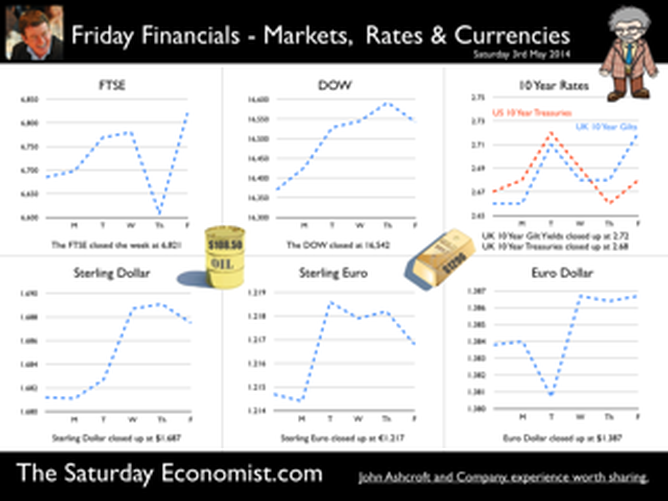

GDP Figures Q1 … UK growth in the first quarter of 2014 was an impressive 3.1% year on year with significant growth in construction, manufacturing and the service sector. [According to the preliminary estimate from the Office for National Statistics released this week.] Construction growth increased by 5.1% in the quarter and manufacturing output increased by 3.5%. Service sector output was up by 2.9% with continued strong growth in distribution, hotels, and leisure (4.9%). The business and financial services sector increased by 3.6%. The outturn is more or less in line with our estimates in the Quarterly Economics Outlook released in March. Following the latest data, we have lowered our forecasts for growth in the construction sector for the year as a whole and increased our estimate of growth in manufacturing. The overall GDP position remains unchanged. We still forecast GDP growth of 2.9% in 2014 and 2.8% in 2015. Growth continues into Q2 … The good news continued this week, with the latest Markit/CIPS PMI® survey data on manufacturing and construction. In April the UK manufacturing sector maintained a robust start to the year. At 57.3, the seasonally adjusted index rose to a five-month high and registered one of the best readings over the past three years. Construction output continued to increase in April, albeit at the slowest pace for six months. The index recording of 60.2 is down from the peaks at the turn of the year but still ahead of the long run average of 54.3. Residential construction was the best performing area of activity. The rate of expansion in April remained one of the fastest seen over the past ten years … just as well! House Prices - increase into double figures … House prices increased by over 10% according to the latest figures from Nationwide. Robert Gardner, Nationwide's Chief Economist said: “After several months of moderation, the pace of house price growth picked up in April. Annual house price growth reached double digits for the first time in four years, with the price of a typical home 10.9% higher than April 2013. Still much to be done in construction however, “The upturn in construction of new homes continues to lag far behind the upturn in demand, with the number of new homes being built in England still around 40% below pre crisis levels.” Sir Jon Cunliffe, Deputy Governor of the Bank of England, expressed some concerns about the housing market in a speech in London this week. “The question for the Financial Policy Committee, is whether the sustained momentum in the housing market will lead to unsustainable growth in household indebtedness, undermining the resilience of the financial system. The growing momentum in the housing market is now the brightest light on the dashboard of warning lights.” You have been warned! Growth in the USA ... In the USA, growth in the first quarter was up by 2.3% year on year (0.1% quarter on quarter). The relatively disappointing number was attributed to a severe winter and much bad, wet weather. The Federal reserve derived some consolation from the strength of the jobs numbers released this week. In April, the number of non farm payroll jobs increased by almost 290,000, the unemployment rate fell to 6.3% and revisions to the employment numbers over the past three months confirmed the strength of the US recovery. Jobs growth over the last three months has averaged almost 240,000. With evidence of a strong performance in employment and household spending, the Federal reserve announced a further reduction in tapering with a reduction in asset purchases to $45 billion per month. Tapering is on track to completion by the September / October this year. Interest rate rises will then ensue possibly within six months. With inflation below target, wages rising by just 1.9% and almost 10 million Americans unemployed, the FOMC will be in no rush to act. So what happened to sterling this week? The pound closed up against the dollar at $1.687 from $1.681 and up against the Euro slightly at 1.217 (1.215). The dollar closed at 1.387 from 1.382 against the euro and at 102.23 (102.15) against the Yen. Oil Price Brent Crude closed at $108.50 from $109.54. The average price in May last year was $102.3. Markets, the Dow closed up at 16,542 from 16,370 and the FTSE also closed up at 6,821 from 6,685. The markets are making the move, the push before the rush, may see the FTSE hit 7000 before the summer sell off! UK Ten year gilt yields closed at 2.72 (2.66) and US Treasury yields closed at 2.72 from 2.67. Gold moved down $1,296 from $1,301. That’s all for this week. Join the mailing list for The Saturday Economist or forward to a friend. John © 2014 The Saturday Economist by John Ashcroft and Company. Experience worth sharing. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice.

