They say inflation's falling ... so far not fast enough. Headline inflation CPI basis eased to 3.2% in March from 3.4% prior month. Markets were disappointed. City analysts had expected a bigger drop. A fall to 3.1% had been expected. There's just no pleasing some folk.

Best not to look at the detail. Goods inflation fell to 0.8%. Service sector inflation eased to 6.0%. Add the two together and divide by two, headline inflation would have been recorded at 3.4%. Weight them effectively (Goods inflation 0.5099 and Service sector inflation 0.4900), the headline rate would have been 3.4%, down from 3.6% prior month. Disappointed by the drop to just 3.2%. Markets would freak at a real rate of 3.4%. As it was the Governor sought to allay concerns suggesting the numbers were in line with expectations. The Chancellor Jeremy Hunt suggested this was confirmation of a soft landing. "The economy has turned the corner. People are beginning to see that." "The plan is working. Inflation is falling faster than expected. It is down to the lowest level in nearly two and a half years." he said. The slower decline in inflation, reinforced speculation the Bank of England will leave rates higher for longer. Financial markets are beginning to think the first rate cut may not happen until November. That's a tough call. Ten year bond yields trade at 4.25 this morning up from 4.10 at close last week. Analysts think inflation will slip back to the official 2 per cent target in April, impacted by a reduction in the energy price cap. Ruth Gregory, deputy chief UK economist at Capital Economics said: "With utility prices set to fall by over 12. per cent in April, inflation will still just about fall below the 2 per cent target in the month." "As long as inflation continues to fall fast in the coming months as we expect, the Bank may still feel comfortable cutting interest rates in June." For the moment this remains our central outlook, with further cuts possible by end of the year, closing the year towards 4.5%. Comments from Andrew Bailey suggest the MPC is prepared to loosen monetary policy ahead of the Fed. "There is strong evidence, inflation is receding. The dynamics for inflation are different now between the UK and the USA." Hawks in the Bank will remain concerned about the high levels of service sector inflation and the latest earnings data. Average weekly earnings at 5.6% are incompatible with a 2% inflation target. Doves on the MPC will express concern about negative growth in the economy, sluggish retail sales, the slight rise in unemployment and the drop in vacancies. Food inflation eased to 3.9% in March and core inflation eased to 3.9% from 5.0%. As we said earlier this week, the bears are watching. Come the MPC meeting in June, the doves will hold sway. For scenario planners we caution, 4.5% base rates may well be the new benchmark. No return to Planet ZIRP. In the UK, prior to the Great Financial Crash [2000 - 2008] the average inflation rate was 2.0%, the average UK bank rate was 4.50%. Ten year gilt yields averaged 4.50%. Thirty year gilts averaged 4.60%. The average growth rate was 2.5%. The average unemployment rate was 5.0%. Earnings averaged 3.9%. This is our "return to the mean" outlook.

0 Comments

We have had a few days now to digest the latest GDP Data for the U.K. economy. It has taken a few days since, like the King of Siam …

