Congress would enact the necessary appropriation. The troops had to eat even though the deficit had not been approved. And so it is with debt markets, “let them eat noodles” is no message to send to international creditors. What happened to sterling? Sterling moved down against the dollar and against the Euro. The pound closed at £1.5954 from $1.6012. Against the Euro, Sterling closed at €1.1772 from €1.1816. The dollar moved up against the yen closing at ¥98.5 from ¥97.4.The dollar euro cross rate at 1.3542 was largely unchanged from 1.3556 Oil Price Brent Crude closed at $111.28 from $109.46. The average price in October last year was almost $112. We expect oil to average $112 in the month, with no real inflationary impact. Markets, rallied - The Dow closed at 15,237 from 15,073. The FTSE closed at 6,487 from 6,454. The markets sense a deal on the deficit is in sight. UK Ten year gilt yields closed at 2.74 from 2.75, US Treasury yields closed at 2.69 from 2.64. Gold closed at $1,270 from $1,310. The bulls have it or do they? Gold will trade sideways for some time yet. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow. Join the mailing list for The Saturday Economist or please forward to a colleague or friend. UK Economics news and analysis : no politics, no dogma, no polemics, just facts. John © 2013 The Saturday Economist. By John Ashcroft and Company, Dimensions of Strategy. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice. It's just for fun, what's not to like! Dr John Ashcroft is The Saturday Economist. |

The Saturday EconomistAuthorJohn Ashcroft publishes the Saturday Economist. Join the mailing list for updates on the UK and World Economy. Archives

April 2024

Categories

All

|

| The Saturday Economist |

RSS Feed

RSS Feed

The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The presentation should not be construed as the giving of investment advice.

|

The Saturday Economist, weekly updates on the UK economy.

Sign Up Now! Stay Up To Date! | Privacy Policy | Terms and Conditions | |