0 Comments

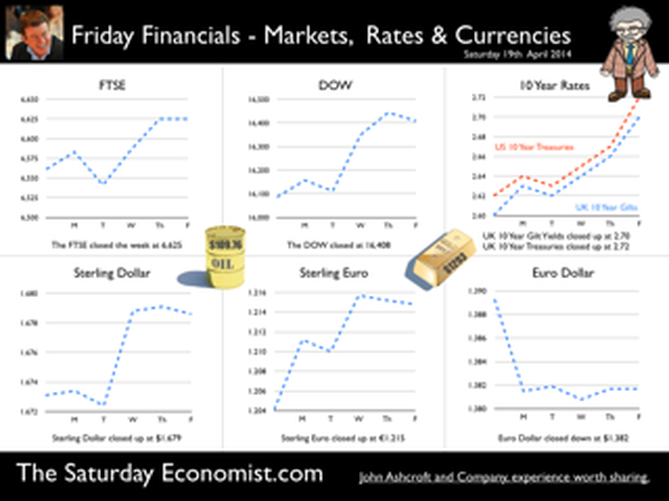

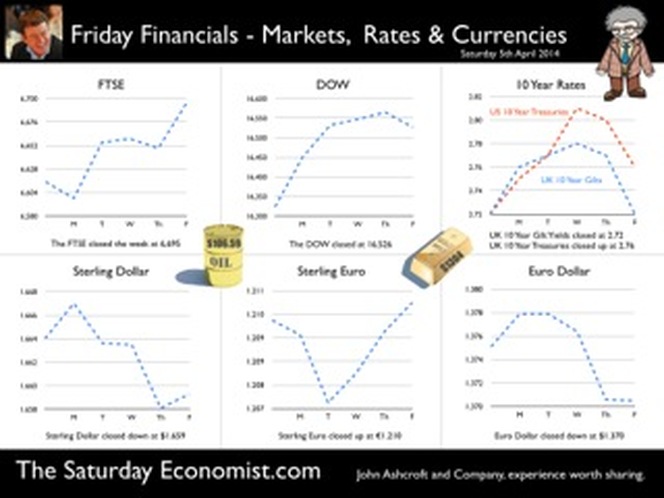

Janet Yellen was speaking at the Economic Club of New York this week. Three big questions continue to dominate policy formulation at the Federal Reserve. Unemployment, inflation and factors which may push the recovery off track. Actually, that’s more than three but … According to the Fed forecasts, US unemployment is set to fall to around 5.5% by the end of 2016 and inflation will hover just below 2%. “The economy would be approaching maximum employment and price stability for the first time in nearly a decade”. That's NICE! And what of interest rates? “Economic conditions, may for some time warrant keeping short term interest rates below levels the Committee views as likely to prove normal in the longer run”. The markets reacted well. The Dow moved up and the dollar moved down. Sterling moved to $1.679. In March, the Fed chair had given a clear indication that rates would start to rise in the first quarter of 2015. Less than a month later, there was no such clarity. Rates will be on hold until the recovery is well established. As long as it takes. Unemployment rate, the measure of momentum that really matters, to the doves at the Fed. Exogenous Shocks Nowhere in the speech did the “Capsid Bug” feature. According to a report in The Times today, black pod disease and capsid bug infestations are ravaging cocoa crops in West Africa. This shock to supply plus the surging demand from Chinese Chocaholics is causing a cocoa pop. Cocoa beans have jumped in price from $2,680 per tonne in January to over $3,000 per tonne in March. There could be a 115,000 tonne shortfall in supply this year. By next Easter, we may well be eating smaller eggs which cost much more. So much for the threat of world deflation! Does this matter? Well yes. The collapse of the Peruvian anchovy crop in 1972/3 was claimed by many to herald the onset of the hyper inflationary episode of the seventies. OK, the Russian grain famine, the onset of OPEC and the quadrupling of oil prices assisted considerably. But the message is, exogenous shocks from commodity prices can have a greater impact on domestic inflation. Much greater than the Phillips curve paradigm, much beloved by the FOMC, provides. This is clearly demonstrated in the UK economics data released this week. Inflation is falling, employment is rising. World prices mitigated by the appreciation of Sterling are marking the price changes. UK Inflation Inflation CPI basis slowed to 1.6% in March from 1.7% in the prior month. Goods inflation fell to 1.0% and service sector inflation fell to 2.3% (2.4%). Oil related transport costs were dominant in the slow down. Manufacturing output prices increased by just 0.5% as input costs actually fell by 6.5%. The fall in crude oil prices, imported metals, parts and equipment largely explained the fall. Sterling appreciation assisted the process. Sterling averaged $1.66 in March this year compared to $1.51 last year. A 10% appreciation assisting the “deflationary process” significantly. [Oil prices Brent crude basis averaged $108 approximately in both months]. So what of employment? Unemployment figures - Jobcentres will be closing by the end of 2016 Unemployment fell to 6.9% in the three months to February to a level of 2.24 million. This is below the level originally outlined in the Bank of England Forward Guidance in August last year. 7.0% the level at