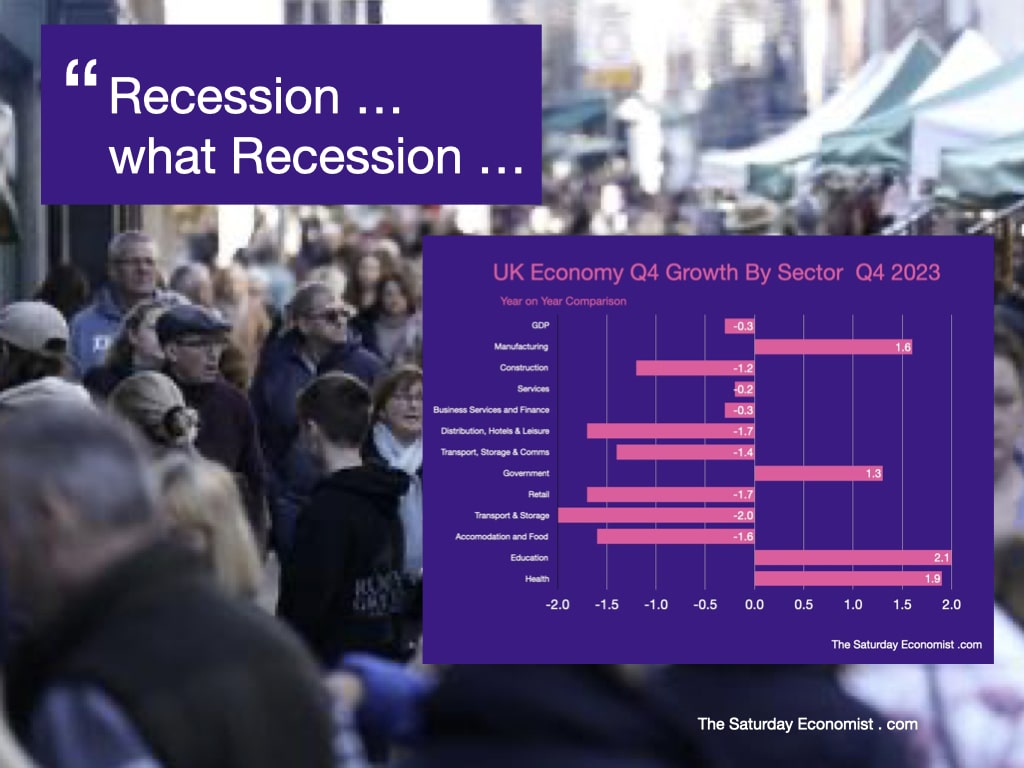

"There are times, I almost think I am not sure, of what I know I very often find confusion in conclusion" Confusion was compounded this weekend by headlines which appeared to suggest the UK was escaping from recession, after set backs in the third and fourth quarters of 2023. Indeed the ONS commentary was upbeat. Real gross domestic product (GDP) is estimated to have grown by 0.2% in the three months to February 2024, compared with the three months to November 2023. It is confusing. I have concluded there is confusion in conclusion. There is a fashion to report growth as a month on month, or quarter on quarter, phenomenon. Call me old fashioned but the valid conventional measure of growth is year on year and not quarter on quarter. The data set [ED2R GVA at basis prices] confirms year on year, growth slowed from 0.6% in Q1 last year to 0.5% in Q2 and Q3, before slipping to -0.2% in the final quarter. The data suggests growth in January was down by -0.1% and down by -0.2% in February. The bears are watching. Barring a bounce back in March, the first quarter of the year, will confirm the UK is in recession, with two successive quarters of negative growth year on year. Slipping into recession, no turning the corner, no light at the end of the tunnel, no dawn of recovery, no green shoots, no bouncing back, no storm passing. The Prime Minister may think “Wages are up. Energy bills are falling. Pensions are going up. Tax cuts are now already happening and benefiting people. The chancellor may think we are "Breaking Through The Clouds" when he set out his vision for long-term prosperity in the UK, optimism despite economic headwinds. Hunt may believe the economy is "back on track". He has rejected the "gloom" about the UK's economic prospects and declaring "declinism about Britain is just wrong." Both Hunt and Sunak should take a hard look at just what happened in the final quarter of last year. There was some good news. Education and healthcare were up by almost 2%. Manufacturing output was up by over 1.2%. But construction output fell by -0.5%, retail and distribution was down by almost 1%. Accommodation and food down by 1.5%. Transport and storage down by over 3%. Into the first quarter of 2025 and the poor performance of the service sector continues, falling by 0.3% year on year. The latest jobs data suggest the unemployment rate is rising as vacancies continue to fall. The bright spot, the arts and entertainment sector is growing by over 6.5% this quarter compared to almost 5% in the last quarter of the prior year. Which just goes to show the information should all be shared with a pinch of uncertainty. Let’s hope we are back on track and breaking through the clouds. Technically we are in recession and the bears are watching ...  One of the world's richest people and the head of the nation's largest bank, join a group of business executives making bold prognostications about the potential of artificial intelligence, according to the Wall Street Journal last week.