which the Bank would begin to consider an increase in base rates. The claimant count fell by 30,000 to a level of 1.142 million. Over the last three months, the count has fallen by 100,000 and almost 400,000 over the last twelve months. If current rates persist, the labour market will fall to pre recession levels towards the end of the year. By the end of 2016, No one will be left on the list. So this is what they mean by full employment! Jobcentres will have to close! The implications for earnings are evident. Already in February, whole economy earnings increased by 1.9% and wages in manufacturing and construction increased by 3%. We expect a significant acceleration in earnings throughout the year as the labour market tightens considerably. As for base rates, Yellen is signalling the US rates will be kept on hold well into 2015. The Bank of England may well have no such luxury. The MPC will be reluctant to raise rates ahead of the Fed. If this were to happen, despite the inherent structural weakness on trade and the current account, sterling will continue to rise significantly. $1.73 the next target? So what happened to sterling this week? The pound closed at $1.679 from $1.673 and at 1.215 from 1.204 against the Euro. The dollar closed at 1.382 from 1.3389 against the euro and at 102.42 against the Yen. Oil Price Brent Crude closed at $109.76 from $107.70. The average price in April last year was $101.2. The energy kicker to falling prices may well be over. Markets, the Dow closed up at 16,408 from 16,086and the FTSE also closed up at 6,625 from 6,561. UK Ten year gilt yields closed at 2.70 (2.60) and US Treasury yields closed at 2.72 from 2.62. Gold moved lower to $1,293 from $1,318. The pattern is bullish for equities.. That’s all for this week. Join the mailing list for The Saturday Economist or forward to a friend. John © 2014 The Saturday Economist by John Ashcroft and Company. Experience worth sharing. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice.   Car sales soar but so will the trade deficit … Good news of the recovery. Car registrations rose to 465,000 in March, an increase of 18% on last year. The new 2014 plates have been great for the car market. More new cars were registered last month, than at any time in the last ten years according to the Society of Motor Manufacturers and Traders. As Mike Hawes, SMMT Chief Executive explains. “Given the past six years of subdued economic performance across the UK, there is still a substantial margin of pent-up demand, contributing to a strong new and used car market.” Easy finance deals and advanced technologies make new cars cheaper to buy and to run. There has never been a better time to buy a new car. The pent up demand is to be unleashed. Bear in mind, we have over 31 million cars on the road in the UK, of which over one third are over nine years old. Let’s hope the owners don’t all appear in the showroom at once.That would create a traffic jam at the docks. The car market demonstrates clearly the problems with the march of the makers, the rebalancing agenda and the inability of sterling depreciation to remedy the trade balance. We expect car sales to increase to around 2.5 million units in 2014 returning to levels last seen in 2004 and 2005. Production is forecast to increase to 1.6 million units following the increase to 1.5 million last year. A further increase to 1.7 million units, then 1.8 million units is expected by 2016. Good news for manufacturing? Of course. But the majority of production is exported. Export sales may hit 1.3 million units in 2014, rising to 1.5 million by 2016. As a result, imports will have to increase to 2.2 million units in 2014, rising to 2.4 million units by 2016 to satisfy domestic demand. The trade deficit (unit sales) will increase to 0.8 or 0.9 million units. An increase to levels least seen pre recession. The recovery in the UK economy will exacerbate the trade deficit in cars just as it will in many other commodities. Relative rates of economic growth here and particularly in Europe primarily determine the demand for imports and exports. Demand is relatively inelastic with regard to price, particularly with exports. Manufacturers price to market or products form part of international syndication. Sterling has a minor role to play in determining the direction of trade in the international car market. Supply, is output constrained and cannot respond to domestic market growth. In fact 80% of car production is exported and 90% of domestic demand is satisfied by imports. We have warned previously, the UK cannot grow faster than trade partners in Europe or North America without a deterioration in the trade account. The car market is a simple arithmetic of the dilemma. Download the short report Car Market - Driving recovery or driving the deficit to access the underlying data. PMI Markit Surveys This is the week of the PMI Markit survey data with information on the March updates. The recovery continues in services, construction and manufacturing. The manufacturing upturn remains solid, service sector activity remains strong and construction firms report brightest outlook for business activity since January 2007. We have upgraded our forecast for UK growth this year to 2.9% based on the strength of the Manchester Index® and latest GM Chamber of Commerce QES survey data. House Prices, Nationwide reports house prices increasing by 9.5% across the UK, increasing by 18% in London. Prices remain slightly below the peak levels of 2007 except in the capital, were levels are now some 20% above peak. Should we worry about the boom in prices? Perhaps but not just yet. Activity levels are still subdued relative to the pre recession peaks but the recovery in prices will be of concern to policy makers as will the developing trade deficit. In our economics presentations we begin to touch on concerns about the recovery. Deflation is not one of them, house prices may be. The current account deficit certainly is. Especially if the trends in investment income from overseas are maintained. Then we shall see just what will happen to sterling. So what happened to sterling this week? The pound closed at $1.659 from $1.664 and at 1.21 unchanged against the Euro. The dollar closed at 1.370 from 1.375 against the euro and at 103.26 from 102.82against the Yen. Oil Price Brent Crude closed at $106.72 from $108.01. The average price in March last year was $108. Markets, the Dow closed up at 16,526 from 16,323 and the FTSE closed at 6,6956 from 6,615. UK Ten year gilt yields closed at 2.72 (2.72) and US Treasury yields closed at 2.76 from 2.72. Gold moved higher to $1,304 from $1,293. That’s all for this week. Join the mailing list for The Saturday Economist or forward to a friend. John © 2014 The Saturday Economist by John Ashcroft and Company. Experience worth sharing. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice.