Elon Musk and Jamie Dimon both say artificial intelligence could usher in dramatic change. It will be smarter than humans, transform society and surpass the collective intelligence of mankind in five years. "My guess is that we will have AI that is smarter than any human probably around the end of next year," Musk said in a recent interview. "AI is the fastest-advancing technology I have ever seen." Jamie Dimon, chief executive of JPMorgan Chase, told investors Monday that AI could be as transformative as some of the major technological inventions over the past several hundred years. "Think the printing press, the steam engine, electricity, computing and the Internet, among others," Dimon wrote in his annual letter to shareholders. "The AI race to build the next big thing has sparked a talent war in Silicon Valley. Tech companies have poured cash into AI at a breakneck pace." Google Chief Executive Sundar Pichai has said AI could be more profound than the invention of fire or electricity. Vinod Khosla, founder of venture-capital firm Khosla Ventures, declared last year that within 10 years, AI will take on "80% of the jobs that exist today." "The need to work in society will disappear within 25 years for those countries that adapt these technologies," Khosla said in an interview with The Wall Street Journal. The technology has also led to stark warnings about the future of humanity. Earlier this week, Japan's largest telecommunications company and the country's biggest newspaper cautioned in a manifesto unless AI is restrained, democracy and social order could collapse. In the U.S., the Biden administration last year invoked emergency federal powers to compel major AI companies to notify the government when developing systems that pose a serious risk to national security. Some say predictions of AI's transformative powers have been overblown. Gary Marcus, a cognitive scientist who sold an AI startup to Uber in 2016, said generative AI may one day approach a level where it can transform society, but there has to be vast improvements to approach the level of change produced by the internet or even smartphones. "Generative AI programs currently make too many mistakes, are unreliable and have a superficial understanding of the world," Marcus said. "It is implausible that AI will approach human intelligence by the end of next year. Surpassing all of human intelligence in the next five years is also far-fetched", he said. Marcus offered to wager $1 million with Musk that his prediction of AI becoming smarter than a human by next year turns out to be wrong. Damion Hankejh, chief executive of Ingk, a startup semiconductor company, says he is bullish on the future of AI, saying it will be the next tech renaissance. But he doesn't think current AI systems will advance enough to surpass human intelligence. It's never going to happen," Hankejh said."Digital math machines aren't brains." "There's a lot of hype in AI right now," says Angel Vossough, the co-founder and chief executive of BetterAI. "AI systems are good at analyzing large data sets, and can make predictions or speed up productivity. But they are nowhere near being as intelligent as humans", she said, "a big part of human intelligence is emotional intelligence." "AI needs to connect, understand and respond to human emotions in a way that actually feels authentic and meaningful" she said. "I don't think we are anywhere close." How To Organise for AI ... Just Say CAIO ... Chief AI officer CAIO is one of the hottest new job titles but some say AI strategy should be everyone's job. Many organizations have decided that AI is too important and complicated to rely on one executive to develop and manage their strategy. Organizations raced to develop AI ideas and leadership in 2023. President Biden ordered every federal agency to hire a chief AI officer (CAIO) by the start of 2024. Imagine that a CAIO in every government department in the UK. It could even lead to an end to fax machines in the NHS ... That's all for now. Let me know what you think. Have a great week ahead ... References Elon Musk and Jamie Dimon's AI Predictions and What They Mean for the Future of Humanity - Wall Street Journal. Joseph De Avila. 10th April 2024. Dimensions of Strategy on Artificial Intelligence ... our own series  Hey Buddy Can You Spare A Dime ... Or Make That Half a Billion Dollars ...