Good news in the car market but the higher level of sales will drive the trade deficit higher - no rebalancing on the road ahead. Download the file here.

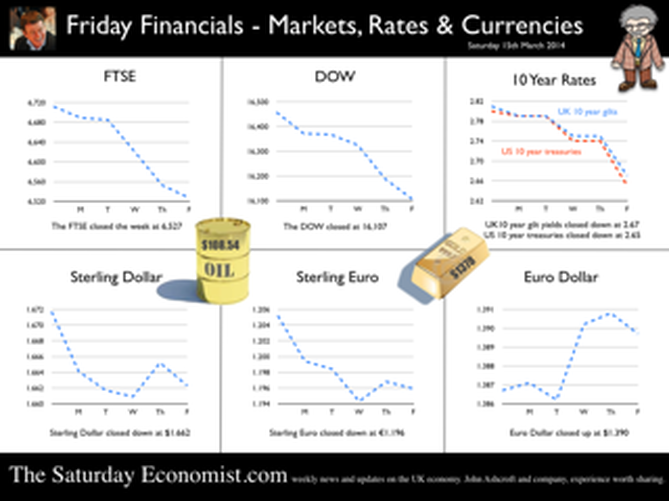

The new 14 plates have been great for the car market. Registrations in March were 465,000, up by 18% on March last year. UK car registration increased by 15% in the first three months of 2014. We forecast total sales of almost 2.5 million this year, returning to levels of sales, last seen in 2004 and 2005. Production is forecast to increase to 1.6 million units following the increase to 1.5 million last year. A further increase to 1.7 million units, then 1.8 million units is expected by 2016. Good news? Of course. But the majority of production is exported. Export sales may hit 1.3 million units in 2014, rising to 1.5 million by 2016. As a result, imports will have to increase to 2.2 million units in 2014, rising to 2.4 million units by 2016. The trade deficit (unit sales) will increase to 0.8 million units, to the levels least seen pre recession. The surge in car sales is a welcome demonstration of UK demand. As Mike Hawes, SMMT Chief Executive explains. “Given the past six years of subdued economic performance across the UK, there is still a substantial margin of pent-up demand that is contributing to a strong new and used car market.” The pent up demand is to be unleashed. Remember we have over 31 million cars on the road in the UK of which over one third are over nine years old. Easy finance deals and advanced technologies make new cars cheaper to buy and to run. There has never been a better time to buy a new car. Let’s hope they don’t all rush at once. That would create a traffic jam at the docks. That’s another reason why we say the trade figures will continue to disappoint, and threaten the recovery, especially if the collapse in investment income continues. Download the short report here.  UK march of the makers … Good news for the march of the makers this week, - manufacturing output increased by 3.3% in January compared to disappointing growth of just 1.9% in the final quarter of 2013. Still some way to go to restore the sector to positive growth. Output remains some 9% below the peak registered in the first quarter of 2008. Output of Investment and capital goods increased by 3.8%, continuing the strong trend since the setback in 2008. We expect manufacturing output to increase by 2.9% for the year as whole and around 2.7% in the following year. Consumer goods output remained weak with further declines in the month. For some sectors of manufacturing, the march of the makers is more like a retreat from Moscow, than a move across the Rhineland. The makers will fail to make a real contribution to the rebalancing agenda. So what of net trade … The trade figures for January were released this week. After the December aberration, a month in which the ONS appears to have lost some £2 billion of imports, the total trade balance returned to normality. A deficit of £2.6 billion compared to £0.7 billion last month. There was a trade shortfall of £9.8 billion on goods, partly offset by an estimated surplus of £7.2 billion on services. For the year as a whole, we expect the trade deficit in goods to increase to £114 billion, offset by a trade in service surplus of £85 billion. The overall trade in goods and services shortfall will be £29 billion. At less than 2% of GDP, the deficit will not pose a threat to the outlook for sterling, assuming investment capital flows recover. The trade deficit will fail to make a real contribution to the rebalancing agenda. And what of Construction … Good news in construction. Output increased by 5.4% in January compared to the same month last year. New work increased by almost 6% in the month, as repair and maintenance budgets also increased by 4.5%. For the year as a whole we expect construction growth of around 6%, with strong growth in housing and commercial property expansion fuelling growth. Prospects for the year … The OECD suggests the UK economy will grow by over 3% in the first half of the year, in line with the strong expectations from the Bank of England “Nowcasting” model, news of which was also released this week. The NIESR GDP tracker for February suggests growth may have slowed to 2.6% in February after strong growth of 3.2% in the prior month. For the year as a whole most forecasters are moving to a 2.7% growth figure. Seems reasonable for now. The recovery appears secure and sustainable. Growth up, unemployment down, inflation down and borrowing heading in the right direction. Just the trade figures will continue to disappoint as we have long pointed out. Charlie Bean on the North East Scene … Charlie Bean was in the North East this week, delivering a speech to the Chamber of Commerce. Further reassurance the MPC will be doing its utmost to ensure that recovery is not nipped in the bud. “When the time does come for us to start raising Bank Rate, we should celebrate that as a welcome sign that the economy is finally well on the road back to normality”. Excellent. Much of the rest of the speech was devoted to investment, productivity and net trade. As the deputy governor points out, the United Kingdom has run a persistent trade deficit of the order of 2-3% of GDP since the beginning of the century. So much for “rebalancing”. On investment, productivity, depreciation and “on shoring”, the speech demonstrates the lack of fundamental understanding of the real economy amongst policy makers at a senior level. We had hoped for better from the new regime. Charlie represents the old guard due to retire in June this year. Of The Treasury Select Committee … The Governor and members of the MPC were in front of the Treasury Select Committee this week. The protocol still eludes the new man. Governor Carney actually winked at Chairman Tyrie at one stage. It is difficult to imagine Governor King, managing a nod let alone a wink. It appears the meetings of the MPC are minuted and recorded. Then for good measure the tapes are destroyed. Lack of good recording equipment formed part of the explanation by the old guard. The solution to invest in better equipment seemed a little too obvious for the Chairman and the new Governor. Expect a rethink! Wink Wink. So what happened to sterling? The pound closed at $1.662 from $1.672 and at 1.196 from 1.205 from against the Euro. The dollar closed at 1.390 from 1.387 against the euro and 101.31 from 103.3 against the Yen. Oil Price Brent Crude closed at $108.34 from $108.86. The average price in March last year was $108. Markets, moved down concerned about China and the Ukraine - The Dow closed at 16,107 from 16,458 and the FTSE closed at 6,527 from 6,712. UK Ten year gilt yields closed at 2.67 from 2.81and US Treasury yields closed at 2.65 from 2.80. Gold loves a crisis, closing up at $1,378 from $1,338. That’s all for this week. No Sunday Times and Croissants tomorrow. All records of the tennis results will be recorded then destroyed. Join the mailing list for The Saturday Economist or forward to a friend. The list is growing as is our research team. John © 2014 The Saturday Economist by John Ashcroft and Company. Experience worth sharing. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice.