I guess we have all been there.. You start the week struggling to find half a billion dollars, then suddenly six come all at once. Better than real estate, the Trump fortunes were boosted by a social media maxi-meme valued, at one stage last week, at over $10 billion dollars. The move valued DJT's personal stake at $6 billion, catapulting Donald Trump into the top billionaires list ranking alongside George Lucas and Georgio Armani. They say you can't beat the market. You can't beat a social media application and nothing beats a maxi-meme. It's much more fun than real estate. You don't have to dress the figures or overstate the floor space. The market's imagination and momentum does the job. Trump's Media & Technology Group Corp. [TMTG], the main product of which is Truth Social, has been absorbed into Digital World Acquisition Company. DWAC is a SPAC, we hope its not a dog but more on that later. The initial share deal valued TMTG at $875 billion. Not bad for a business, which reported a net loss of $58 million in 2023, with total revenue of $4.1 million in that time. Not bad for a business which brings in little revenue, posts zero profit and has no indication it has a path to profitability that would justify a valuation of almost $1 billion, let alone a valuation of over $10 billion which the stock hit in the first week of trading. Not bad for a business which did not provide the Digital World Board with financial projections in connection with the due diligence process. Not bad for a business which has identified a material weakness in its internal control over financial reporting. The acquisition prospectus explains, Digital World may not be able to accurately report its financial results in a timely manner, which may adversely affect investor confidence and materially and adversely affect business and operating results. Not bad for a business which does not currently, and may never, collect, monitor or report certain key operating metrics used by companies in similar industries. KPIs like sign ups, average revenue per user, ad impressions, monthly and daily active users. That sort of thing. Why not? The prospectus explains, "Since its inception, TMTG has focused on developing Truth Social by enhancing features and user interface rather than relying on traditional performance metrics." "While many industry peers may gather and report on these or similar metrics, given the early development stage of the TMTG platform, TMTG's management and board has not relied on any particular key performance metric to make business or operating decisions." "At this juncture in its development, TMTG believes that adhering to traditional key performance indicators, could potentially divert its focus from strategic evaluation with respect to the progress and growth of its business." "TMTG believes that focusing on these KPIs might not align with the best interests of TMTG or its shareholders, as it could lead to short-term decision-making at the expense of long-term innovation and value creation. No short-termism in the TMTG board room. Well there you have it. No short-termism in the TMTG board room. Working for the long term to justify the market faith in the business. Presumably advertisers will have to take the performance figures in good faith or be prepared to lob a bit of cash into the Donald Trump coffers to make good the revenue targets. Not bad for a business which cannot assure investors that TMTG will effectively manage TMTG's growth. If TMTG fails to effectively manage its growth, business and operating results could be harmed. Another warning. Page 126 Prospectus. Not bad for a business which is now a Donald Trump company. The prospectus warns there are a number of companies that were associated with President Trump have filed for bankruptcy, including one with a DJT Ticker. The ticker symbol "DJT" was also previously used by Trump's Atlantic City casino business, Trump Hotels and Casino Resorts, which went public in 1995 and eventually filed for bankruptcy in 2004. The prospectus warns, there can be no assurances that TMTG will not also become bankrupt. The use once again of the DJT Ticker for TMTG, may well serve as a mega-warning from a mega-meme. I could have been so different. DWAC considered fifteen different deals in view of delays with TMTG. The Prospectus reveals Digital World sent an NDA to Target B, an American pet care company offering a technology platform to enable on-demand and scheduled dog walking, training, and other pet care services. In the end target B walked with another suitor. So there you have it. DWAC could have morphed into a doggie app. Cynics argue, there's time yet. Doggie App or Maxi Meme? Post Note ... DJT closed at $48.66 last night, down 40% from peak last week as the company announced "TMTG expects to incur operating losses for the foreseeable future," according to yesterday's filing with the Securities and Exchange Commission. ------------------------------------------------------------------------------- Notes On The Art Of The Deal ... Digital World [DWAC] Digital World [DWAC] is a special purpose acquisition company [SPAC] formed for the purpose of effecting a merger, capital stock exchange, asset acquisition, stock purchase, reorganisation or similar business combination with one or more businesses. Digital World was incorporated under the laws of the State of Delaware on December 11, 2020. In September 2021, the SPAC raised approximately $300 million dollars by the issuance of around 30 million shares marked at $10 dollars per share. Trump Media & Technology Group Corp. [TMTG] Trump Media & Technology Group Corp. [TMTG] is a Delaware corporation which aspires to build a media and technology powerhouse to rival the liberal media consortium and promote free expression. TMTG was founded to fight back against the big tech companies, Meta (Facebook, Instagram and Threads), X (formerly Twitter), Netflix, Alphabet (Google), Amazon and others. TMTG was incorporated under the laws of the State of Delaware on February 8, 2021. TMTG's first product, Truth Social, is a social media platform aiming to disrupt big tech's control on free speech by opening up the Internet and giving the American people their voices back. Truth Social was generally made available in the first quarter of 2022. Valuation At the time of valuation, the median enterprise value of the available "Trading Comparables" surpassed $324 billion. Specifically, the enterprise value of Twitter (now known as X), the closest competitor to TMTG's initial product, Truth Social, was $41 billion. Therefore, at such time, Digital World's management concluded that an initial valuation of $875 million, with the potential for an additional earnout of $825 million, was a reasonable assessment for TMTG's enterprise valuation in the Business Combination transaction.  Inflation Set To Fall ... Interest Rates Set To Follow ...

Bond yields rallied, Sterling slipped against the Dollar this week. The latest US inflation suggests CPI is heading higher. Analysts are beginning to rethink, the forward outlook for US interest rates and the actions of the Federal Reserve. It doesn't take much to spook markets. Uncle Sam's CPI inflation increased to 3.2 per cent in February from 3.1 per cent prior month. Producer prices increased to 1.6 per cent in February, up from 1 per cent in January and 0.8 per cent in November last year. Markets moved. Ten year bond yields increased to 4.31% in the U.S. and 4.10% in the U.K. Sterling slipped from $1.29 to $1.27. When it comes to understanding market moves, "Any explanation is better than none" (Nietzsche). In the U.K. We won't have to wait long for an update. The MPC is set to meet this week. A decision on UK rates due Thursday. The latest inflation data is due on Wednesday. This will give some steer to the direction of travel on prices and base rates. So what to expect? Market forecasts suggest consumer price inflation will have fallen from 4 per cent in January to 3.5 per cent last month. This, on the back of slowing food and energy prices. Core inflation, excluding food and energy, is expected to have eased from 5.1 per cent to around 4.5 per cent. Strong disinflationary pressures and tight monetary policy may cause inflation to fall below the 2 per cent target this year. The Office for Budget Responsibility produced new forecasts this month. They indicate inflation will hit the 2 per cent target in the second quarter and will stay below target for the rest of the year, ending the year at 1.4 per cent. The Bank of England forecasts suggest inflation will hit the 2 per cent target in the second quarter but inflation is expected to rise in the second half of 2024. Inflation will end the year a 2.8%, meeting the 2 per cent target only in 2025, the Bank said. Falling food prices and energy costs the critical drivers. Intervention of the Ofgem price caps of great assistance in April. The rosy coloured outlook for inflation may not be so easy to achieve. Oil prices Brent Crude averaged $83.48 dollars in February compared to $82.59 last year. Prices averaged $75 dollars in May and June 2023. The latest earnings data suggest whole economy earnings were 5.6 per cent in January (6.1 per cent excluding bonuses). Moving in the right direction but as yet incompatible with the 2 per cent target. Service sector inflation, accounting for almost half the index, increased to 6.5 per cent in January, up from 6.3% in November. So we await with interest, the February figures for inflation. Some steer on what happens next with Base Rates may then follow. Bank of England Interest Rate Decision ... There is little or no expectation the Bank of England will lower rates this week. Rates on hold the probable decision. The only excitement, the voting mix, "stick or twist". As David Smith writing in the Sunday Times this week points out ... "It is now more than seven months since the MPC last changed interest rates.. It would be a big surprise if there is not another hold this week. That does not mean that there will be no interest in Thursday's decision. Last month, one member of the committee, Swati Dhingra, voted to cut, while two members, Catherine Mann and Jonathan Haskel, voted to raise rates. The other six were happy to leave things unchanged. Some of the speculation this week is therefore, whether anybody else joins Dhingra in voting for a cut rates, which at this stage is considered unlikely, and whether Mann and Haskel throw in the towel on further rate rises." So when will there be a cut in rates? Following this week's meeting, the MPC will have five more meetings and five more opportunities to cut interest rates this year. Markets think May is too early. June is favoured for the first cut of 25 basis points. August, September, November and December are the remaining meetings scheduled this year. December too close to Christmas. November too close to an election, if he makes it that far! We anticipate base rates at 4.5 per cent by the end of the year. That would suggest rates cuts possible in August and September but not much more to follow in 2025 . In the UK, prior to the Great Financial Crash [2000 - 2008] the average inflation rate was 2.0%, the average UK bank rate was 4.50%. Ten year gilt yields averaged 4.50%, real GDP growth averaged 2.5%, earnings averaged 3.5%, the unemployment rate averaged 5%. As always, "'The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals." Oops, that's the Fed, not the Old Lady, talking.  It was budget day on Wednesday. No rabbit from the hat, no bounce for the dead cat. The Deep State was silent. The Chancellor of the Exchequer presented his Spring budget. It will be his last before the election. An election which could take place as early as May.

It's going to be great. We will be the creative capital of Europe, the next Hollywood, the next Silicon Valley. Not for the moment, the low tax, "Singapore of Europe" but we are still working on that. National Insurance will be abolished (but not anytime soon). We begin with a with an additional 2% cut, to an 8% rate, beginning in April this year. Full expensing of leased assets to be included for business tax relief. Capital gains tax for sales of second homes to be cut from 28% to 24%. We are on track to become the world's next Silicon Valley. We have become Europe's largest film and TV production centre. Studio space in the UK has doubled in the last three years. At the current rate of expansion, we will be second only to Hollywood by the end of 2025. We are providing more military support to Ukraine than nearly any other country. Our spending will rise to 2.5% of GDP as soon as economic conditions allow, or the Russians invade the Baltic states. Plans for leveling up continue, more money for Cambridge and Canary Wharf. AstraZeneca to invest £60m to expand their footprint on the Cambridge Biomedical Campus. Canary Wharf to be transformed into a new hub for life science companies. Problems in the hospitality sector identified. The freeze on alcohol duty will be extended to April 2025. The 75% business rates discount for pubs will continue. Fuel duty will be frozen for the thirteenth year in succession. The freeze means fuel duty will remain at 57.95p per litre, as it has since March 2011. The 'temporary' 5p cut on the fuel tax, first introduced in March 2022 by Chancellor Rishi Sunak, will remain in place until March 2025. The investment needed to modernise NHS systems so "they are as good as the best in the world" will be fully funded by central government. It will cost £3.4 billion and unlock £35 billion of savings, a ten fold payback assuming development costs can be kept under control and we don't use Huawei, Fujitsu or TikTok. "We will slash the 13 million hours lost by doctors and nurses every year to outdated IT systems. We will use AI to cut down and potentially cut in half, form filling by doctors. We will digitise operating theatre processes allowing the same number of consultants to do an extra 200,000 operations a year." We will also get rid of fax machines and use WhatsApp.  We have made good progress ...