UK rates on hold …

No surprise this week - the MPC voted to keep rates on hold and maintain the size of the asset purchase programme at £375 billion. It will be some months yet before rates begin to rise. Our current assumption is that rates will begin to rise in the second quarter of 2015. 40% of respondents in the latest Bank of England/GfK Inflation survey expect rates to rise over the next twelve months. No worries for the future apparently. Once on the rise, over 70% expect rates to be less than 3% in five years time. So much for the madness of crowds. Clearly the general public have a much better grasp of the latest simulations of the “equilibrium real interest rate associated with a neutral monetary policy over the medium term” than is generally assumed. They must have been listening to the speech by David Miles last month. Asked about the current rate of inflation, the median answer was 3.5% down from 4.4% in November. Excellent. So much for the madness and the wisdom of crowds. US Payroll data up … In the USA, better than expected payroll data guarantees the Federal Reserve will continue to taper, with a further reduction this month to $55 billion. Employers added 175,000 more jobs in February. Movement in US futures suggest the markets attach a "higher probability to a US rate rise in the middle of 2015". Fed officials have said they are “comfortable with market expectations of future rate rises”. We think US rate rises could be on the agenda by the end of 2014 or early 2015. The implications for UK rate rises should be evident. Our mantra - watch the USA and add six months - may be a little more compressed in this cycle. UK survey data … This week the February Markit/CIPS UK PMI® surveys were released. The strong upswing in the UK manufacturing sector continued in February. Output and new business continued to rise at above-trend rates. The leading index at 56.9 was up from a revised reading of 56.6 in January. In construction, the pace of expansion continued to rise sharply. The leading index scored 62.6 in February, down from a 77-month high of 64.6 in January. Still a very strong performance. In the service sector, output continues to expand strongly in the month. The headline Business Activity Index recorded 58.2 during February, little changed on January’s 58.3 and indicative of a sharp rise in activity on a monthly basis. Overall, output in construction, manufacturing and services suggest the economy continues to recover across the board at a very strong rate. The latest NIESR GDP tracker suggest growth increased by 3.5% in January. The Bank of England expects growth of over 3.5% in the first quarter. For the year as a whole, the consensus forecast is for growth of 2.7% this year. We await the details of the latest GM Chamber of Commerce survey before raising our estimates of growth this year. The GDP(O) model is signalling growth of 3% for the year as a whole. The survey data is a little more tempered, I suspect. In the UK and the USA, growth is accelerating and the job market is “tightening”. The pay round will become more difficult by the end of the year. Earnings are set to increase significantly as critical unemployment levels are breached by early 2015. Household incomes are set to improve and the recovery in spending will continue. There will be no “rebalancing”, whatever that really means. Growth up, unemployment down, inflation down and borrowing heading in the right direction. Just the trade figures will continue to disappoint. If growth hits 3% this year, disappointment could turn to shock and alarm. Then all forward rate bets will be off. So what happened to sterling? The pound closed at $1.672 from $1.675 and at 1.205 from 1.213 against the Euro. The dollar closed at 1.387 from 1.381 against the euro and 103.3 from 101.7 against the Yen. Oil Price Brent Crude closed at $108.86 from $109.02. The average price in February last year was almost $116 falling to $108 in March. Markets, moved slightly - The Dow closed at 16,458 from 16,367 and the FTSE slipped closing at 6,712 from 6,809. UK Ten year gilt yields closed at 2.81 from 2.72 and US Treasury yields closed at 2.80 from 2.67. Gold lovers worship alone with a close at $1,338. That’s all for this week. No Sunday Times and Croissants tomorrow or for the rest of this year for that matter. We are taking a break in this pre election year. Join the mailing list for The Saturday Economist or forward to a friend. The list is growing as is our research team. John © 2014 The Saturday Economist by John Ashcroft and Company. Experience worth sharing. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice.  Revisions to GDP …