OBR forecasts show we have made good progress on the Prime Minister's three economic priorities. Inflation has halved ... Debt is falling ... Growth is 1.5 percentage points higher than predicted. The OBR expects the economy to grow by 0.8% this year and 1.9% next year. After that growth rises to 2%, 1.8%, and 1.7% in 2028. Inflation will fall to 2%. Underlying debt, will be 91.7% of GDP in 2024-25, then 92.8%, 93.2%, 93.2% before falling to 92.9% in 2028-29 with final year headroom of £8.9bn. (That's enough for another NI cut!) Business confidence is returning ... Business confidence is returning. Investment is surging. In the short period since the Autumn Statement, Nissan have announced they will build two new electric car models in the UK. Microsoft and Google have announced data centres worth over £3 billion. Thanks to the Business Secretary, the Global Investment Summit unlocked £30 billion of investment. There will be more money for police technology ... There will be more money for police technology. We will spend £230m rolling out time saving technology which speeds up police response times. Victims will be able to report crimes by video call (assuming their phones haven't been nicked). Drones will be used as first responders, under a new "Use Your Phone or Talk To A Drone" campaign. This way, all incidents will be attended with a "Fly By" at least. The crime response stats will be improved at the "flick of a joystick". Non Dom status will be abolished ... Non Dom status will be abolished raising £2.7 billion a year but there's a catch ... From April 2025, new arrivals to the UK will not be required to pay any tax on foreign income for their first four years of UK residency. This is a more generous regime than at present and one of the most attractive offers in Europe. But after four years, those who continue to live in the UK will pay the same tax as other UK residents. In a two-year period, individuals will be encouraged to bring wealth, earned overseas, to the UK where it can be spent, invested and taxed! This measure will attract £15 billion of foreign income and generate more than £1 billion in extra tax, it is said. Yes they will be arriving by the boat load, who could resist that offer. Overall, abolishing non-dom status will raise £2.7 billion a year by the end of the forecast period. That's assuming "they stay to pay". There aren't many, anyway, approximately 37,000, of which 90% choose to leave with seven years as it is. If they come and leave within four years, they will be better off under the new regime. It's a four year window. Time to work things out and time to buy a second home in Monaco. Village Hall Boost ... More good news, there will be £5m to renovate hundreds of local village halls across England so they can remain at the heart of their communities, hosting food banks and social services as local authority budgets are slashed.  Liz Truss complained, when ditched as Prime Minster, she had been "downed by the deep state". The Bank of England, the Office for Budget Responsibility, the International Monetary Fund, the Economist and the Financial Times were all, she claimed, part of the Deep State. A sinister left-wing cabal promoting something called "wokeonomics" and an anti growth agenda.

"We have to understand how deep the vested interests of the establishment are, how hard they will fight and how unfairly they will fight in order to get their way". "That is what I learnt from my time as a government minister and my time in No 10." [Obviously a quick learner.] This time, this budget, the deep state was silent. Or was it? According to Tom Peck in the Times on Friday, maybe the Institute of Fiscal Studies should be added to the Deep State Hit List. "The IFS post-budget briefing is where budgets traditionally go to die". Director, Paul Johnson, the Wonk King, stands up in front of the assembled wonks and nobly fulfills his role of national, post-budget, extractor fan. The smoke is sucked away. The mirrors smashed." Reality revealed. "Nothing that Jeremy Hunt did yesterday, changed anything," Paul Johnson said on Thursday "We are still heading for a parliament in which living standards will be worse at the start than at the end. That's pretty much unprecedented." Tax revenues are seen to rise to the highest level, as a share GDP, since 1948. Pensioners will be punished by the latest budget moves. Risks to borrowing from certain tax cuts now, are to be paid for by back loaded uncertain increases in the future. Spending plans are largely unspecified. Richard Hughes Director at the OBR has called Government spending plans a " work of fiction". "Some people call [the projections] a work of fiction, but that is probably being generous. At least someone has bothered to write a work of fiction, the government hasn't even bothered to write down what the departmental spending plans are", he said. The IFS claims, there would need to be at least £20 billion of spending cuts, for departments other than the ring fenced departments of, health, defence, education and child care. Where would they come from? This, will be a "staggeringly hard choice". "How do you make cuts, given NHS waiting lists, local authorities at or near bankruptcy, backlogs in the justice system, long-term cuts to university funding and struggles in social care and prison systems". The £20 billion plus savings from productivity improvements are ambitious. The inclusion of £5 billion revenue annually for energy hikes in the future, flies in the face of history. How do you make cuts? The answer is, you don't or can't. The staggeringly hard choice will almost certainly be somebody else's problem, given the next spending review will take place rather conveniently, after the next election. Some agree with Professor Philip Cowley and have signed up to his Campaign to Scrap the Budget. "Such occasions of parliamentary theatre, give governments an incentive to put short-term gimmicks above serious policy development". Short term gimmicks? Never! Yep, tough choices to be made but after the next election. It could be sooner than you think ...  Retail sales bounced back in January following a disappointing quarter at the end of 2023. Sales volumes were up by almost 1% in the month, year on year. Sales values increased by 4%.