The second estimates of growth in the UK and the USA were released this week. In the US growth of 3.2% in the final quarter of the year, was revised down to a more modest 2.5%. Janet Yellen, head of the Fed is prepared to dismiss recent soft economic data as possible result of the bad cold snap. For the year as a whole, US growth in 2013 was a respectable 1.9%. Most forecasters still expect US growth of 2.8% to 2.9% in 2014. In the UK, the second estimate of GDP was also released this week. Growth in 2013 was revised down to 1.8%. Oh dear, the UK is no longer the fastest growing economy in the developed world. Just as well, the balance of payments strain would have been too much. The outlook for the current year hasn’t changed overall. We still expect growth of 2.5% in the year, with the consensus forecast slightly higher around 2.7%. The right kind of growth? … But is it the right kind of growth? For the purists, probably not. For the pragmatic, what’s not to like? The service sector continued to drive expansion in the economy, with significant growth in the leisure sector along with business and financial services. Distribution, hotels and restaurant trades grew by almost 4% in the year, up by almost 5% in the final quarter. Business and financial services were up by 3% in the last quarter, up by 2.6% for the year as a whole. The service sector accounts for 80% of total output in the economy. The real driver of recovery. Good news in construction … The good news in construction continued with growth up by 4.4% in the last three months of the year. Developments in the housing sector providing foundations for recovery. Assuming we can make the bricks, growth should continue into 2014 with our forecast growth over 6% in the current year. The march of the makers … So what of the march of the makers? Growth in manufacturing output was revised down to less than 2% in the final quarter. This is particularly disappointing, since the prior year figure was a “nothing to beat number”. For the year, manufacturing output actually fell by 0.6%. Output is still almost 10% below the pre recession peak. We have to be realistic when formulating a policy for industry. We expect growth for the manufacturing sector broadly in line with total GDP this year but not much more. So what of rebalancing … Household spending last year was up by 2.5% accounting for over 60% of GDP. There is little evidence of rebalancing in the economy, either in terms of net trade or investment. Investment, accounting for 14% of total spending, actually fell slightly, despite growth of over 8% in the final three months. Was this a trend reversal, end of year? Possibly. We expect investment growth to continue into 2014 as the forward outlook clears and confidence returns to the board room. M & A activity, will assist the figures. Plus, 60% of investment is related to dwellings and commercial property. Investment in plant and machinery, the real capital stock within the economy, accounts for just 20% of total investment. With property resurgent, we expect investment growth of 8% in 2014. And what of base rates? … In the US, Janet Yellen affirmed the Fed commitment to continued tapering. QE could be eliminated by the Fall with a steady reduction of $10 billion per month. That could mean, a US rate rise could be on the agenda by the end of the year. The mantra for the UK remains watch the USA and add six months. The MPC cannot move ahead of the Fed without significant appreciation of sterling. When will UK rates rise? Martin Weale has suggested UK rates will rise in the Spring next year and could rise earlier if productivity fails to improve and inflation ticks up. Ian McCafferty a fellow MPC member suggests the rate rise may be held back because of the strength of sterling and the resultant mitigating impact on inflation. Either way, rates are set to rise, probably in 2015 but possibly after the May election. The banks are beginning to model affordability and pay back with a 5% base rate test. This may prove too severe for some years yet. The MPC would have us believe rates will be held below 2% until late 2017. David Miles in a speech to the Mile End group this week, suggests the “new normal” could include an equilibrium base rate of 2.5% to 3% over the long term. Imagine, we may never see the 4.5% base rate again! So much for 320 years of history, in which we have endured an average base rate of 4.5% to 5%. If only! New normals usually end up as the same old same olds. So what happened to sterling? The pound closed up at $1.675 from $1.664 and at 1.213 from 1.210 against the Euro. The dollar closed at 1.381 from 1.374 against the euro and 101.7 from 102.5 against the Yen. Oil Price Brent Crude closed at $109.02 from $109.67. The average price in February last year was almost $116 falling to $108 in March. Markets, moved slightly - The Dow closed at 16,367 from 16,143 and the FTSE closed at 6,809 from 6,838. UK Ten year gilt yields closed at 2.72 from 2.79 and US Treasury yields closed at 2.67 from 2.75. That’s all for this week. No Sunday Times and Croissants tomorrow or for the rest of this year for that matter. We are taking a break in this pre election year. Join the mailing list for The Saturday Economist or forward to a friend. The list is growing as is our research team. John © 2014 The Saturday Economist by John Ashcroft and Company. Experience worth sharing. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice. |

The Saturday EconomistAuthorJohn Ashcroft publishes the Saturday Economist. Join the mailing list for updates on the UK and World Economy. Archives

April 2024

Categories

All

|

| The Saturday Economist |

RSS Feed

RSS Feed

The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The presentation should not be construed as the giving of investment advice.

|

The Saturday Economist, weekly updates on the UK economy.

Sign Up Now! Stay Up To Date! | Privacy Policy | Terms and Conditions | |