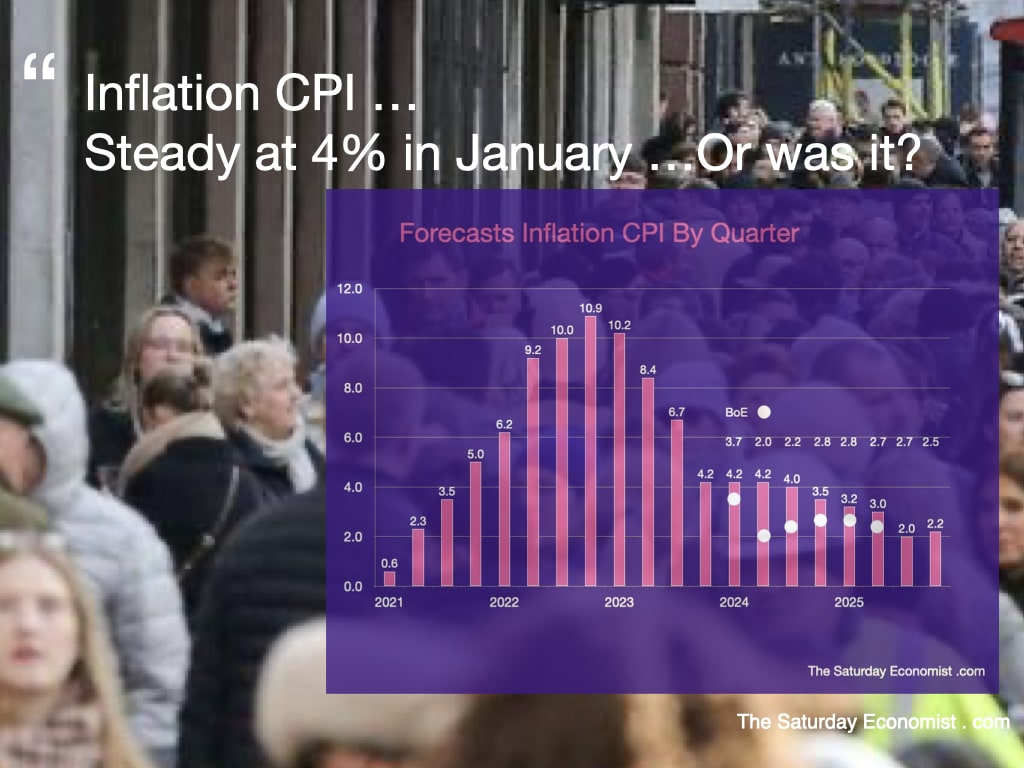

Consumers were spending big on alcohol (27%), music (34)%, computers (27%) and cosmetics (9%). Flowers, plant and seed sales were up by 18%, second hand goods sales increased by 29%. Biggest losers were chemists (-18%) and clothing retailers (-8%) . There is a pattern in there somewhere. Remember "Any explanation is better than none". Nietzsche. So what of the recession? Did you miss it? Markets, journalists and analysis were disturbed by the latest GDP date released on Thursday. The GDP monthly estimate for December 2023 revealed Real Gross Domestic Product (GDP) is estimated to have fallen by 0.3% in the three months to December 2023, compared with the three months to September 2023. According to the ONS, "On a quarterly basis, this gives two consecutive falls in GDP, with a fall of 0.3% in Quarter 4, following a fall of 0.1% in Quarter 3." For some, this constitutes a technical recession, defined as two consecutive falls in quarterly GDP. For purists (and those with pedantic disposition) this is not the case. The definition of recession requires two consecutive falls in quarterly GDP year on year, not quarter on quarter. This did not happen. The so called "technical recession" is in fact a "phantom recession." For the year as a whole, the UK economy is expected to have increased by 0.5% in 2023, compared to prior year. In the first half of the year, GDP increased by 0.6% in Q1 and Q2. Growth then slowed to 0.5% in the third quarter, then fell in the final quarter of the year by -0.3%. It was a strange quarter and a strange slow down. According to the latest employment data, the unemployment rate actually fell to 3.8% in December, the number unemployed fell to 1.3 million from 1.5 million in June. Data hardly consistent with a lurch into recession. Analyze the GDP fall by sector and the pattern becomes even more confusing. Strong growth was experienced in manufacturing and government spending, especially on health and education. Construction output slipped in the quarter, down by 1.2%. We still expect growth of 2.5% in the year as a whole, following a strong performance in the first half of the year and Q3. It is within the service sector down by -0.2% the damage occurred in the final quarter. Retail sales were down by 1.5%, this impacted on transport storage and communications, down by 1.4% overall (1.7% in retail and 2.0% in transport and storage.) In the leisure sector, distribution, hotels and leisure output fell by 1.7%, accommodation and food sales specifically fell by 1.6%. Maybe there is something of a structural change occurring in the sector as consumer spending is redirected. This month, Pryzm night club owner Rekom announced the closure of seventeen venues with the loss of 500 jobs. Students pre-drinking and not going out mid-week is to blame for nightclubs closing, the boss of the UK's biggest club chain has said. New data suggests close to 400 clubs permanently shut down between March 2020 and December 2023, according to the Night Time Industries Association (NTIA). Overall, the UK restaurant industry demonstrated resilience in the face of challenges including inflation, rising energy costs, food costs, staff turnover, recruitment difficulties and transport strike action. Yet ... According to the BDO Restaurant and Bars Report for 2023, over half of consumers cut back on discretionary spending to put the money towards energy bills. Of these people, 6 in 10 intended to achieve this by reducing how often they eat out (Barclaycard); 77% of UK hospitality firms reported a decrease in diners and drinkers at the end of last year. Outlets are responding by reducing opening hours and days to reduce energy costs. The British Beer and Pub Association reported over 500 pubs closed for good in 2023. In the Hotel sector, according to "Visit Britain" Hotel Occupancy rates were actually up in the final quarter from 76.3% to 77.0% thanks to a slight increase in the December performance. Overall, a disappointing performance in the leisure sector in the final quarter. The trade will be looking for a budget boost in the March statement on business rates, lower VAT and reform of the apprenticeship levy. The step up in the National Living Wage in April is unlikely to improve sentiment. The easing of price pressures on food and energy will help. The anticipated fall in base rates will undoubtedly assist. For the year as a whole, we still expect modest GDP growth of 0.7% in 2024 and over 1.3% in 2025. Inflation is expected to slow further, our base rate outlook is unchanged.  Expectations of a midsummer rate cut increased sharply this week in response to the release of cooler than expected inflation data for January. The Bank of England will make the first cut to interest rates since 2020 at its June meeting, if not before, according to money market bets.

Financial markets are now forecasting, with a probability of 70 per cent, the Monetary Policy Committee will lower the base rate from 5.25 per cent either at, or before, the June 20 meeting. Markets had expected inflation to ease up to 4.1% in the month. As it was, goods inflation eased to 1.8% from 1.9% prior month. Service sector inflation edged up to 6.5% from 6.4%. Food inflation eased to 7%, energy costs were down by just over 18%. Core inflation was steady at 5.1%. The headline CPI rate was unchanged at 4.0%. The arithmetic of goods and service sector inflation, a model in which both are equally weighted, suggests 4.1% would have been nearer the mark for January CPI but that would also apply to November and December for that matter. The inflation numbers followed updates on earnings and wages in the latest employment data. Earnings increased by 5.8% in the three months to December from 8% in the previous quarter ending September. We expect the rise in earnings to ease to 4.5% by the end of the year Q4. Inflation CPI to end at 3.5% in the final quarter. Not quite as optimistic as the Bank of England perhaps but even so ... Our base rate scenario is unchanged, we expect base rates to end the year at 4.5% with the first cut in May or June ... |

The Saturday EconomistAuthorJohn Ashcroft publishes the Saturday Economist. Join the mailing list for updates on the UK and World Economy. Archives

April 2024

Categories

All

|

| The Saturday Economist |

RSS Feed

RSS Feed

The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The presentation should not be construed as the giving of investment advice.

|

The Saturday Economist, weekly updates on the UK economy.

Sign Up Now! Stay Up To Date! | Privacy Policy | Terms and Conditions | |